Mitie group plc – Annual report – 31 March 2017

Industry: support services

- Basis of preparation and significant accounting policies (extract)

(c) Prior year restatements

During the year there was an apparent significant shortfall in the expected profitability of the Group for the year ended 31 March 2017. A new executive management team was appointed in December and January and they immediately launched an Accounting Review process to provide confidence that all relevant accounting standards were appropriately reflected in the Group’s financial reporting.

Following additional information becoming available, the review work has identified a number of prior year errors that, due to their materiality, require the restatement of the results for the year ended 31 March 2016, as well as the consolidated balance sheet positions as at 31 March 2016 and at 31 March 2015.

These prior year restatements relate to the following areas:

Impairment of Healthcare goodwill

The Healthcare goodwill impairment testing for the year ended 31 March 2016 was carried out by reference to a business plan, which incorrectly included within it an apprenticeships business and certain other assumptions. Correcting for these errors in the goodwill impairment model would have resulted in Healthcare goodwill being impaired by £26.0m in the year ended 31 March 2016. This amount has now been written off to the consolidated income statement in the year ended 31 March 2016.

Additionally there was a material disclosure deficiency in the 2016 Annual Report and Accounts, in that there was a failure to disclose the significant judgements made around the inclusion of new service line expansion plans in the Healthcare business, adjacent to existing skills and assets already in the business. See Note 2 for further details.

Intangible asset write-off

Errors arising from the incorrect application of accounting policies during the impairment testing of other intangible assets for the year ended 31 March 2014 resulted in the carrying value of capitalised software costs within intangible assets being overstated at 31 March 2015 and 31 March 2016. At 31 March 2015 this resulted in a net asset value of £2.8m being written off to the consolidated income statement together with a corresponding increase in the deferred tax asset of £0.5m. In the consolidated income statement for the year ended 31 March 2016 a credit for £0.5m has now been included in respect of amortisation no longer required, and a corresponding reduction in the deferred tax asset of £0.1m.

Under-accrual of costs

A number of under-accruals, or under-provisions, of various categories of costs have been identified in relation to prior years. These costs have now been written off to the consolidated income statement in the relevant years and were incurred in relation to:

i) employee bonuses that were paid during the year ended 31 March 2017 but related to the financial years ended 31 March 2015 and 31 March 2016 totalling £8.3m (2015 – £0.6m and 2016 – £7.7m); and

ii) under-provision of insurance liabilities that were outstanding at 31 March 2015 (£5.6m) and 31 March 2016 (£0.3m) and contract related provisions of £2.2m in the year to 31 March 2016.

The tax impacts of these adjustments were credits to the consolidated income statement of £1.3m in 2015 and £2.0m in 2016.

Overstatement of trade receivables and accrued income

Certain revenue recognition polices relating to the inclusion of disputed items in project revenues, the deferral in recognition of commercial claims and the recognition of profit margins on accrued income balances were not applied correctly, resulting in an overstatement of trade receivables and accrued income at 31 March 2015 (£4.6m) and 31 March 2016 of (£11.2m). These amounts have now been written off to the consolidated income statement along with a corresponding credit to tax of £1.0m in 2015 and £2.2m in 2016.

Summary

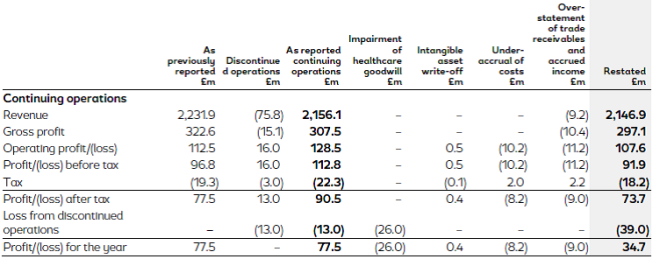

A summary of the combined impact of the prior year adjustments on the consolidated income statement and consolidated statement of cash flows for the year ended 31 March 2016 as well as the consolidated balance sheet as at 31 March 2016 arising from the restatements is as follows:

Consolidated income statement for the year ended 31 March 2016

Consolidated statement of cash flows for the year ended 31 March 2016

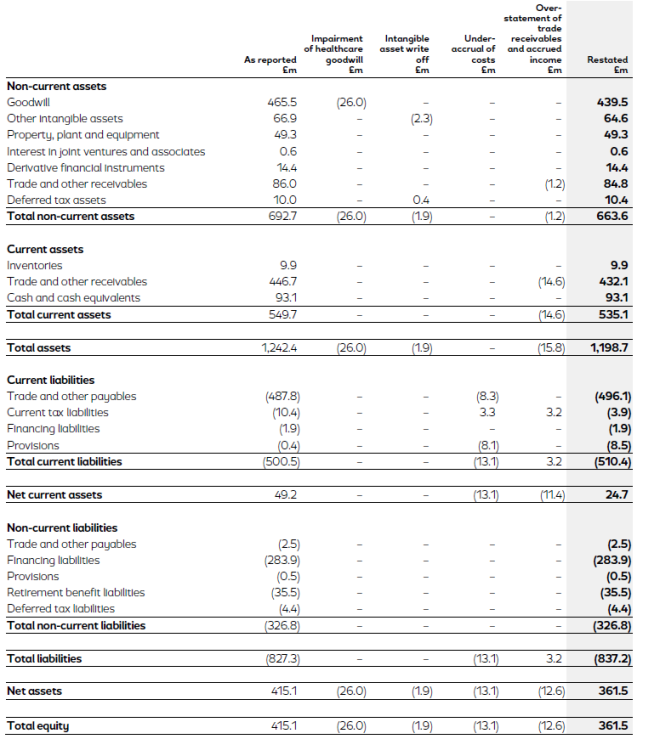

Consolidated balance sheet as at 31 March 2016

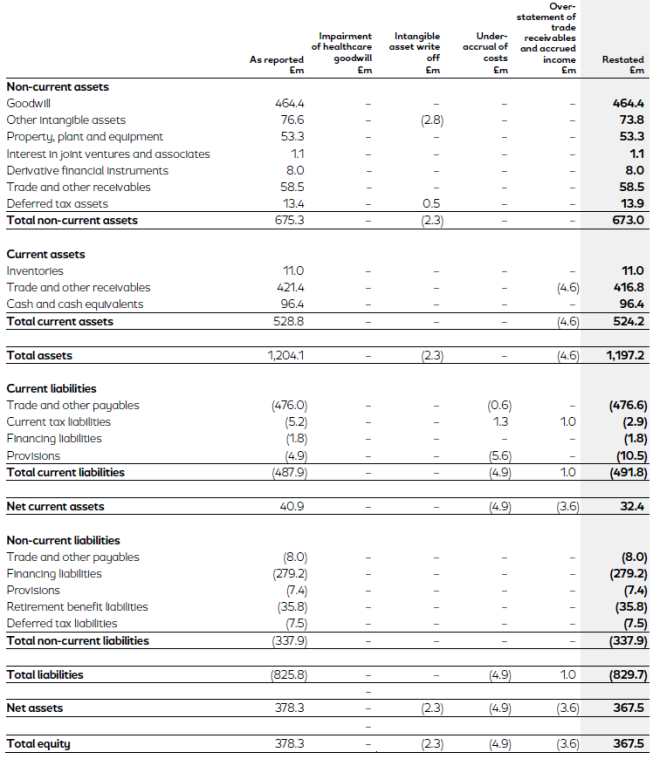

Consolidated balance sheet as at 31 March 2015

Consolidated balance sheet

As at 31 March 2017

Consolidated statement of changes in equity

For the year ended 31 March 2017

- Critical accounting judgements and key sources of estimation uncertainty (extract)

Key sources of estimation uncertainty (extract)

The key assumptions concerning the future, and other key sources of estimation uncertainty at the balance sheet date, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year, are discussed below.

Assessment of a prior year error in relation to goodwill on the Healthcare CGU

At 31 March 2016, the reported carrying value of Healthcare goodwill was £107.2m, with value-in-use calculated at £145.4m. At 30 September 2016 it was determined that the carrying value of this goodwill was fully impaired and written down to a nil value. Subsequently a large proportion of the Healthcare CGU was sold for £2 and the Group agreed to contribute £9.5m towards the trading losses of the business and the turnaround plan (see Note 6 ‘Discontinued operations and disposal of subsidiaries’ for further details on the sale of the Healthcare division).

As explained in the Audit Committee report on page 55 the FRC’s Corporate Reporting Review Committee has made enquiries in this area. During the course of preparation of our response to its February 2017 letter, new evidence came to light that had not previously been provided to the external auditor, the Audit Committee or the Board. The Audit Committee appointed KPMG to review the circumstances surrounding the judgement made on Healthcare goodwill at 31 March 2016.

As a result of the review, the Audit Committee has considered whether there were one or more errors, which in accordance with IAS 8, require a prior year adjustment.

As part of this assessment the Audit Committee considered the further information that was available at 31 March 2016 but had not been communicated to the external auditor, the Audit Committee or the Board. It has concluded that:

- One or more errors had been made in the preparation of the plan that was approved by the Board and formed the basis for the impairment testing of Healthcare goodwill. Correction of those errors reduces the value in use by £64.0m which results in an impairment to Healthcare goodwill of £26.0m as at 31 March 2016. The Audit Committee believes that this is a prior period error in accordance with IAS 8 and consequently a prior year adjustment is made in these accounts to goodwill at 31 March 2016 (see Note 1(c) ‘Prior year restatements’ for further details on the prior year restatements made).

- A number of other judgements were made in respect of the impairment testing of Healthcare goodwill at 31 March 2016, which were impacted by the discovery of further information and has been considered by the Board and Audit Committee as part of the preparation of the 2017 Annual Report and Accounts.

These judgements relate to the inclusion of new service line expansion plans in the Healthcare business, adjacent to existing skills and assets already in the business, namely provision of telecare services, community healthcare and supply of temporary staff on an agency basis.

Additionally, the inclusion of Tascor, acquired in January 2016, subsequently renamed Care & Custody Health and retained by Mitie following the disposal of the Healthcare business in February 2017, was regarded as part of the Healthcare CGU, rather than with the CGU that included Care & Custody (Soft FM CGU).

Had these been regarded as prior year errors rather than changes in judgement, the amount of the prior year adjustment would have increased by £44.0m.

The Directors have specifically reviewed the IAS 8 ‘Accounting Policies, Changes in Accounting Estimates and Errors’ definition of a change in accounting estimate which states that “changes in accounting estimates result from new information or new developments and, accordingly, are not corrections of errors”. The Audit Committee has carefully reconsidered the judgements it made in the light of the discovery of new information and notwithstanding this becoming available and taken into account, considers that the judgements made as to what should be classified as a prior year error have been formed on a reasonable basis. However, the Audit Committee recognises that the failure to disclose these judgements in the 2016 Annual Report and Accounts was in itself a material disclosure deficiency.