Rolls-Royce Holdings plc – Half year report – 30 June 2018

Industy: aerospace

Notes to the half-year financial statements (extract)

1 Basis of preparation and accounting policies (extract)

Significant accounting policies

Except for the adoption of IFRS 15 Revenue from Contracts with Customers and IFRS 9 Financial Instruments, the accounting policies applied by the Group in these condensed consolidated half-year financial statements are the same as those that were applied to the consolidated financial statements of the Group for the year ended 31 December 2017 (International Financial Reporting Standards issued by the International Accounting Standards Board (IASB), as adopted for use in the EU effective at 31 December 2017).

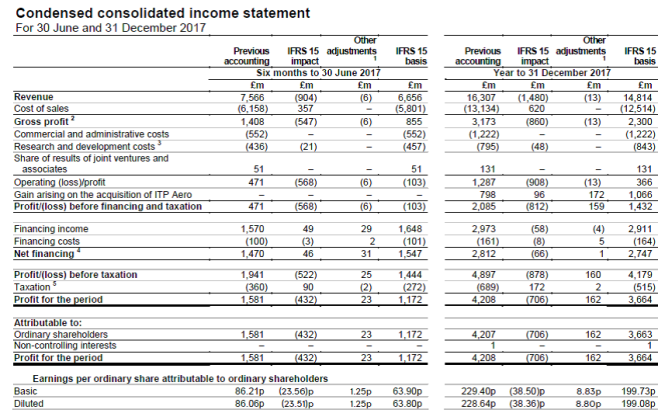

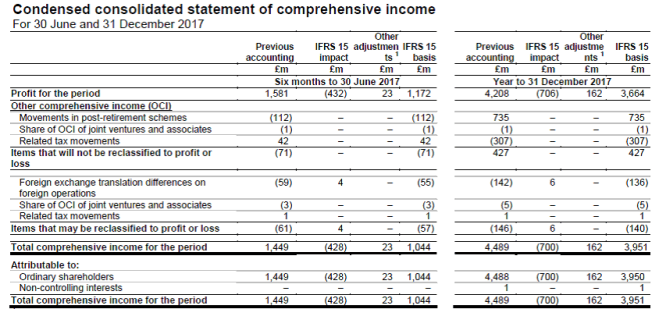

The prior period has been restated for IFRS 15 Revenue from Contracts with Customers, an interim update to the provisional fair values of the ITP Aero acquisition and other adjustments. See note 16 for more details.

IFRS 15 Revenue from Contracts with Customers

The Group adopted IFRS 15 on 1 January 2018 using the ‘full’ retrospective approach.

IFRS 15 provides a single, principles based five-step model to be applied to all sales contracts. It is based on the transfer of control of goods and services to customers. In summary:

- Revenues on original equipment (OE) and time and material aftermarket contracts are generally recognised at the point of delivery;

- Revenues on long-term aftermarket contracts and some OE contracts (generally for products without an alternative use to the specific contract) are recognised on an activity basis using the costs incurred as the measure of the activity; and

- Costs are recognised as they are incurred.

Accounting policy

Revenue recognised comprises sales to the Group’s customers after discounts and amounts payable to customers. It excludes value added taxes. The Group has elected to use the practical expedient not to adjust revenue for the effect of financing components where the expectation is that the period between the transfer of goods and services to customers and the receipt of payment is less than a year.

Sales of standard OE, spare parts and time and material overhaul services are generally recognised on delivery to the customer, unless the specific contractual terms indicate a different point.

Sales of services and OE specifically designed for the contract are recognised by reference to the progress towards completion of the performance obligation provided the outcome of contracts can be assessed with reasonable certainty.

- The Group generates a considerable proportion of its revenue and profit from aftermarket arrangements. These aftermarket contracts, such as TotalCare and CorporateCare agreements in Civil Aerospace, cover a range of services and generally have contractual terms covering more than one year. Under these contracts, the Group’s primary obligation is to maintain customers’ equipment in an operational condition and this is achieved by undertaking various activities, such as repair, overhaul and engine monitoring over the period of the contract. Revenue on these contracts is recognised over the period of the contract and the measure of progress is a matter of judgement. The stage of completion of the contract is best measured by using the actual costs incurred to date compared to the estimated costs to complete the performance obligations, as this reflects the extent of completion of the activities performed.

- The estimated revenue and costs under such agreements are inherently imprecise and significant estimates are required to take into account uncertainties relating to: (i) the forecast utilisation of the engines by the operator and related pricing; (ii) payments due to the customer that are either contractual and based on measures of performance or that could reasonably be expected to have been reflected in the contract price; (iii) the frequency of engine overhauls where the principal variables are the operating parameters of the engine and operational lives of components; and (iv) the forecast costs to maintain the engines in accordance with the contractual requirements where the cost of each overhaul is dependent on the required work-scope and the cost of parts and labour at the time.

- Future variable revenue is constrained to take account of the risk of non-recovery of resulting contract balances from reduced utilisation e.g. engine flying hours, based on historical forecasting experience, the risk of aircraft being parked by the customer and the customer’s creditworthiness.

- A significant amount of revenue and cost is denominated in currencies other than that of the relevant Group undertaking. These are translated at estimated long-term exchange rates.

- The assessment of stage of completion is generally measured for each contract. However, in certain cases, such as for CorporateCare agreements where there are many contracts covering aftermarket services, each for a small number of engines, the Group accounts for a portfolio of contracts together as the effects on the Condensed Financial Statements would not differ materially from applying the standard to the individual contracts in the portfolio. When accounting for a portfolio of long-term service arrangements the Group uses estimates and assumptions that reflect the size and composition of the portfolio.

- A contract asset/liability is recognised where payment is received in arrears/advance of the costs incurred to meet performance obligations.

- In rare circumstances we may incur costs of wasted material, labour or other resources to fulfil a contract where the level of cost was not reflected in the contract price, these are expensed when the trigger to incur these costs arises. The identification of such costs is a matter of judgement and would only be expected to arise where there has been a series of abnormal events which give rise to a significant level of cost which is also of a nature we would not expect to incur and hence is not reflected in the contract price. For example, where we have technical issues that require resolution to meet regulatory requirements; have a wide-ranging impact across a product type; and cause significant operational disruption to customers. Similarly, in these rare circumstances, significant disruption costs to support customers resulting from the actual performance of a delivered good or service may be treated as a warranty type cost in the period. Where material these costs are recorded as an exceptional non-underlying expense.

The Group has paid participation fees to airframe manufacturers, its customers for OE on certain programmes. Amounts paid are initially treated as contract assets within trade and other receivables and subsequently charged as a reduction to the OE revenue when it is transferred to the customer over the estimated number of units to be delivered. This estimate of the number of units may change over the course of the programme.

In assessing the accounting for the participation fee payments we make to our OE customers, we have also assessed the accounting for up-front payments we sometimes receive from the Group’s suppliers under RRSAs to allow them to participate in an engine programme. These receipts are deferred and recognised against cost of sales over the estimated number of units to be delivered.

The Group has elected to use the practical expedient to expense as incurred any incremental costs of obtaining or fulfilling a contract if the amortisation period of an asset created would have been one year or less. Where costs to obtain a contract are capitalised, they are amortised over the performance of the related contract.

16 Impact of adopting IFRS 15 and other adjustments

1 The other adjustments arise from: the revised calculation of the foreign exchange rate applied to non-monetary assets and liabilities £29m credit in June 2017 and (£4m) charge in December 2017; the revised unwind of discounting of non-current liabilities of (£4m) in June 2017 and (£8m) in December 2017; and a preliminary update of the provisional fair values arising on the acquisition of ITP Aero increasing the gain arising on acquisition in December 2017 by £172m.

2 Predominantly due to de-recognition of contractual aftermarket rights, de-linkage of OE from aftermarket contracts and a change to recognise revenue on long-term service agreements as costs are incurred rather than when the engines are operated.

3 Re-classification of the recognition of contributions received from the Group’s suppliers under Risk and Revenue Sharing Agreements (RRSAs) to cost of sales.

4 Revised phasing of foreign exchange in line with revised phasing of long-term service agreement revenues and unwind of discounting of future guarantee payments due to customers.

5 Consequential change from the restated reported profit.

1 See footnote 1 above.

1 The other adjustments primarily arise from: the revision of the foreign exchange rate applied to the initial recognition of non-monetary assets and liabilities that increases retained earnings by £140m; the reduction in deferred tax assets of (£18m); the use of a revised discount rate on non-current liabilities (£86m); and a reclassification of contract provisions from trade and other receivables to provisions for liabilities and charges (£12m current and £50m non-current). In addition a preliminary update has been made to the provisional fair values arising on the acquisition of ITP Aero in December 2017 increasing opening net assets by £172m. The tax effect of these items is to reduce net assets by (£3m).

2 The change in intangible assets primarily arises from the de-recognition of Contractual Aftermarket Rights (CARs) and reclassification of participation fees as contract assets within trade and other receivables as a result of IFRS 15 providing additional guidance on the treatment of payments to customers. The change also includes movement on ITP Aero, see note 14.

3 Consequential change from the restated cumulative profits.

4 Relates to the cost of parts sold where we retain an option to repurchase e.g. within a larger manufactured assembly. The customer has not obtained control based on the IFRS 15 definition, so the asset has been added to the inventory balance.

5 There are a number of factors impacting trade and other receivables as follows:

(a) Revised revenue allocation between years (deferred income) as a result of de-linkage of OE from aftermarket contracts and a change to recognise revenue on long-term service agreements as costs are incurred rather than as engines are operated.

(b) Recognition of an additional asset where we have incurred costs to obtain a contract that will subsequently be amortised as a reduction against the associated revenue as goods and services are delivered.

(c) Reclassifications of: participation fees from intangible assets; RRSA payments made ahead of parts usage as a prepayment from trade and other payables; and amounts billed in advance have increased the trade receivables asset (amount billed) and the contract liability within trade and other payables to better reflect the contractual position.

6 Cash received for parts sold with an option to repurchase as per 4 and future obligations to airframers arising from sale of our OE on their airframes.

7 Revised revenue allocation as a result of de-linkage of OE from aftermarket contracts and a change to recognise revenue on long-term service agreements as costs are incurred rather than when the engine is operated. Also includes reclassification of RRSA payments made ahead of parts usage as a prepayment within trade and other receivables.

8 As a result of the more refined guidance on contract liabilities we have reclassified balance from provisions into trade and other receivables / payables

9 Cumulative change from consolidating overseas entities IFRS 15 local currency income statement and closing balance sheet impacts into sterling.

10 Cumulative impact of restating prior period’s performance. Predominantly due to de-recognition of contractual aftermarket rights, de-linkage of OE from aftermarket contracts and a change to recognise revenue on long-term service agreements as costs are incurred rather than when the income is received.

11 Re-assessment of recoverability of financial assets using IFRS 9 principles has resulted in a reduction in net assets of £(15)m.

Cash flows

The adjustments to the income statement and balance sheet described above do not affect the cash balances, but do alter the categorisation of some items in the cash flow statement. In particular, the de-recognition of contractual aftermarket rights and the transfer of participation fees to contractual assets reduce additions to intangible assets by £172m and £346m in the half year and full year respectively. These cash flows are now included in the net cash flows from operating activities and there is a consequential change to the adjustment for amortisation of intangible assets. Other adjustments are principally within monetary working capital movements.

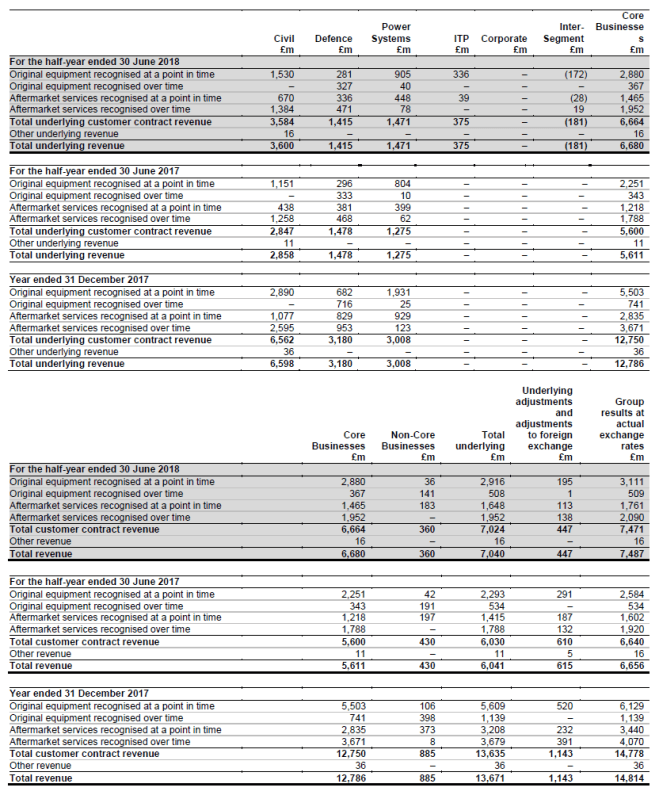

2 Analysis by business segment (extract)

Disaggregation of revenue from contracts with customers