Aker Solutions ASA – Half year report – 30 June 2019

Industry: construction, engineering

Note 10 Leasing

Financial Reporting Principles

IFRS 16 Leasing effective January 1, 2019 has significantly changed how the company accounts for its lease contracts. The company leases a number of office buildings in addition to manufacturing and service sites. The company also leases machines and vehicles. Before the adoption of IFRS 16, all lease contracts were classified as operating leases. IFRS 16 requires all contracts that contain a lease to be recognized on the balance sheet as a right-of-use asset and lease liability. Only certain short-term and low-value leases are exempt.

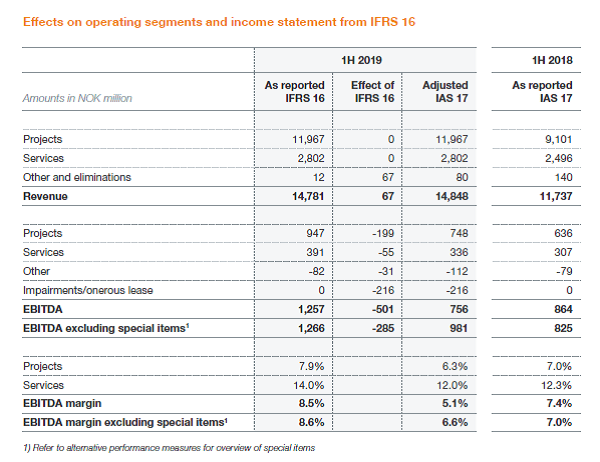

The right-of-use asset is depreciated over the lease term and is subject to impairment testing. The lease payments previously included as operating expense in the income statement are reported as depreciation and financial expense under IFRS 16. This results in an improvement of EBITDA, refer to “”special items and IFRS 16 effects”” section to see the impact of IFRS 16 on the performance measures of the operating segments. The lease liability represents the net present value of the lease payments to be made over the remaining lease period. The cash outflows for leases under IFRS 16 is presented as repayment of interest-bearing liabilities within financing activities in the cash flow statement. Interest paid is still classified as cash outflows within operating activities.

All sub-leases were previously classified as operating leases with lease payments recognized as revenue. Under IFRS 16, some sub-leases covering the major part of the lease term in the head-lease are classified as finance sub-leases. The portion of the right-of-use asset subject to sub-lease is de-recognized and a sub-lease receivable is recognized in the balance sheet when the sub-lease commences. The sub-lease will result in interest income and lower right-of-use depreciation under IFRS 16, rather than lease revenue as under IAS 17.

The company has implemented the leasing standard using a modified retrospective method with the cumulative impact recognized in retained earnings on January 1, 2019. Comparative figures are not restated. IFRS 16 Leasing replaced former leasing guidance, including IAS 17 Leases and IFRIC 4, SIC 15 and SIC 27. According to the company’s loan agreements, the new leasing standard will not impact the current debt covenants.

Judgments and Estimates

The company has applied significant judgment when determining impairment of the right-of-use asset. Impairment is assessed for separable parts of leased buildings that have been or will be vacated in the near future. The impairment is sensitive to changes in estimated future expected sub-lease income and sub-lease period. Judgment is also involved when determining whether sub-lease contracts are financial or operational, as well as when determining lease term for contracts that has extension or termination options.

Recognition and Measurement Approach on Transition

The company has elected to use the recognition exemptions in the standard for short-term leases and leases of low value items such as computers and office equipment. The company also applied the recognition exemption for leases that expire in 2019. The company adjusted the right-of-use asset on January 1, 2019 with the provision for onerous leases on December 31, 2018. The company has elected to exclude the initial direct costs from the measurement of right-of-use asset on implementation. The right-of-use asset for selected leases has been measured as if IFRS 16 had always been applied (using the incremental borrowing rate per January 1, 2019).

The discount rate has been determined for each leased asset according to the incremental borrowing rate at the date of implementation (January 1, 2019). On January 1, 2019, the discount rate applied varied between 2.0 and 11.5 percent giving a weighted-average rate of 4.4 percent. The non-cancellable lease period is basis for the lease commitment. Periods covered by extension or termination options are included when it is reasonably certain that the lease period will be extended. Non-lease components such as electricity, insurance and other property-related expenses paid to the landlord are excluded from the lease commitment for offices and manufacturing sites, but included when renting apartments and vehicles if included in the agreed lease amount. Future index or rate adjustments of lease payments are only included in the lease liability when a minimum adjustment has been contractually agreed and is in-substance fixed. Certain sub-leases that were operational under IAS 17 became financial under IFRS 16.

Implementation effects

The effect of implementing IFRS 16 as of January 1, 2019 was as follows:

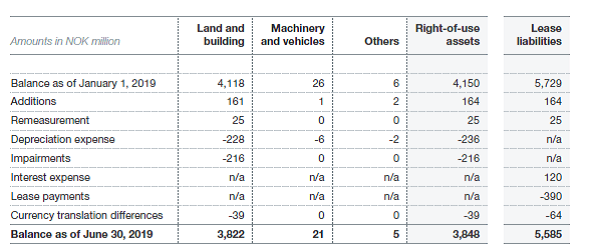

The movement in the right-of-use assets and lease liabilities since implementation is summarized below.

Lease payments of NOK 390 million consist of lease installments of NOK 270 million and interest expense of NOK 120 million. The impairment of right-of-use for land and buildings in the first-half 2019 mainly relates to buildings that are, or will be, vacated by Aker Solutions and update of market value of potential sub-leases.

Alternative Performance Measures (extract 1)

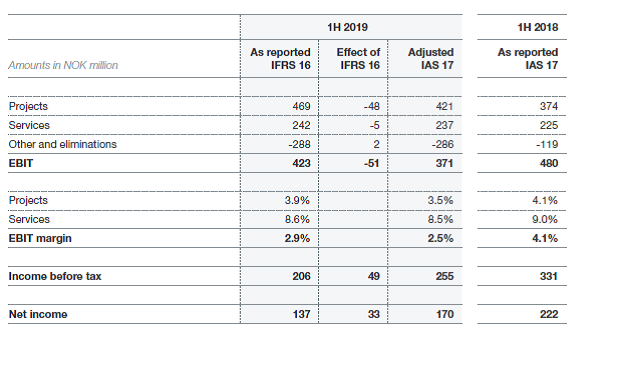

Aker Solutions discloses alternative performance measures in addition to those normally required by IFRS as such performance measures are frequently used by securities analysts, investors and other interested parties. Alternative performance measures are meant to provide an enhanced insight into the operations, financing and future prospects of the company. Figures for 2019 include the effects of IFRS 16, whereas comparative figures for 2018 do not. Refer to note 10 in the half-year report and section “Special items and IFRS 16 effects” for the effects on the profit per segment.

Alternative Performance Measures (extract 2)

Net debt to EBITDA (leverage ratio) is a key financial measure that is used by management to assess the borrowing capacity of a company. The ratio shows how many years it would take for a company to pay back its debt if net debt and EBITDA are held constant. The ratio is one of the debt covenants of the company. The ratio is calculated as net debt (total principal debt outstanding less unrestricted cash) divided by EBITDA excluding certain special items (as defined in loan agreements) for the last twelve month period. If a company has more cash than debt, the ratio can be negative. The leverage ratio does not include the effects of IFRS 16 Leasing, as covenants are based on frozen GAAP.