Australian Agricultural Company Limited – Annual report – 31 March 2026

Industry: agriculture

A Financial Performance (extract)

A1 Significant Matters (extracts

North Queensland Floods

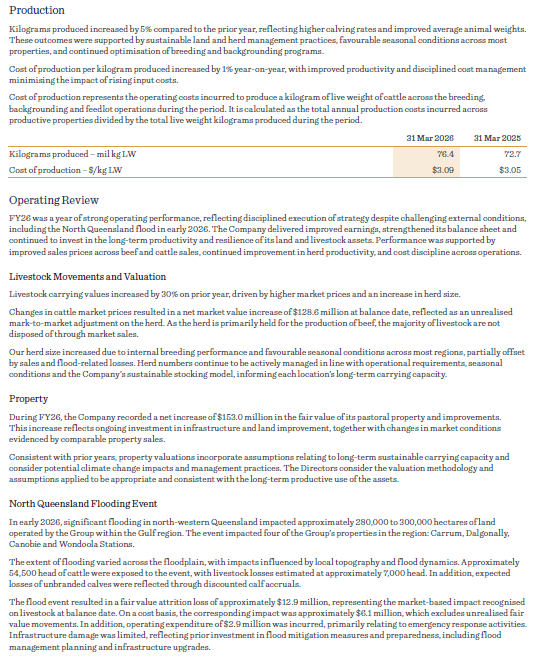

In early January 2026, a significant flood event impacted parts of north‑western Queensland following the development of a monsoon trough system. Flooding affected approximately 280,000 to 300,000 hectares of land managed by the Group in the Gulf region.

The event impacted four of the Group’s properties in the region: Carrum, Dalgonally, Canobie and Wondoola Stations. The extent of flooding varied across the floodplain, with impacts influenced by local topography and flood dynamics.

Approximately 54,500 head of cattle were exposed to the flood event. Livestock losses are estimated to be approximately 7,000 head, representing around 1.5% of the Group’s total herd. In addition, the Group has adjusted calf accruals on the impacted properties to reflect expected losses of unbranded calves, with approximately 3,900 head of calves estimated to have been lost.

Determining the extent of livestock losses across large and remote properties is inherently challenging. The losses recognised have therefore been based on the best available information and management’s best estimates and judgement. These estimates were prepared on a property‑by‑property basis using a combination of aerial observations of surviving livestock, physical inspections as floodwaters receded, assessment of damaged infrastructure, and an evaluation of expected survival rates by paddock having regard to land topography, flood behaviour and livestock vulnerability, including consideration of calf age profiles.

Livestock are recognised as biological assets measured at fair value less costs to sell in accordance with AASB 141 Agriculture. The estimated livestock losses resulted in a fair value attrition loss of approximately $12.9 million, representing the market‑based impact recognised in the Income Statement (see note A3). On a cost basis, the corresponding impact was approximately $6.1 million, which excludes unrealised fair value movements.

Infrastructure damage arising from the event was limited, with the majority relating to fencing and livestock water infrastructure. No infrastructure assets had been written off at balance date. Operating expenditure of $2.9 million was recognised during the year in relation to some infrastructure repairs, helicopter mustering and emergency fodder drops.

The flood event is considered significant due to the scale of the flooding, the geographic concentration of affected properties and the use of estimation and judgement in determining livestock losses and accrual adjustments.

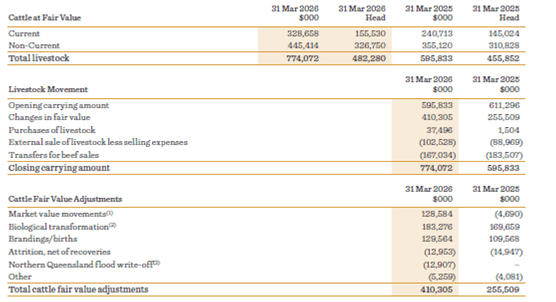

Herd Numbers

The closing herd headcount increased compared to the prior year, with 482,280 head on hand at 31 March 2026 (455,852 at 31 March 2025). This increase in the herd reflects the combined effect of the Company’s internal breeding program, seasonal conditions which were favourable across most properties notwithstanding flooding impacts in certain regions, and the purchase of some breeding stock. The impact of these factors has been partially offset by additional live sales and livestock losses associated with flooding in certain regions. Herd size continues to be managed in response to operational requirements and seasonal conditions.

Herd Valuation

The herd value movement since 31 March 2025 includes $410.3 million related to fair value adjustments. This includes unrealised gains of $183.3 million from biological transformation, in line with AASB 141 Agriculture, and $128.6 million from the movement in liveweight market prices. Over their lifecycle, market prices of cattle are expected to fluctuate and the value at the time of sale or processing may be higher or lower than the market valuation disclosed in the financial statements, which represents the fair value at a point in time.

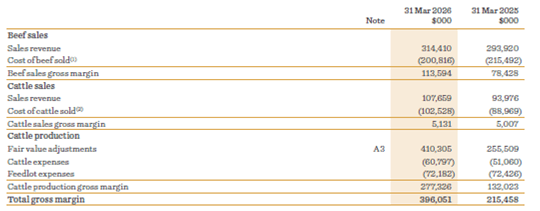

A2 Gross Margin

Gross margin represents value added through the production chain. Margin is achieved through sales of beef products and cattle, as well as cattle production (pastoral and feedlot).

(1) Includes the transfer of cattle at the applicable fair value at the time they leave the property gate en route to a processing plant.

(2) Represents the fair value of the cattle at the time of live sale, which equates to the recorded fair value less costs to sell.

A3 Livestock

(1) As a biological asset, AASB 141 Agriculture requires livestock to be valued at fair value less costs to sell at all times prior to sale or harvest. As such, market value movements occur through changes in fair value rather than sales margin.

(2) Biological transformation, in accordance with AASB 141 Agriculture, includes reclassification of an animal as it moves from being a branded calf, grows, ages, and progresses through the various stages to become a trading or production animal.

(3) Due to the Northern Queensland flood event in January 2026, the Company recognised an additional attrition reflecting the market value of expected livestock losses in this significant event. Refer note A1 for more information.

Accounting Policies – Livestock

Livestock is measured at fair value less costs to sell, with any change recognised in the income statement. Costs to sell include all costs that would be necessary to sell the assets, including freight and direct selling costs.

The fair value of livestock is based on its present location and condition. If an active or other effective market exists for livestock in its present location and condition, the quoted price in that market is the appropriate basis for determining the fair value of that asset. Where the Company has access to different markets, then the most relevant market is used to determine fair value. The relevant market is defined as the market for which “access is available to the entity”, to be used at the time the fair value is established.

If an active market does not exist, then one of the following is used in determining fair value, in the below order:

- the most recent market transaction price, provided that there has not been a significant change in economic circumstances between the date of that transaction and the end of the reporting period;

- market prices, in markets accessible to us, for similar assets with adjustments to reflect differences; or

- sector benchmarks.

In the event that market determined prices or values are not available for livestock in its present condition, the present value of the expected net cash flows from the asset discounted at a current market determined rate may be used in determining fair value.

Livestock are classified as Current and Non-Current. Current livestock are trading cattle and feedlot cattle with less than a year remaining in the feedlot at the end of the financial year, as these animals are due to be sold or processed within the next 12 months. Non-Current livestock are the commercial and stud breeding herd, calves, and feedlot cattle with over a year remaining in the feedlot at end of financial year.

Livestock fair value

At the end of each reporting period, livestock is measured at fair value less costs to sell. The fair value is determined through market price movements and changes in the weight of the herd due to growth, attrition, natural increase, beef transfers or sale.

The net increments or decrements in the market value of livestock are recognised as either gains or losses in the profit or loss, determined as:

- The difference between the total fair value of livestock recognised at the beginning of the financial year and the total fair value of livestock recognised as at the reporting date; less

- Costs expected to be incurred in realising the market value (including freight and selling costs).

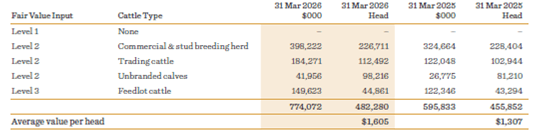

Fair Value Inputs are summarised as follows:

- Level 1 Price Inputs – are quoted prices (unadjusted) in active markets for identical assets or liabilities that can be accessed at the measurement date.

- Level 2 Price Inputs – are inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices).

- Level 3 Price Inputs – are inputs for the asset or liability that are not based on observable market data (unobservable inputs).

(1) Unbranded calves are assessed at each reporting date based on information available at the time. The Company does not track individual calves until such time as they have been branded and recorded in the livestock management system.

D Financial Risk Management (extract)

D3 Commodity Price Risk

Transactional commodity price risk exists in the sale of cattle and beef. Other commodity price exposures include feed inputs for our feedlot operations and operational costs such as fuel.

Price risks are managed, where possible, through forward sales of boxed beef for a period of up to six months. Forward sales contracts for boxed beef are classified as non-derivative and are not required to be fair valued. Revenues derived from these forward sales are recognised in accordance with the Company’s revenue recognition policy for beef sales disclosed at note G3 (r).

For feedlot commodities, price risk is mitigated where possible through internal production, on-site storage & entering into forward purchase contracts. Purchases of commodities may be for a period of up to 12 months. As at 31 March 2026, stock on hand was approximately 22% (31 March 2025: 26%) of our expected grain & roughage usage for the coming 12 months and forward purchases for approximately 70% (31 March 2025: 46%) of our expected grain & roughage purchases for the coming 12 months. These forward purchases include expected internal supply. Without internal supply, forward purchases accounted for approximately 38% (31 March 2025: 6%) of our expected grain & roughage purchases for the coming 12 months. These contracts are entered into and continue to be held for the purpose of grain purchase requirements; they are classified as non-derivative and are not required to be fair valued.

E1 Commitments

We have entered into forward purchase contracts for $33.9 million worth of grain commodities as at 31 March 2026 (31 March 2025: $17.0 million). There are no forward purchase contracts for cattle as at 31 March 2026 (31 March 2025: no forward purchase contracts). All forward contracts are expected to be settled within 12 months from the balance date.

Capital expenditure of $7.1 million has been contracted in respect of property, plant and equipment as at 31 March 2026 (31 March 2025: $11.3 million).

Operating and Financial Review (extract)