Sony Group Corporation – Annual report – 31 March 2022

Industry: manufacturing

2. Basis of preparation (extract)

Compliance with International Financial Reporting Standards

The consolidated financial statements of Sony have been prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). The term “IFRS” also includes International Accounting Standards (IASs) and the related interpretations of the interpretations committees (Standard Interpretations Committee (SIC) and International Financial Reporting Interpretations Committee (IFRIC)).

Sony adopted IFRS for the first time this fiscal year (commencing on April 1, 2021 and ending on March 31, 2022), and so the annual consolidated financial statements for this fiscal year are the first ones prepared in conformity with IFRS. The date of Sony’s transition to IFRS is April 1, 2020. Sony has adopted IFRS 1 “First-Time Adoption of International Financial Reporting Standards” (“IFRS 1”) for the transition to IFRS.

The effect of the transition to IFRS on Sony’s financial position, results of operations and cash flows is presented in Note 34.

34. First-time adoption

Sony has adopted IFRS from the first quarter of the fiscal year ended March 31, 2022. The latest consolidated financial statements under U.S. GAAP were prepared for the fiscal year ended March 31, 2021, and the date of transition to IFRS was April 1, 2020.

(1) Exemption under IFRS 1

IFRS 1 requires that a company adopting IFRS for the first-time (“first-time adopters”) shall apply IFRS retrospectively. However, IFRS 1 provides certain exemptions that allow first-time adopters to choose not to apply certain standards retrospectively. Sony has adopted the following exemptions:

Business combinations

First-time adopters may choose not to apply IFRS 3 “Business Combinations” (“IFRS 3”) retrospectively to business combinations that occurred before the date of transition to IFRS. Sony has applied this exemption and chosen not to apply IFRS 3 retrospectively to business combinations that occurred before the date of transition to IFRS. Therefore, the carrying amounts of goodwill generated in business combinations that occurred prior to the date of transition to IFRS were based on the carrying amounts determined under U.S. GAAP at the date of transition to IFRS.

Sony performed an impairment test on goodwill at the date of transition to IFRS regardless of whether there were any indications that the goodwill may be impaired, refer to Note 3 I. Significant accounting policies (10).

Exchange differences on translating foreign operations

First-time adopters may choose to deem the cumulative exchange differences on translating foreign operations as zero at the date of transition to IFRS. Sony has chosen to apply this exemption and deemed all cumulative exchange differences on translating foreign operations as zero at the date of transition to IFRS.

Designation of financial instruments recognized before the date of transition to IFRS

First-time adopters may designate an investment in an equity instrument as an investment recognized at fair value through other comprehensive income in accordance with IFRS 9 “Financial Instruments” based on the facts and circumstances that existed at the date of transition to IFRS. Sony has applied this exemption and designated some equity instruments at fair value in other comprehensive income at the date of transition to IFRS.

Recognition of ROU assets and lease liabilities

When first-time adopters recognize ROU assets and lease liabilities as a lessee, they are permitted to measure ROU assets and lease liabilities at the date of transition to IFRS. Sony measured all lease liabilities at the date of transition to IFRS at the present value of the remaining lease payments, discounted using Sony’s incremental borrowing rate at the date of transition to IFRS. Sony recognized ROU assets equal to the amount of lease liabilities at the date of transition to IFRS.

(2) Mandatory exception under IFRS 1

IFRS 1 prohibits the retrospective application of IFRS concerning “estimates,” “non-controlling interests,” “classification and measurement of financial instruments” and other items. Sony applied these items prospectively from the date of transition to IFRS.

(3) Reconciliation

The reconciliations required to be disclosed in the first IFRS financial statements are described in the reconciliations as below. “Reclassification” includes items that do not affect retained earnings and comprehensive income, while “Recognition and measurement differences” includes items that affect retained earnings and comprehensive income.

Reconciliation of equity at the date of transition to IFRS (April 1, 2020)

Reconciliation of equity as of March 31, 2021

Reconciliation of profit or loss for the fiscal year ended March 31, 2021

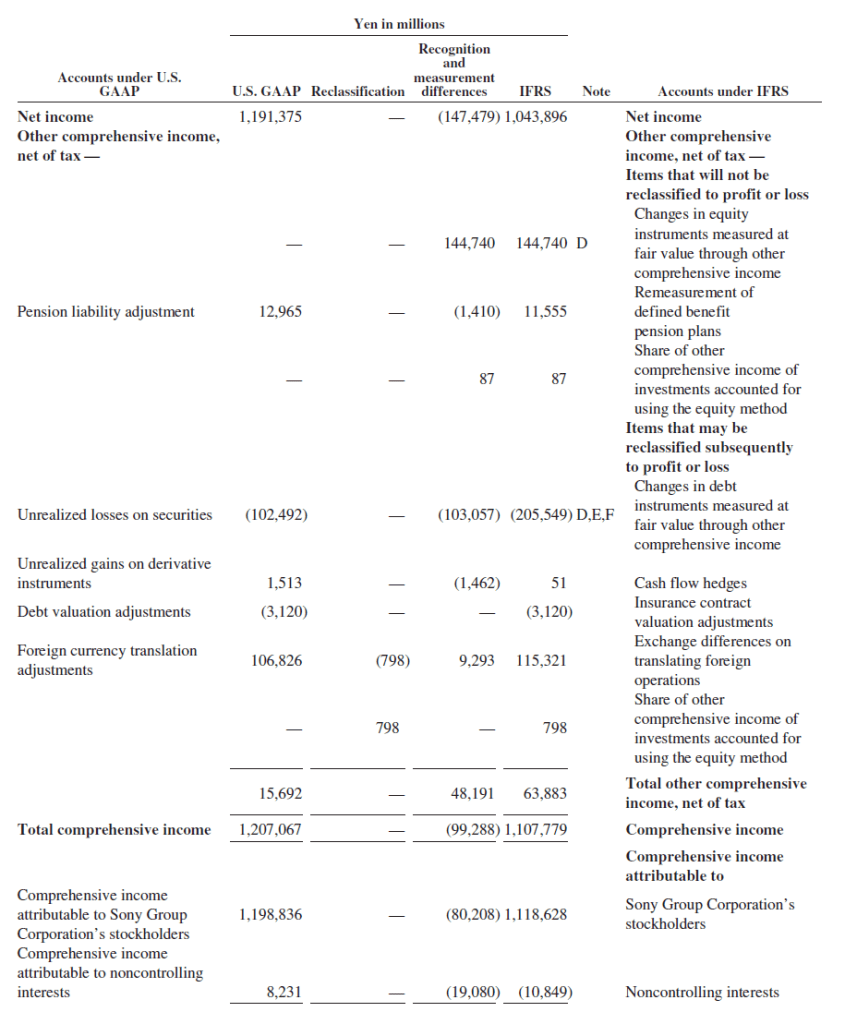

Reconciliation of comprehensive income for the fiscal year ended March 31, 2021

(4) Notes to reconciliation

Reclassifications

a. “Marketable securities,” which were separately presented under U.S. GAAP, have been reclassified into “Investments and advances in the Financial Services segment” as current assets under IFRS. Investments held for variable annuities and variable life insurance contracts in the life insurance business, which were included in “Marketable securities” under U.S. GAAP, have been reclassified into “Investments and advances in the Financial Services segment” as current assets or non-current assets under IFRS, after considering the current/non-current distinction based on the purpose of the investments related to the insurance liabilities in accordance with paragraph 66 of IAS 1 “Presentation of Financial Statements” (“IAS 1”).

b. “Notes and accounts receivable, trade and contract assets” and “Allowance for credit losses,” which were separately presented under U.S. GAAP, have been reclassified into “Trade and other receivables, and contract assets” under IFRS.

c. “Other receivables,” which were separately presented under U.S. GAAP, have been reclassified into “Trade and other receivables, and contract assets” under IFRS.

d. “Other financial assets,” which were included in “Prepaid expenses and other current assets” under U.S. GAAP, are separately presented under IFRS.

e. “Film costs,” which were presented separately, and music catalogs, artist contracts, music distribution rights and other content assets, which were included in “Intangibles, net” under U.S. GAAP are collectively reclassified and presented as “Content assets” under IFRS. “Intangibles, net” other than those reclassified and presented as “Content assets” have been reclassified into “Other intangible assets” under IFRS.

f. “Securities investments and other,” which were separately presented under U.S. GAAP, have been reclassified into “Investments and advances in the Financial Services segment” as non-current assets for the amounts related to the Financial Services segment and “Other financial assets” as non-current assets for the amounts related to all segments excluding the Financial Services segment under IFRS. Housing loans in the banking business, which were included in “Securities investments and other” under U.S. GAAP, have been reclassified into “Investments and advances in the Financial Services segment” as current assets or non-current assets under IFRS after considering the current/non-current distinction based on the terms of the contract in accordance with paragraph 66 of IAS 1.

g. “Operating lease right-of-use assets” and “Finance lease right-of-use assets,” which were separately presented under U.S. GAAP, have been reclassified into “Right-of-use assets” under IFRS.

h. “Other financial assets,” which were included in “Other” in other assets under U.S. GAAP, are separately presented under IFRS.

i. “Current portion of long-term operating lease liabilities” and “Long-term operating lease liabilities,” which were separately presented under U.S. GAAP, have been reclassified into “Current portion of long-term debt” and “Long-term debt,” respectively under IFRS.

j. “Notes and accounts payable, trade,” which were separately presented under U.S. GAAP, have been reclassified into “Trade and other payables” under IFRS.

k. “Accounts payable, other and accrued expenses,” which were separately presented under U.S. GAAP, have been reclassified into either “Trade and other payables,” “Participation and residual liabilities in the Pictures segment,” “Other financial liabilities” or “Other current liabilities” under IFRS.

l. “Deposits from customers in the banking business,” which were separately presented under U.S. GAAP, have been reclassified into “Other financial liabilities” of non-current liabilities under IFRS, after considering the current/non-current distinction based on the terms of the contract in accordance with paragraph 69 of IAS 1.

m. “Trade and other payables” and “Other financial liabilities,” which were included in current liabilities “Other” under U.S. GAAP, are separately presented under IFRS.

n. “Participation and residual liabilities in the Pictures segment” and “Other financial liabilities,” which were included in “Other” in other than current liabilities under U.S. GAAP, are separately presented under IFRS.

o. “Redeemable noncontrolling interest,” which was separately presented under U.S. GAAP, has been reclassified into “Other financial liabilities” under IFRS.

p. Under U.S. GAAP, securities received as collateral other than cash in lending transactions are accounted for as “Marketable securities” and also as “Other current liabilities” representing Sony’s obligation to return the collateral, which was 373,274 million yen as of March 31, 2021. Under IFRS, the securities received as collateral other than cash shall be recognized in the consolidated statements of financial position if they are sold or the transferor defaults. None of the securities was recognized in the consolidated statements of financial position as of March 31, 2021.

q. “Other operating revenue,” which was separately presented under U.S. GAAP, has been reclassified into “Sales” under IFRS.

r. Under IFRS, “Financial services revenue” and “Financial services expenses” have increased by the same amount due to the gross up of revenue and expenses related to service transactions, based on the presentation requirements.

s. Under IFRS, “Financial income” and “Financial expenses” have been presented separately, based on the presentation requirements.

Recognition and measurement differences

A. Exchange differences on translating foreign operations

Under IFRS 1, first-time adopters may choose to deem the cumulative exchange differences on translating foreign operations as zero at the date of transition to IFRS. Sony has chosen to apply this exemption and transferred all cumulative exchange differences on translating foreign operations into retained earnings at the date of transition to IFRS.

The impact of this change is as follows:

B. Post-employment benefits

Under U.S. GAAP, past service costs and actuarial gains and losses are deferred in accumulated other comprehensive income, and subsequently reclassified to profit or loss over a certain period of time in the future.

Under IFRS, past service costs are expensed as incurred. Adjustments due to remeasurements of the net defined benefit liabilities or assets, such as actuarial gains and losses, are recognized in other comprehensive income when incurred and immediately transferred to retained earnings and are not reclassified to profit or loss in a subsequent period.

In addition, if the fair value of plan assets is in excess of the present value of defined benefit obligations, the amount of any asset to be recognized is limited to the present value of any economic benefits available in the form of refunds from the plan or reductions in the future contributions to the plan.

The impact of this change before considering the tax effect is as follows:

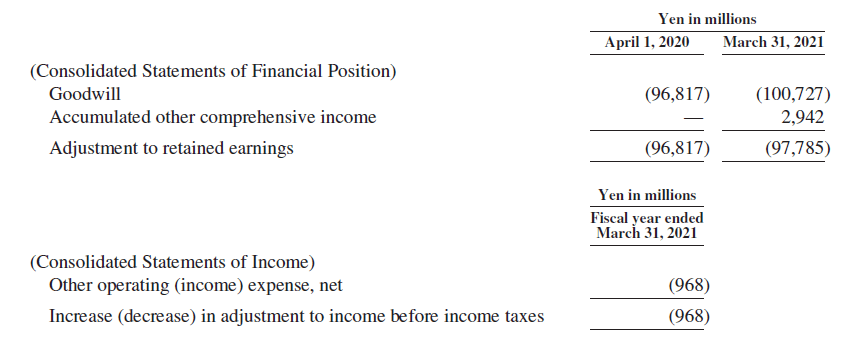

C. Impairment of goodwill

The level at which goodwill is tested for impairment differs between U.S. GAAP and IFRS. Under U.S. GAAP, goodwill is tested for impairment at the reporting unit level. Reporting units are Sony’s operating segments or one level below the operating segments. The identification of reporting units is dependent on the level at which discrete financial information is available and regularly reviewed by the segment manager. Under IFRS, goodwill is tested for impairment at the level of the CGU or group of CGUs, which represent the lowest level at which goodwill is monitored for internal management purposes, which may be a lower level of grouping than a reporting unit under U.S. GAAP. A CGU is the smallest identifiable group of assets that generates cash inflows that are largely independent of the cash inflows from other assets or group of assets.

Upon the transition to IFRS, Sony assessed its reporting units to determine if such reporting units should be further divided into several CGUs under IFRS. As a result, Sony determined that certain CGUs should be grouped at a lower level than a reporting unit under U.S. GAAP. In addition, Sony performed an impairment test for goodwill at the date of transition to IFRS regardless of whether there were any indications that the goodwill may be impaired based on conditions at the date of transition to IFRS. In performing the impairment test, Sony used the goodwill balance under U.S. GAAP attributed to each CGU or group of CGUs based on the history of acquisitions of the businesses. Under U.S. GAAP, when a business within a reporting unit was disposed of (including when classified as held for sale), goodwill was allocated to the remaining business and the disposed business based on relative fair value, and only the goodwill allocated to the disposed business was written off. Under IFRS, since certain disposed businesses represented individual CGUs or a group of CGUs, at the time of disposition, all the goodwill that was recognized for such businesses would have been written off. The assessment resulted in impairments related to CGUs or groups of CGUs of businesses that Sony disposed of prior to the date of transition to IFRS. In addition, the assessment resulted in impairments related to CGUs or groups of CGUs of businesses that existed at the date of transition to IFRS where the recoverable amount was lower than the carrying amount.

As a result, at the date of transition to IFRS, goodwill decreased by 96,817 million yen, and retained earnings decreased by the same amount. The impact of this change was primarily in the I&SS and Pictures segments and is discussed below.

In the I&SS segment, at the date of transition to IFRS, Sony recognized 43,376 million yen of impairment losses in retained earnings, which includes the impairment loss related to the goodwill allocated to CGUs or groups of CGUs of businesses that Sony disposed of prior to the date of transition to IFRS as well as the Internet of Things (“IoT”)-related business, which existed at the date of transition to IFRS. The recoverable amount of the IoT-related business was determined by the value in use and a pre-tax discount rate of 9.8% was used in the measurement.

In the Pictures segment, at the date of transition to IFRS, Sony recognized 48,749 million yen of impairment losses in retained earnings, which includes the impairment loss related to the goodwill allocated to CGUs or groups of CGUs of businesses that Sony disposed of prior to the date of transition to IFRS as well as the United States television network CGU, which existed at the date of transition to IFRS. The recoverable amount of the United States television network CGU was determined by the value in use and a pre-tax discount rate of 15.9% was used in the measurement.

The impact of this change is as follows:

D. Equity instruments and debt instruments

Under U.S. GAAP, equity securities are recognized at fair value and subsequent changes in fair value are recognized in profit or loss. Equity securities that do not have readily determinable fair values are measured at cost minus impairment, if any, plus or minus changes resulting from observable price changes in orderly transactions for the identical or a similar investment of the same issuer.

Additionally, under U.S. GAAP, debt securities that are held-to-maturity, primarily in the life insurance business, are carried at amortized cost.

Under IFRS, equity instruments are recognized at fair value and subsequent changes in fair value are recognized in profit or loss. However, for investments in equity instruments which are not held for trading, Sony may make an irrevocable election at initial recognition to present subsequent changes in fair value of the investments in other comprehensive income. Such financial assets are measured at fair value and subsequent changes in the fair value are recognized in other comprehensive income.

Additionally, under IFRS, debt instruments, which are primarily in the life insurance business, are classified as financial assets measured at fair value through other comprehensive income if the debt instruments are held within a business model whose objective is achieved by both collecting contractual cash flows and selling the financial assets and the contractual terms of the financial assets give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. Changes in the fair value of the financial assets after initial recognition, except for impairment gains or losses and foreign exchange gains or losses, are recognized in other comprehensive income.

The impact of this change before considering the tax effect is as follows:

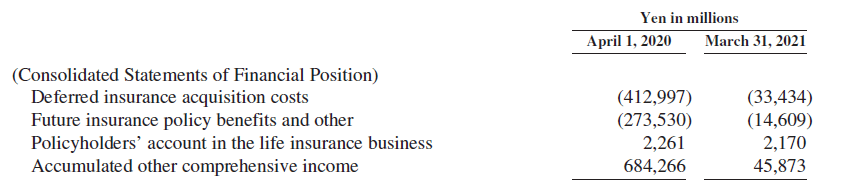

E. Insurance-related accounts

In accordance with Sony’s first-time adoption of IFRS 4 at the date of transition to IFRS, insurance contracts are recognized and measured based on the same accounting principles previously applied under U.S. GAAP. Under IFRS, the amount of insurance-related accounts was affected by shadow accounting in the life insurance business as a result of the increase in financial instruments to be measured at fair value through other comprehensive income. This change is mainly because the shadow liability adequacy test indicated that the insurance liabilities were not recorded at a sufficient level at the date of transition to IFRS.

The impact of this change before considering the tax effect is as follows:

F. Impact of changes in the measurement method of debt instruments in the life insurance business on deferred tax liabilities and noncontrolling interests

In connection with “D. Equity instruments and debt instruments” and “E. Insurance-related accounts,” accumulated other comprehensive income is affected due to the change in the measurement method of debt instruments in the life insurance business and the change in the amount of insurance-related accounts as a result of the application of shadow accounting.

The impact of this change on deferred tax liabilities and noncontrolling interests is as follows:

G. Retained earnings

The main items causing the differences in retained earnings are as follows:

H. Income before income taxes

The main items causing the differences in income before income taxes are as follows:

I. Income taxes

Due to the adoption of IFRS, income taxes have been adjusted by recording the tax effects on various IFRS adjustments recognized and measured, and other IFRS tax effects.

(5) Reconciliation of consolidated statements of cash flows

The main items causing the differences in the consolidated statements of cash flows are as follows:

*1 Principal payments for operating lease liabilities

Under U.S. GAAP, lessees classify leases as either operating leases or finance leases, and the principal payments for the operating lease liabilities are classified as cash flows from operating activities in the consolidated statements of cash flows. Under IFRS, the distinction between operating leases and finance leases no longer exists for lessees, and all of the principal payments for lease liabilities are classified as cash flows from financing activities in the consolidated statements of cash flows.

*2 Additions and disposals of content assets

Under U.S. GAAP, Sony classified the cash flows from the additions and disposals of film costs as cash flows from operating activities, and classified the cash flows from the additions and disposals of music catalogs, artist contracts, music distribution rights and other content assets as cash flows from investing activities in the consolidated statements of cash flows based on the nature of such transactions as additions and disposals of intangible assets. Under IFRS, Sony defines these intangible assets as content assets, and classifies the cash flows from the additions and disposals of content assets as cash flows from operating activities in the consolidated statements of cash flows except for additions and disposals of content assets from business combinations or business divestitures, because the additions and disposals of content assets are derived from the principal revenue-producing activities of Sony.

*3 Changes in assets and liabilities in the Financial Services segment

Under U.S. GAAP, Sony classified cash flows from changes in investments and advances in the Financial Services segment and repurchase agreements in the Financial Services segment, deposits from customers in the banking business and policyholders’ account in the life insurance business according to the nature of these transactions in the consolidated statements of cash flows. Under IFRS, Sony classifies cash flows from these transactions as cash flows from operating activities in the consolidated statements of cash flows as these transactions are viewed as integral to the principal revenue-producing activities of Sony.