AB Akola Group – Annual report – 30 June 2025

Industry: agriculture

All amounts in thousands of euros, unless otherwise stated

2. Material accounting policies (extract)

2.11. Biological assets

The Group’s biological assets include animals and livestock, poultry, and crops.

Animals and livestock are accounted for at fair value less costs to sell. The fair value of milking cows is measured using discounted cash flows method (level 3). Other livestock is measured at comparable market prices (level 2).

Poultry is accounted for at fair value less costs to sell. The fair value of poultry is measured based on future value of chickens/meat broilers/eggs less costs to maintain (level 3).

Crops are accounted for at fair value less costs to sell. The fair value of crops is measured at comparable market prices based on expected yield (level 3).

Agricultural produce harvested from an entity’s biological assets is measured at its fair value less estimated costs to sell at the point of harvest. The measured value of the harvested yield is then considered to be the cost of inventories.

As at 30 June 2025 and 30 June 2024, the management of the Group treats all animals and livestock (excluding eggs and broilers) as non – current assets and all crops, eggs and broilers as current.

All changes in fair value of biological assets were accounted for under cost of sales caption in the statements of profit (loss) and other comprehensive income.

2.18. Fair value measurement

All assets and liabilities for which fair value is measured or disclosed in the financial statements are categorized within the fair value hierarchy, described as follows, based on the lowest level input that is significant to the fair value measurement as a whole:

- Level 1 – Quoted (unadjusted) market prices in active markets for identical assets or liabilities.

- Level 2 – Valuation techniques for which the lowest level input that is significant to the fair value measurement is directly or indirectly observable.

- Level 3 – Valuation techniques for which the lowest level input that is significant to the fair value measurement is unobservable.

For assets and liabilities that are recognized in the financial statements on a recurring basis, the Group determine whether transfers have occurred between levels in the hierarchy by re – assessing categorization (based on the lowest level input that is significant to the fair value measurement as a whole) at the end of each reporting period.

Valuations are performed by the Group’s management at each reporting date. For the purpose of fair value disclosures, the Group and the Company have determined classes of assets and liabilities based on the nature, characteristics and risks of asset or liability and the level of the fair value hierarchy as explained above.

2.20. Use of significant accounting judgments and estimates in the preparation of financial statements (extract)

Significant accounting estimates (extract)

Valuation of biological assets

As at 30 June 2025 and 30 June 2024, the Group did not have an independent appraisal of its biological assets. According to IFRS, such assets must be recorded at fair value. Biological assets mostly consist of three groups: animals and livestock, poultry and crops which are accounted for at fair value less costs to sell (Note 2.11).

The fair value of biological assets of the Group is determined on a recurring basis. The management determines key assumptions based on historical figures and the best estimate as at the reporting date. Applied unobservable assumptions are challenged on a regular basis and adjusted after back testing is performed. Other observable inputs used are based on publicly available sources (prices in the market). The management of the Group constantly analyses the changes in fair value and assesses what has the biggest influence on it – quantity produced, sales prices and etc.

Animals and livestock are valued in two ways: milking cows are valued using discounted cash flows method less costs to sell (level 3) and other groups of livestock at market prices less cost to sell at the reporting date (level 2). Crops are valued at market prices based on expected yield less costs to sell at the reporting date (level 3).

Poultry are valued in the following way: hatching chicken are valued based on the future value of the produced eggs less costs to maintain the chicken until end of its production period, slaughter costs as well as costs to sell at the reporting date (level 3). Meat broilers are valued based on average age of the chicken and its respective market value between the value range of day one and value at the moment of slaughtering the chicken (level 3).

- Milking cows

The Group’s management estimates the fair value of dairy cows using the discounted cash flow method because there is no active and reliable market for this type of cattle and this valuation method is the most accurate estimate of the fair value of dairy cows.

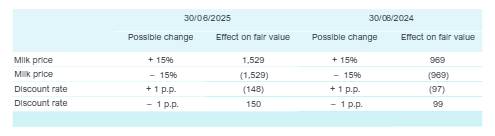

As at 30 June 2025, the main assumptions used to determine the fair value of the dairy cows are the expected selling prices of milk over the useful life of the dairy cow used to calculate the future net revenue streams (for the years ending 30 June 2026 and 30 June 2027: EUR 0.500 and EUR 0.500, respectively), which have been determined on the basis of publicly available mid – market prices and the pre – tax discount rate before income tax (7.20%).

As at 30 June 2024, the main assumptions used to determine the fair value of the dairy cows are the expected selling prices of milk over the useful life of the dairy cow used to calculate the future net revenue streams (for the years ending 30 June 2025 and 30 June 2026: EUR 0.427 and EUR 0.427, respectively), which have been determined on the basis of publicly available mid – market prices and the pre – tax discount rate before income tax (8.96%).

The following table demonstrates the sensitivity of the fair value of milking cows to a reasonably possible change in key assumptions and its effect on profit or loss. There is no effect to other comprehensive income.

- Crops

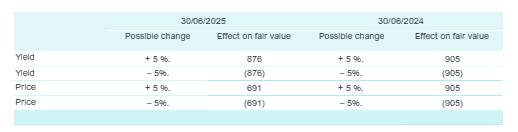

As at 30 June 2025 and 2024, the key assumptions used to determine fair value of crops are the estimated yield ranges depending on the type of crops (2.40– 10.6 tons/ha for grain cultures and 60 – 65 tons/ha for beet cultures for the year ending 30 June 2025 and 2.48– 10.0 tons/ha for grain cultures and 60 – 70 tones/ha for beet cultures for the year ending 30 June 2024) and the expected sales price, which was based on the estimated future grain, oilseeds and beet cultures sales price of the deliveries taking place September – December of the respective year.

The following table demonstrates the sensitivity of the fair value of crops to a reasonably possible change in key assumptions and its effect on profit or loss. There is no effect to other comprehensive income.

- Poultry

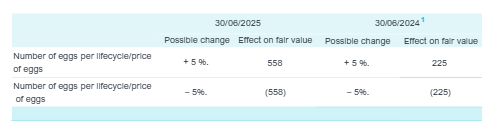

As at 30 June 2025 and 30 June 2024, the main assumptions used to determine fair value of hatching chicken are the price of the incubation eggs (EUR 0.35 for the unit; EUR 0.24 – 0.32 for the unit in previous financial year) which was estimated based on publicly available yearly average market price and the average number of hatching eggs produced per hatching chicken in the lifetime 170.8 units for financial year (179 units – previous financial year).

The following table demonstrates the sensitivity of the fair value of hatching chickens to a reasonably possible change in key assumptions and its effect on profit or loss. There is no effect to other comprehensive income.

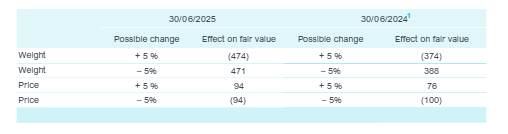

As at 30 June 2025, the main assumptions used to determine fair value of broilers are the market price of chickens from EUR 0.416 to EUR 0.42 for 1 day old and EUR 2.04 for 36 days old and EUR 1.09 for 37.7 days and 38.2 days old (from EUR 0.45 to EUR 0.57 for 1 day old and EUR 1.60 for 36 days old and EUR 1.59 for 38 days old as at 30 June 2024) which was estimated based on actual purchases/sales taking place close to the 30 June 2025 and broiler weight from 2.45 to 2.48 kg as at 37.7 days old and 38.2 days old respectively (as at 30 June 2024 – from 2.28 to 2.48 kg as at 36 days old and 38 days old).

1Comparative information has been restated to better reflect the model’s sensitivity to changes in key assumptions.

The following table demonstrates the sensitivity of the fair value of broilers to a reasonably possible change in key assumptions and its effect on profit or loss. There is no effect to other comprehensive income:

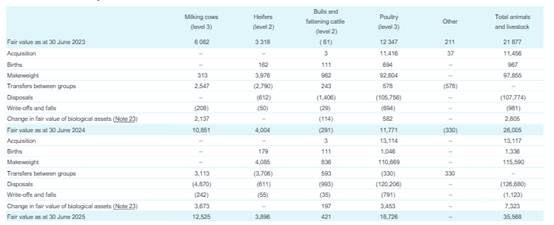

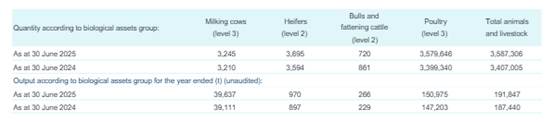

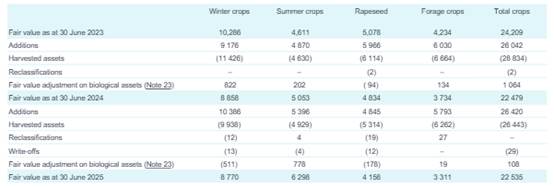

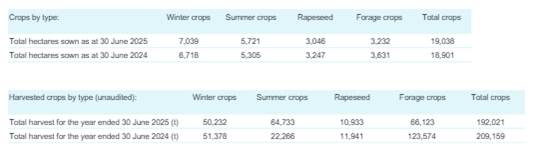

8. Biological assets

Management determined key assumptions and their sensitivity used in biological assets valuation presented in Note 2.20.

Fair value of the Group’s animals and livestock

As at 30 June 2025, part of poultry amounting to EUR 11,307 thousand is presented as current assets (EUR 9,563 thousand as at 30 June 2024).

Fair value of the Group’s crops (level 3):

During the years ended 30 June 2025 and 30 June 2024, there were no transfers between the different levels of fair value hierarchy.

As at 30 June 2025, part of animals and livestock of the Group with the carrying value of EUR 5,910 thousand (as at 30 June 2024 – EUR 4,845 thousand) were pledged to banks as a collateral for the loans (Note 17).

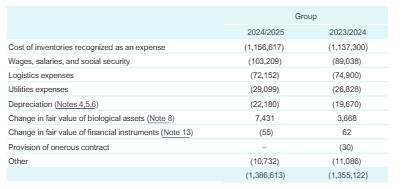

23. Cost of sales

30. Financial assets and liabilities and risk management (extract)

Strategy for managing financial risks arising from biological assets

The Group is engaged in wholesale trade of milk, therefore, is exposed to risks arising from changes in milk prices. The Group’s wholesale agreements for milk not related with financial instruments but represent a significant price risk. The Group does not anticipate that milk prices will be in prolonged decline in the foreseeable future (at current period price increase noted) and, therefore, has not entered into derivative or other contracts to manage the risk of the decline in milk prices. The Group reviews its outlook for milk prices regularly in considering the need for active risk management.

Strategy for managing financial risks arising from derivative instruments

- Derivatives not designated as hedging instruments

The Group uses foreign exchange forward and swap contracts to manage some of its transaction exposures. The foreign exchange forward contracts are not designated as cash flow hedges and are entered into for periods consistent with foreign currency exposure of the underlying transactions, generally from one to 12 months.

- Derivatives designated as hedging instruments

- Fair value hedges

- Commodity price risk

The Group purchases/sells agriculture production on an ongoing basis as some contracts have a fixed purchase price. Some of such contracts are not covered with a fixed price. As grains are commodities, the prices of them are largely determined by the market, thus, the Sellers and the Buyers of grain negotiate and set the sales price close to the market price, however, if the price is set using variable method the Sellers are responsible for choosing when to fix the MATIF price. MATIF a commodity exchanged which provides the floating rates for grain.

To manage the emerging risk of price fluctuations, the Group has entered into MATIF futures contracts, which the Group trades on the stock exchange NYSE Euronext Paris SA. To hedge the risk of rapeseed oil and rapeseed meal prices, the Group uses over-the-counter transactions, which traded on the over-the-counter markets of Rotterdam and Neuss Spyck.

These contracts, are expected to reduce the volatility attributable to price fluctuations of grains trade. Hedging the price volatility of forecast grains purchases/sales is in accordance with the risk management strategy outlined by the Group.

There is an economic relationship between the hedged items and the hedging instruments as the terms of commodity forward contracts match the terms of the expected highly probable forecast transactions (i.e., notional amount and expected payment date). The Group has established a hedge ratio of 1:1 for the hedging relationships as the underlying risk of the commodity forward contracts are identical to the hedged risk components. To test the hedge effectiveness, the Group uses the hypothetical derivative method and compares the changes in the fair value of the hedging instruments against the changes in fair value of the hedged items attributable to the hedged risks.

Hedging inefficiencies can arise from:

- Different indexes (and accordingly different curves) linked to the hedged risk of the hedged items and hedging instruments;

- Differences in timing of cash flows of the hedged item and hedging instrument;

- The counterparties’ credit risk differently impacting the fair value movements of the hedging instrument and hedged item.

For more information see Note 13.

- Cash flow hedges

- Commodity price risk

The Group purchases grains and gas needed for its manufacturing process of various products: combined feed, flour, poultry and other. In grain and gas market, when concluding purchase contracts, the prices are not known and change until they are fixed. The MATIF values are used when determining grain prices. To manage the emerging risk of grain price fluctuations, the Group has entered into MATIF futures contracts. To manage the emerging risk of gas price fluctuations, the Group has entered into gas future contracts. The Group uses a layering tactic where price fixing is done for the planned quantity in parts (in parts, 5% – 10% of the total amount). The insured object is future cash flows for energy for expenses. As the Group carries out and plans to continue to carry out production activities, it can estimate future energy needs.

These grains and gas future contracts are expected to reduce the volatility attributable to price fluctuations of grains and gas in Group manufacturing process. Hedging the price volatility of forecast grains and gas purchases is in accordance with the risk management strategy outlined by the Group.

There is an economic relationship between the hedged items and the hedging instruments as the terms of commodity forward contracts match the terms of the expected highly probable forecast transactions (i.e., notional amount and expected payment date). The Group has established a hedge ratio of 1:1 for the hedging relationships as the underlying risk of the commodity forward contracts are identical to the hedged risk components. To test the hedge effectiveness, the Group uses the hypothetical derivative method and compares the changes in the fair value of the hedging instruments against the changes in fair value of the hedged items attributable to the hedged risks.

Hedging inefficiencies can arise from:

- Differences in the timing of the cash flows of the hedged items and the hedging instruments;

- Different indexes (and accordingly different curves) linked to the hedged risk of the hedged items and hedging instruments;

- The counterparties’ credit risk differently impacting the fair value movements of the hedging instruments and hedged items;

- Changes to the forecasted amount of cash flows of hedged items and hedging instruments.

For more information see Note 13.

Market price risk

The Group is exposed to the grain market price risk which is managed with the hedge accounting described in Note 13.

13. Other financial assets and derivative financial instruments (extract)

The Group concludes forward agreements with fixed price with Lithuanian and Latvian agricultural production growers for purchase/sale of agricultural produce. For part of such agreements the Group does not have agreed sales/purchases contracts with fixed price.

As at 30 June 2025 and 30 June 2024, to hedge the arising risk of price fluctuations for the total amount of such unutilized purchase or sales commitments the Group concluded futures contracts that are traded on NYSE Euronext Paris SA exchange.

The Group hedges the risk of rapeseed oil and rapeseed meal price fluctuations by entering into over-the-counter (OTC) contracts traded in the Rotterdam and Neuss Spyck markets.

There is an economic relationship between the hedged items and the hedging instruments as the terms of the forward agreement match the terms of the commodity future contract (i.e., notional amount and expected payment date). The Group has established a hedge ratio of 1:1 for the hedging relationships as the underlying risk of the commodity future contracts are identical to the hedged risk components. To test the hedge effectiveness, the Group uses the hypothetical derivative method and compares the changes in the fair value of the hedging instruments against the changes in fair value of the hedged items attributable to the hedged risks.

The hedge ineffectiveness can arise from:

- Differences in the timing of the cash flows of the hedged items and the hedging instruments;

- The counterparties’ credit risk differently impacting the fair value movements of the hedging instruments

- Changes to the forecasted amount of cash flows of hedged items and hedging instruments