Mercedes-Benz Group AG – Annual report – 31 December 2023

Industry: automotive

Accounting policies (extract)

Impairment of financial assets

At each reporting date, an impairment is recognized for financial assets, loan commitments and financial guarantees other than those to be measured at fair value through profit or loss reflecting expected credit losses for these instruments. Impairments are allocated using a three stage approach to expected credit losses:

Stage 1: expected credit losses within the next twelve months

Stage 1 includes all contracts with no significant increase in credit risk since initial recognition and usually includes new acquisitions and contracts with fewer than 31 days past due date. The portion of the lifetime expected credit losses resulting from default events possible within the next 12 months is recognized.

Stage 2: expected credit losses over the lifetime – not credit impaired

If a financial asset has a significant increase in credit risk since initial recognition but is not yet credit impaired, it is moved to stage 2 and measured at lifetime expected credit loss, which is defined as the expected credit loss that results from all possible default events over the expected life of a financial asset.

Stage 3: expected credit losses over the lifetime – credit impaired

If a financial asset is defined as credit-impaired or in default, it is transferred to stage 3. The expected credit loss is recognized as an impairment measured over the expected lifetime of the financial asset. Objective evidence for a credit-impaired financial asset includes 91 days past due date and other information about significant financial difficulties of the debtor.

The determination of whether a financial asset has experienced a significant increase in credit risk is based on an assessment of the probability of default, which is made at least quarterly, incorporating external credit rating information as well as internal information on the credit quality of the financial asset. For debt instruments that are not receivables from financial services, a significant increase in credit risk is assessed mainly based on past-due information or the probability of default.

A financial asset is migrated to stage 2 if the asset’s credit risk has increased significantly compared to its credit risk at initial recognition. The credit risk is assessed based on the probability of default. For trade receivables, the simplified approach is applied whereby all trade receivables are allocated to stage 2 initially. Hence, no determination of significant increases in credit risk is necessary.

The Mercedes-Benz Group applies the low-credit-risk exception to the stage allocation to quoted debt instruments with investment-grade ratings. These debt instruments are always allocated to stage 1.

In stages 1 and 2, the effective interest revenue is calculated based on gross carrying amounts. If a financial asset becomes credit impaired in stage 3, the effective interest revenue is calculated based on its net carrying amount (gross carrying amount adjusted for any loss allowance).

Measurement of expected credit losses

Expected credit losses are measured in a way that reflects:

a) the unbiased and probability-weighted amount;

b) the time value of money;

c) reasonable and supportable information (if available without undue cost or effort) at the reporting date about past events, current conditions and forecasts of future economic conditions.

Expected credit losses are measured as the probability-weighted present value of all cash shortfalls over the expected life of each financial asset. For receivables from financial services, expected credit losses are calculated using a statistical model with three major risk parameters: probability of default, loss given default and exposure at default.

The estimation of these risk parameters incorporates all available relevant information, not only historical and current loss data, but also reasonable and supportable forward-looking information reflected by future expectations. This information includes macroeconomic factors (e.g. gross domestic product growth, unemployment rate, cost performance index) and forecasts of future economic conditions. For receivables from financial services, these forecasts are performed using a scenario analysis (basic scenario, optimistic scenario and pessimistic scenario). The impairment amount for trade receivables is predominantly determined on a collective basis.

A financial instrument is written off when there is no reasonable expectation of recovery in whole or in part, for example, after the end of insolvency proceedings or after a court decision of uncollectibility.

Significant modification of financial assets (e.g. with a change in the present value of the contractual cash flows of 10%) also leads to derecognition of the financial assets with a simultaneous recognition of new financial assets. If the terms of a contract are renegotiated or modified and this does not result in derecognition of the contract, then the gross carrying amount of the contract is recalculated and a modification gain or loss is recognized in profit or loss.

33. Management of financial risks (extract)

General information on financial risks

As a result of its businesses and the global nature of its operations, the Mercedes-Benz Group is exposed to market risks from changes in foreign currency exchange-rates and interest rates, while price risks arise from the procurement of raw materials and energy, for example. An equity price risk results from investments in listed companies. In addition, the Group is exposed to credit risks from its leasing and mainly financing activities and from its business operations (trade receivables). Furthermore, the Group is exposed to country and liquidity risks relating to its credit and market risks or a deterioration of its business operations or financial market disturbances. If these financial risks materialize, they could adversely affect the Group’s profitability, liquidity and capital resources and financial position.

The Mercedes-Benz Group has established internal policies for risk controlling procedures and for the use of financial instruments, including a clear segregation of duties with regard to financial activities, settlement, accounting and the related controlling. The guidelines upon which the Group’s risk management processes for financial risks are based are designed to identify and analyse these risks throughout the Group, to set appropriate risk limits and controls and to monitor the risks by means of reliable and up-to-date administrative and information systems. The guidelines and systems are regularly reviewed and adjusted to changes in markets and products.

The Group manages and monitors these risks primarily through its operating and financing activities and, if required, through the use of derivative financial instruments. The Mercedes-Benz Group uses derivative financial instruments exclusively for hedging financial risks that arise from its business operations or refinancing activities or liquidity management. Without these derivative financial instruments, the Group would be exposed to higher financial risks. Additional information on financial instruments and especially on the volumes of the derivative financial instruments used is included in Note 32. The Mercedes-Benz Group regularly evaluates its financial risks with due consideration of changes in key economic indicators and up-to-date market information.

The market sensitive instruments, including equity and debt securities, that the plan assets hold to finance pension and other post-employment healthcare benefits, are not included in the following quantitative and qualitative analysis. See Note 22 for additional information on the Mercedes-Benz Group’s pension and post-employment healthcare benefits.

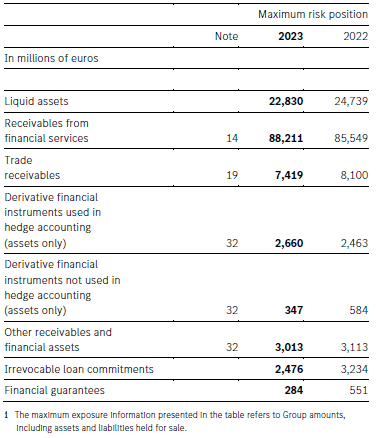

Credit risk

Credit risk describes the risk of financial loss resulting from a counterparty failing to meet its contractual payment obligations. Credit risk encompasses both the direct risk of default and the risk of a deterioration of creditworthiness as well as concentration risks. The maximum risk positions of financial assets which are generally subject to credit risk are equal to their carrying amounts at the balance sheet date (without consideration of collateral, if available). There is also a risk of default from irrevocable loan commitments which had not been utilized as of that date, as well as from financial guarantees. The maximum risk position in these cases is equal to the expected future cash outflows.

The following table shows the maximum risk positions at the balance sheet date.

Maximum risk positions of financial assets, irrevocable loan commitments and financial guarantees1

Liquid assets

Liquid assets consist of cash and cash equivalents and marketable debt securities and similar investments. With the investment of liquid assets, banks and issuers of securities are selected very carefully and diversified in accordance with a limit system. Liquid assets are mainly held at financial institutions within and outside Europe with high creditworthiness, as bonds issued by German federal states and as money market funds. In connection with investment decisions, priority is placed on the borrower’s very high creditworthiness and on balanced risk diversification. The limits and their utilization are reassessed continuously. In this assessment, the Mercedes-Benz Group also considers the credit risk assessment of its counterparties by the capital markets. In line with the Group’s risk policy, most liquid assets are held in investments with an external rating of “A” or better. Liquid assets are thus not subject to a material credit risk and are allocated to stage 1 of the impairment model under IFRS, which is based on expected credit risk.

Receivables from financial services

The Mercedes-Benz Group’s financing and leasing activities are primarily focused on supporting the sales of the Group’s automotive products. As a consequence of these activities, the Group is exposed to credit risk, which is monitored and managed based on defined standards, guidelines and procedures. The Mercedes-Benz Group manages its credit risk irrespective of whether it is related to a financing contract or to an operating lease or a finance lease contract. For this reason, statements concerning the credit risk of Mercedes-Benz Mobility refer to the entire financing and leasing business, unless otherwise specified.

Exposure to credit risk from financing and lease activities is monitored based on the portfolio subject to credit risk. The portfolio subject to credit risk consists of wholesale and retail receivables from financial services and the portion of the operating lease portfolio that is subject to credit risk. Receivables from financial services comprise claims arising from finance lease contracts and repayment claims from financing loans. The operating lease portfolio is reported under equipment on operating leases in the Group’s Consolidated Statement of Financial Position. Lease payments due from operating lease contracts are recognized in receivables from financial services.

The Mercedes-Benz Mobility segment has policies setting the framework for effective risk management at a global as well as a local level. In particular, these policies deal with minimum requirements for all risk-relevant credit processes, the definition of financing products offered, the evaluation of customer quality, requests for collateral and the treatment of unsecured loans and non-performing claims. The limitation of concentration risks is implemented primarily by means of global limits, which refer to customer exposures. To comply with these limits, Mercedes-Benz Mobility applies approval standards and measures to avoid concentration risks. Only one customer was granted a credit line in the form of a large loan. The Mercedes-Benz Mobility portfolio consists of a large number of small and medium-sized enterprises and private customers from more than 30 countries. At 31 December 2023, this segment accounted for 72% of the portfolio.

With respect to its financing and lease activities, the Group holds collateral for customer transactions limiting actual credit risk through its fair value. The value of collateral generally depends on the amount of the financed assets. The financed vehicles usually serve as collateral. Furthermore, Mercedes-Benz Mobility limits credit risk from financing and lease activities, for example through deposits from customers.

For the assessment of the default risk of retail and small business customers, scoring systems are applied to evaluate their creditworthiness. Corporate customers are evaluated using internal rating instruments. Both evaluation processes use external credit bureau data if available. The scoring and rating results as well as the availability of security and other risk mitigation instruments, such as deposits, guarantees and, to a lesser extent, residual debt insurances, are essential elements for credit decisions.

If, in connection with contracts, a worsening of payment behaviour or other causes of a credit risk are recognized, collection procedures are initiated by claims management to obtain the overdue payments of the customer, to take possession of the asset financed or leased or, alternatively, to renegotiate the impaired contract. Internal restructuring policies and practices for loan and leasing contracts are based on the indicators or criteria which, in the judgement of local management, indicate that repayment will probably continue and that the total proceeds expected to be derived from the renegotiated contract exceed the expected proceeds to be derived from immediate repossession and remarketing. In the case of receivables from financial services, significant modifications of financial assets were only made in rare cases and to an insignificant extent.

The allowance ratio decreased compared to the previous year due to the sale of the Russian Mercedes-Benz Mobility companies for which very high provisions were recorded in 2022. The default rate has increased compared to the very low figures in the previous year, mainly due to a challenging lending environment in the United States.

For information on credit risks included in receivables from financial services, see Note 14. Information on the measurement of expected credit losses is provided in Note 1.

Trade receivables

Trade receivables are mostly receivables from worldwide sales of vehicles and spare parts. The credit risk from trade receivables encompasses the default risk of customers, e.g. dealers and general distribution companies, as well as other corporate and private customers. In order to identify credit risks, the Mercedes-Benz Group assesses the creditworthiness of customers. The Mercedes-Benz Group manages its credit risk from trade receivables using appropriate IT applications and databases on the basis of internal policies which have to be followed Group-wide.

A significant proportion of the trade receivables from each country’s domestic business is secured by various country-specific types of collateral. This collateral includes conditional sales, guarantees and sureties, as well as mortgages and deposits from customers.

For trade receivables from the export business, the Mercedes-Benz Group also evaluates its customers’ creditworthiness by means of an internal rating process with consideration of the respective country risk.

In this context, the Annual Financial Statements and other relevant information on the general distribution companies, such as payment history, are used and assessed.

Depending on the creditworthiness of the customers, the Mercedes-Benz Group establishes credit limits and limits credit risks with the following types of collateral:

– credit insurances,

– first-class bank guarantees and

– letters of credit.

These procedures are defined in the export credit guidelines, which have Group-wide validity.

For impairments of trade receivables, the simplified approach is applied, according to which these receivables are allocated to stage 2. Credit losses until maturity for these trade receivables are recognized upon initial recognition.

Further information on trade receivables and the status of loss allowances recognized is provided in Note 19.

Derivative financial instruments

The Group uses derivative financial instruments exclusively for hedging financial risks that arise from its operational business, financing activities or liquidity management. The Mercedes-Benz Group manages its credit risk exposure in connection with derivative financial instruments through a limit system, which is based on the review of each counterparty’s financial strength. This system limits and diversifies the credit risk. As a result, the Mercedes-Benz Group is exposed to credit risk only to a small extent with respect to its derivative financial instruments. In accordance with the Group’s risk policy, most derivatives are contracted with counterparties which have an external rating of “A” or better.

Other receivables and financial assets

The Mercedes-Benz Group is exposed to credit risk only to a small extent with respect to other receivables and financial assets included in other financial assets in 2023 and 2022.

Irrevocable loan commitments

The Mercedes-Benz Mobility segment in particular is exposed to credit risk from irrevocable loan commitments to end customers and retailers. At 31 December 2023, irrevocable loan commitments amounted to €2,476 million (2022: €3,234 million). These loan commitments had a maturity of less than one year and are not subject to a material credit risk based on the current state of knowledge.

Financial guarantees

The maximum potential obligations resulting from financial guarantees amounted to €284 million at 31 December 2023 (2022: €551 million) and included liabilities recognized at 31 December 2023 in the amount of €4 million (2022: €7 million). Financial guarantees represent contractual arrangements. These guarantees generally provide that in the event of default or nonpayment by the primary debtor, the Group will be required to settle such financial obligations generally up to a contractually agreed amount.

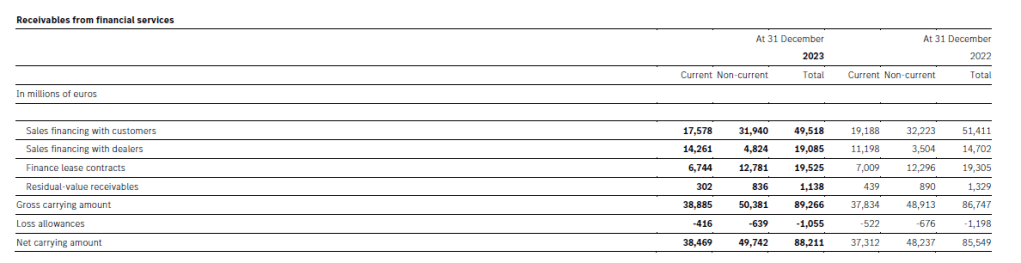

14. Receivables from financial services

Types of receivables

Receivables from sales financing with customers include receivables from credit financing for non-Group third parties who purchased their vehicle either from a dealer or directly from the Mercedes-Benz Group. Receivables from sales financing with dealers represent loans for floor financing programmes for vehicles purchased from the Mercedes-Benz Group. In addition, these receivables also relate to the financing of other assets that the dealers purchased from third parties, in particular used vehicles or property.

Receivables from finance lease contracts consist of receivables from leasing contracts for which all substantial risks and rewards incidental to the leasing objects are transferred to the lessee.

In 2023, the Mercedes-Benz Group recognized a gain of €538 million (2022: €177 million) from the difference between the additions to receivables from finance lease contracts and the carrying amounts of the underlying assets.

At 31 December 2023, receivables from financial services with a carrying amount of €11,139 million (2022: €11,931 million) were pledged mostly as collateral for liabilities from ABS transactions (see also Note 24).

The following table shows the maturities of the future contractual lease payments and the development of lease payments to the carrying amounts of receivables from finance lease contracts.

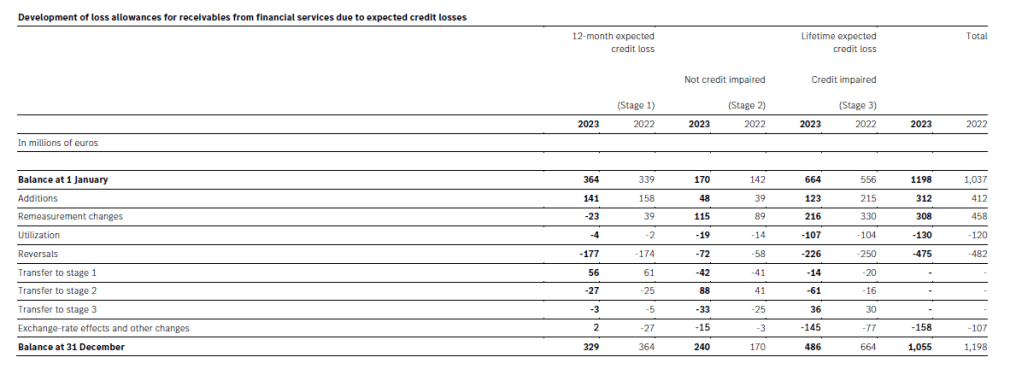

Loss allowances

The loss allowances for receivables from financial services due to expected credit losses are shown in the table Development of loss allowances for receivables from financial services due to expected credit losses. The carrying amounts of receivables from financial services based on modified contracts that are shown in stages 2 and 3, amounted to €463 million at 31 December 2023 (2022: €223 million). In addition, carrying amounts of €86 million in connection with contractual modifications were reclassified at 31 December 2023 from stages 2 and 3 into stage 1 (2022: €135 million).

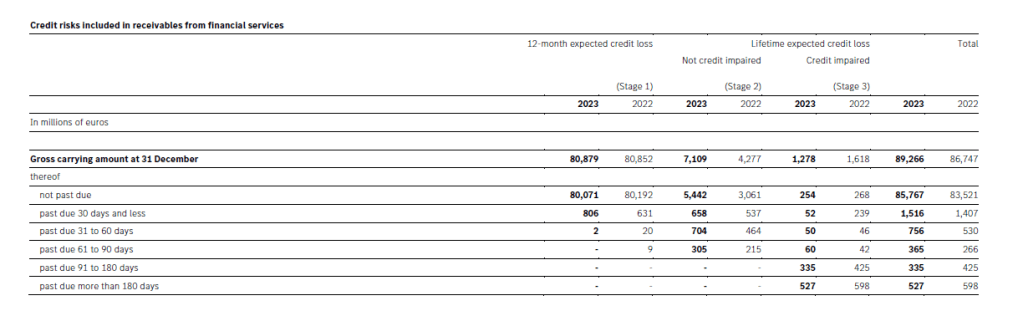

Credit risks

Information on credit risks included in receivables from financial services is shown in the table Credit risks included in receivables from financial services.

Longer overdue periods regularly lead to higher loss allowances.

At the beginning of the contracts, collaterals of usually at least 100% of the carrying amounts were agreed, which are backed by the vehicles based on the underlying contracts. Over the contract terms, the amounts of the collaterals are included in the calculation of the risk provisioning, so the net carrying amounts of the credit-impaired contracts are essentially backed by the underlying vehicles.

Further information on loss allowances, financial risks and types of risks is provided in Note 33.

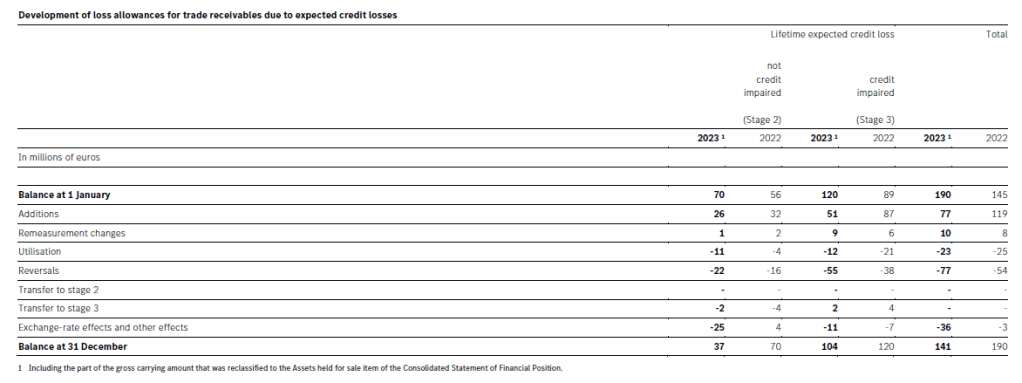

19. Trade receivables

Trade receivables are primarily receivables from contracts with customers within the scope of IFRS 15 and are shown in the following table.

At 31 December 2023, €33 million of the trade receivables mature after more than one year (2022: €48 million).

Loss allowances

The development of loss allowances due to expected credit losses for trade receivables is shown in the following table.

Credit risks

Information on credit risks included in trade receivables is shown in the following table. Further information on financial risk and types of risk is provided in Note 33.