Compass Group PLC – Annual report – 30 September 2025

Industry: support services

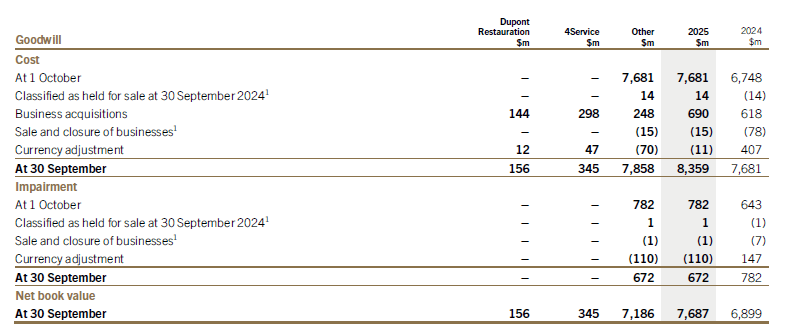

9 Goodwill

Significant accounting policy

Goodwill arising on consolidation represents the excess of the cost of acquisition over the fair value of the Group’s share of the identifiable assets and liabilities of the acquired subsidiary at the date of acquisition. Goodwill is tested annually for impairment and is carried at cost less any accumulated impairment losses.

Goodwill is allocated to the cash-generating units (CGUs) or groups of CGUs that are expected to benefit from the acquisition, which is usually the geographical location of the operations of the Group. Goodwill is subsequently monitored and tested for impairment at the level at which it is allocated. Gains and losses on the disposal of businesses take account of the carrying amount of goodwill relating to the business sold, allocated where necessary on the basis of relative fair value, unless another method is determined to be more appropriate.

The recoverable amount of a CGU is determined based on value-in-use calculations. If the recoverable amount of a CGU is less than its carrying amount, an impairment loss is recognised in the consolidated income statement which is allocated first to reduce the carrying amount of any goodwill allocated to the CGU and then to the other assets of the CGU pro rata on the basis of the carrying amount of each asset in the CGU. An impairment loss recognised in respect of goodwill is not subsequently reversed.

Major source of estimation uncertainty

The value in use of the UK CGU is estimated for the purposes of impairment testing based on assumptions, including the most recent three-year strategic plan approved by management, long-term growth rates and discount rates. A reasonably possible change in the assumptions used to derive this estimate could have a material effect on the carrying amount of goodwill in the UK CGU in the next 12 months. The key assumptions used in the value-in-use calculations, together with sensitivity analysis, are set out below.

Climate change

The potential impact of climate change and the Group’s net zero commitments on forecast cash flows beyond the Group’s three-year planning period has been considered during impairment testing by including in the sensitivity analysis assumptions consistent with the quantitative scenario analysis performed for the Task Force on Climate-related Financial Disclosures (see pages 30 and 31).

1. The assets and liabilities of the businesses classified as held for sale at 30 September 2024 were sold during 2025 and are included in sale and closure of businesses (see note 27).

1. Includes $1.8bn (2024: $1.7bn) which arose in 2000 on the Granada transaction.

2. 2024 includes $352m of goodwill recognised on the acquisition of CH&CO which has been allocated to the UK CGU on completion of the integration of the business in 2025.

3. Our former Rest of World region now accounts for c.5% of the Group’s revenue on a pro forma basis. With effect from 1 October 2024, the Group’s internal management reporting structure changed to combine Rest of World with Europe to form a new International region. Comparative segmental financial information for 2024 has been re-presented.

Impairment testing

The key assumptions used in the value-in-use calculations are: operating cash flow forecasts from the most recent three-year strategic plan approved by management, adjusted to remove the expected benefits of future restructuring activities and improvements to assets; externally-derived long-term growth rates; and pre-tax discount rates.

The strategic plan is based on expectations of future outcomes taking into account past experience, adjusted for anticipated revenue growth from both new business and like-for-like growth, and taking into consideration macroeconomic and geopolitical factors, including the impact of inflation.

Cash flows beyond the three-year period covered by the plan are extrapolated using estimated growth rates based on expected local economic conditions and do not exceed the long-term average growth rate for the country. Cash flow forecasts for a period of up to five years are used by exception to reflect the medium-term prospects of the business if the initial level of headroom in the impairment test for a country is low, with cash flows beyond five years extrapolated using estimated growth rates that do not exceed the long-term average growth rate for that country.

The pre-tax discount rates are based on the Group’s Weighted Average Cost of Capital (WACC) adjusted for specific risks relating to the country in which the CGU operates. The beta and gearing ratio assumptions used in the calculation of the discount rates represent market participant measures based on the averages of a number of companies with similar assets.

1. Other excludes Türkiye which has residual growth rate and pre-tax discount rate assumptions of 15.1% (2024: 15.5%) and 26.5% (2024: 27.1%), respectively.

Consistent with prior years, the goodwill impairment testing was performed as at 31 July. Subsequent to 31 July, management has considered whether there have been any indicators that the goodwill may be impaired. There was no impact on the reported amounts of goodwill as a result of this review.

Sensitivity analysis

The Group has performed a sensitivity analysis based on changes in key assumptions considered to be reasonably possible by management. The sensitivity analysis is prepared on the basis that a change in the assumptions would not have a consequential impact on other assumptions used in the impairment testing. There was no impact on the reported amounts of goodwill as a result of this review.

The recoverable amount of the Group’s operations in the UK, which is estimated to exceed its carrying value by $572m (2024: $512m), is sensitive to a reasonably possible change in the pre-tax discount rate. In the event that the pre-tax discount increased by 1%, the estimated recoverable amount would decrease by $411m (2024: $309m). In order for the estimated recoverable amount to be equal to the carrying value, the pre-tax discount rate would have to increase by 1.5% (2024: 1.8%), projected operating profit decrease by 13% (2024: 16%) or the long-term growth rate decrease to a decline of 0.1% (2024: 0.6%).

No other reasonably possible changes in key assumptions would cause the estimated recoverable amounts of the individually significant CGUs disclosed above to fall below their carrying values.