Land Securities Group PLC – Annual report – 31 March 2026

Industry: real estate

SECTION 3 – PROPERTIES

This section focuses on the property assets which form the core of the Group’s business. It includes details of investment properties, investments in joint ventures and trading properties.

Our property portfolio is a combination of properties that are wholly owned by the Group, part owned through joint arrangements and properties owned by the Group but where a third party holds a non-controlling interest. In the Group’s IFRS balance sheet, wholly owned properties and properties owed by the Group but where a third party holds a non-controlling interest are presented as either ‘Investment properties’ or ‘Trading properties’. The Group applies equity accounting to its investments in joint ventures, which requires the Group’s share of properties held by joint ventures to be presented within ‘Investments in joint ventures’.

Internally, management review the results of the Group on a basis that adjusts for these forms of ownership to present a proportionate share. The Combined Portfolio, with assets totalling £10.8bn, is an example of this proportionate share, reflecting the economic interest we have in our properties regardless of our ownership structure. We consider this presentation provides further insight to stakeholders about the activities and performance of the Group, as it aggregates the results of all of the Group’s property interests which under IFRS are required to be presented across a number of line items in the statutory financial statements.

The Group’s investment properties are carried at fair value and trading properties are carried at the lower of cost and net realisable value. Both of these values are determined by the Group’s external valuers. The combined value of the Group’s total investment property portfolio (including the Group’s share of investment properties held through joint ventures) is shown as a reconciliation in note 13.

A ACCOUNTING POLICY

INVESTMENT PROPERTIES

Investment properties are properties, either owned or leased by the Group, that are held either to earn rental income or for capital appreciation, or both. Investment properties are measured initially at cost including related transaction costs, and subsequently at fair value. Fair value is based on market value, as determined by a professional external valuer at each reporting date. The difference between the fair value of an investment property at the reporting date and its carrying amount prior to remeasurement is included in the income statement as a valuation surplus or deficit. Investment properties are presented on the balance sheet within non-current assets.

Some of the Group’s investment properties are owned through long-leasehold arrangements, as opposed to the Group owning the freehold. Where the Group is a lessee, a right-of-use asset is recognised at the commencement date of the lease and accounted for as investment property. Initially, the cost of investment properties held under leases includes the amount of lease liabilities recognised, initial direct costs incurred, and lease payments made at or before the commencement date less any lease incentives received. The investment properties held under leases are subsequently carried at their fair value. A corresponding liability is recorded within borrowings. Each lease payment is allocated between repayment of the liability and a finance charge to achieve a constant interest rate on the outstanding liability.

TRADING PROPERTIES

Trading properties are those properties held for sale, or those being developed with a view to sell. Trading properties are recorded at the lower of cost and net realisable value. The net realisable value of a trading property is determined by a professional external valuer at each reporting date. If the net realisable value of a trading property is lower than its carrying value, an impairment loss is recorded in the income statement. If, in subsequent periods, the net realisable value of a trading property that was previously impaired increases above its carrying value, the impairment is reversed to align the carrying value of the property with the net realisable value. Trading properties are presented on the balance sheet within current assets.

ACQUISITION OF PROPERTIES

Properties are treated as acquired when the Group assumes control of the property.

CAPITAL EXPENDITURE AND CAPITALISATION OF BORROWING COSTS

Capital expenditure on properties consists of costs of a capital nature, including costs associated with developments and refurbishments. Where a property is being developed or undergoing major refurbishment, interest costs associated with direct expenditure on the property are capitalised. Where borrowings are specifically used to finance any capital expenditure on the properties, the actual borrowing costs incurred are capitalised. However, where borrowings are used generally to finance the operations of the Group, the interest capitalised is calculated using the Group’s weighted average cost of borrowings. Interest is capitalised from the commencement of the development work until the date of practical completion. Certain internal staff and associated costs directly attributable to the management of major schemes are also capitalised. The total staff and associated costs are capitalised based on the proportion of time spent on the relevant scheme. Internal staff costs are capitalised from the date the Group determines it is probable that the development will progress until the date of practical completion.

TRANSFERS BETWEEN INVESTMENT PROPERTIES AND TRADING PROPERTIES

When the Group begins to redevelop an existing investment property for continued future use as an investment property, the property continues to be held as an investment property. When the Group begins to redevelop an existing investment property with a view to sell, the property is transferred to trading properties and held as a current asset. The property is remeasured to fair value as at the date of the transfer with any gain or loss being taken to the income statement. The remeasured amount becomes the deemed cost at which the property is then carried in trading properties.

DISPOSAL OF PROPERTIES

Properties are treated as disposed when control of the property is transferred to the buyer. Typically, this will either occur on unconditional exchange or on completion. Where completion is expected to occur significantly after exchange, or where the Group continues to have significant outstanding obligations after exchange, the control will not usually transfer to the buyer until completion.

The profit on disposal is determined as the difference between the sales proceeds and the carrying amount of the asset at the beginning of the accounting period plus capital expenditure to the date of disposal. The profit on disposal of investment properties is presented separately on the face of the income statement. Proceeds received on the sale of trading properties are recognised within Revenue, and the carrying value at the date of disposal is recognised within Costs.

S SIGNIFICANT ACCOUNTING JUDGEMENT

ACQUISITION AND DISPOSAL OF PROPERTIES

Property transactions can be complex in nature and material to the financial statements. To determine when an acquisition or disposal should be recognised, management consider whether the Group assumes or relinquishes control of the property, and the point at which this is obtained or relinquished. Consideration is given to the terms of the acquisition or disposal contracts and any conditions that must be satisfied before the contract is fulfilled. In the case of an acquisition, management must also consider whether the transaction represents an asset acquisition or business combination.

KEY ACCOUNTING ESTIMATES AND OTHER SOURCES OF ESTIMATION UNCERTAINTY

VALUATION OF THE GROUP’S PROPERTIES

The valuation of the Group’s property portfolio has been undertaken by independent valuers in accordance with the Royal Institution of Chartered Surveyors (RICS) Valuation – Global Standards and UK Supplement (together the “Red Book”). Real estate by its nature is a complex asset class with value determined by a range of factors overlaid by interpretation and judgemental assessment of market data; as such it is classified as ‘Level 3 asset’ within IFRS. Factors affecting valuation are on an individual property level and include the property type, location, tenure and tenancy characteristics, quality of the asset and prospects for future rental revenue.

The Group’s investment property valuation has been undertaken by valuers interpreting market evidence as available in reaching their conclusions on Fair Value, reflecting asset specific data provided by Management, making assumptions that tenure, tenancies, town planning and condition of buildings are as provided. As a result, the valuations the Group places on its property portfolio are subject to a degree of uncertainty and are made on the basis of assumptions which may not prove to be accurate, particularly in periods of volatility or low transaction volume in the property market.

The estimation of the net realisable value of the Group’s trading properties, in particular the development land and infrastructure programmes, is inherently subjective due to a number of factors, including their complexity, unusually large size, the substantial expenditure required and long timescales to completion. In addition, as a result of these timescales to completion, the plans associated with these programmes could be subject to significant market variation over the course of development. As a result, and similar to the valuation of investment properties, the net realisable values of the Group’s trading properties are subject to a degree of uncertainty and are determined on the basis of assumptions which may not prove to be accurate.

If the assumptions upon which the external valuer has based its valuations prove to be inaccurate, this may have an impact on the value of the Group’s investment and trading properties, which could in turn have an effect on the Group’s financial position and results. Whilst the valuations were appropriate as at 31 March 2026, changes to macroeconomic conditions could affect future valuations.

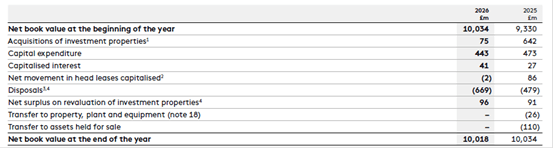

13 INVESTMENT PROPERTIES

1. Adjusted downward by £17m of transaction and contract related provisions utilised in the year (see note 33).

2. See note 21 for details of the amounts payable under head leases and note 4 for details of the rents payable in the income statement.

3. Includes impact of disposals of finance leases.

4. Whilst the Group’s accounting policy is to recognise the profit/(loss) on disposal of investment properties with reference to the asset’s carrying amount at the beginning of the accounting period, £22m of the balance pertains to revaluation movements arising from rental income received from 1 April 2025 to the date of disposal on the Queen Anne’s Mansions office block.

The market value of the Group’s investment properties, as determined by the Group’s external valuers, differs from the net book value presented in the balance sheet due to the Group presenting tenant finance leases, head leases and lease incentives separately. The following table reconciles the net book value of the investment properties to the market value.

1. Refer to note 15 for a breakdown of this amount by our principal joint arrangements.

The net book value of leasehold properties where head leases have been capitalised is £1,438m (2025: £1,761m).

Investment properties include capitalised interest of £358m (2025: £317m). The average rate of interest capitalisation for the year is 4.7% (2025: 4.8%). The gross historical cost of investment properties is £8,941m (2025: £9,136m).

VALUATION PROCESS

The fair value of investment properties at 31 March 2026 was determined by the Group’s external valuers, CBRE and JLL. The valuations are in accordance with RICS standards and were arrived at by reference to market evidence of transactions for similar properties. The valuations performed by the valuers are reviewed internally by Senior Management and other relevant people within the business. This process includes discussions of the assumptions used by the valuers, as well as a review of the resulting valuations. Discussions of the valuation process and results are held between Senior Management, the Audit Committee and the valuers on a half-yearly basis.

The valuers’ opinion of fair value was primarily derived using comparable recent market transactions on arm’s length terms and using appropriate valuation techniques. The fair value of investment properties is determined using the income capitalisation approach. Under this approach, forecast net cash flows, based upon existing leases and current market derived estimated rental values (market rents) together with estimated costs, are discounted at market derived capitalisation rates to produce the valuers’ opinion of fair value. The average discount rate, which, if applied to all cash flows would produce the fair value, is described as the equivalent yield.

Properties in the development programme are typically valued using a residual valuation method. Under this methodology, the valuer assesses the completed development value using income and yield assumptions. Deductions are then made for estimated costs to complete, including finance and developer’s profit, to arrive at the valuation. Costs include future estimated costs associated with refurbishment or development (excluding finance costs), together with an estimate of cash incentives to be paid to tenants. As the development approaches completion, the valuer may consider the income capitalisation approach to be more appropriate.

The Group considers all of its investment properties to fall within ‘Level 3’, as defined by IFRS 13 and as explained in note 25(iii). Accordingly, there have been no transfers of properties within the fair value hierarchy in the financial year.

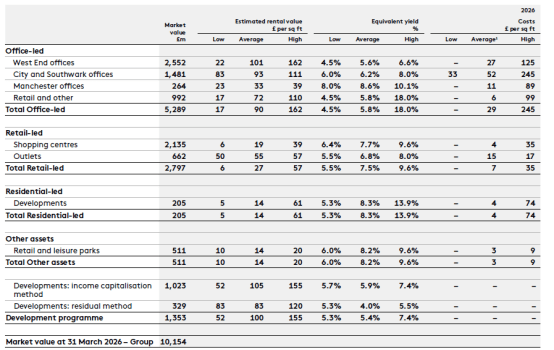

The table below summarises the key unobservable inputs used in the valuation of the Group’s wholly owned investment properties, and properties owned by the Group but where a third party holds a non-controlling interest, at 31 March 2026:

1. The calculation for average costs excludes those properties which are assumed by the Group’s external valuer to be substantially refurbished or redeveloped, but which do not yet form part of the development programme.

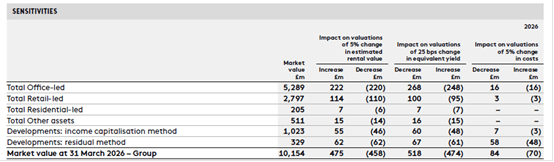

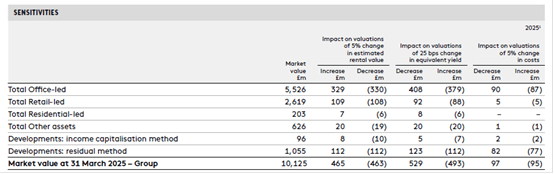

The sensitivities below illustrate the impact of changes in key unobservable inputs (in isolation) on the fair value of the Group’s properties:

The table below summarises the key unobservable inputs used in the valuation of the Group’s wholly owned investment properties, and properties owned by the Group but where a third party holds a non-controlling interest, at 31 March 2025:

1. Restated for changes in the Group’s operating segments as outlined in note 4.

2. The calculation for average costs excludes those properties which are assumed by the Group’s external valuer to be substantially refurbished or redeveloped, but which do not yet form part of the development programme.

The sensitivities illustrate the impact of changes in key unobservable inputs (in isolation) on the fair value of the Group’s properties:

1. Restated for changes in the Group’s operating segments as outlined in note 4.

40 OPERATING LEASE ARRANGEMENTS

A ACCOUNTING POLICY

The Group earns rental income by leasing its properties to tenants under non-cancellable operating leases. Leases in which substantially all risks and rewards incidental to ownership of investment properties are retained by the Group as the lessor are classified as operating leases. Payments, including prepayments, received under operating leases (net of any incentives paid) are charged to the income statement on a straight-line basis over the period of the lease.

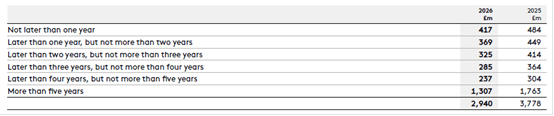

At the balance sheet date, the Group had contracted with tenants to receive the following undiscounted future minimum lease payments:

The total of contingent rents, primarily turnover based rents, recognised as income during the year was £43m (2025: £25m).

16 CAPITAL COMMITMENTS

Capital commitments include contractually committed obligations to purchase goods or services used in the construction, development, repair, maintenance or other enhancement of the Group’s properties.

6 REVENUE (extract)

All revenue is classified within the ‘EPRA earnings’ column of the income statement, with the exception of proceeds from the sale of trading properties, income from development contracts or transactions and the non-owned element of the Group’s subsidiaries which are presented in the ‘Capital and other items’ column.

1. Current year balances reflect a reclassification of service charge management fees from service charge expense to service charge income of £11m. While the comparatives have not been restated, the equivalent reclassification would have been £8m.