NEXT plc – Annual report – 31 January 2026

Industry: retail

CORPORATE RESPONSIBILITY (extract)

ENVIRONMENT

Our commitment

We are committed to minimising our environmental impact by reducing the carbon intensity of our activities and the natural resources we use.

Rankings

Our efforts around ESG are reflected in the following external benchmarks:

- Constituent of the FTSE4Good Index.

- MSCI: ESG rating AA (Leader).

- CDP: Climate change: B, Forests: C, Water security: B-.

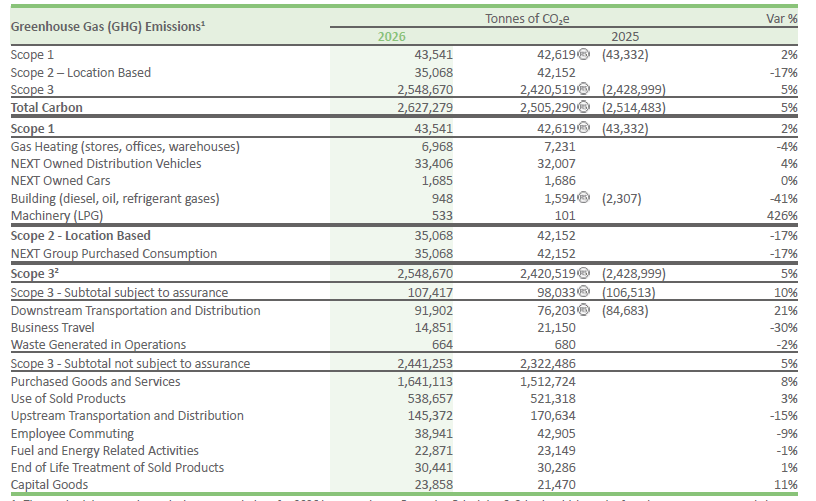

Greenhouse gas emissions – Streamlined Energy and Carbon Reporting (SECR)

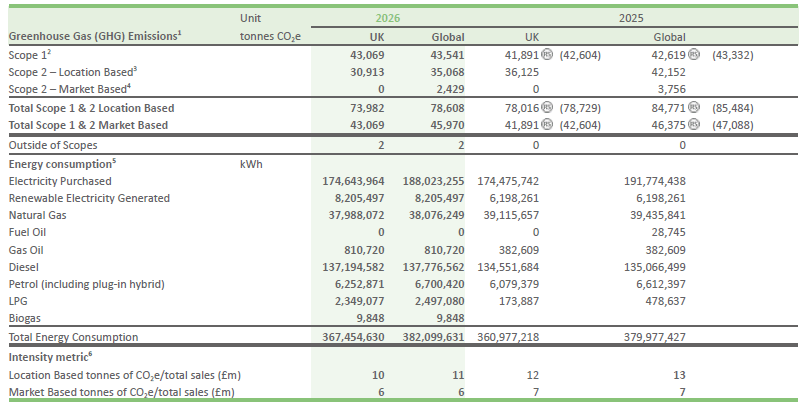

In accordance with the disclosure requirements for listed companies under the Companies Act 2006, the table below shows the Group’s SECR disclosure across Scope 1 and 2 together with an appropriate intensity metric and our total energy use of gas, electricity and other fuels during the financial year. The reported emissions data for 2026 includes NEXT plc and those of its subsidiaries in which it has a controlling interest. Emissions from Reiss, FatFace and Joules are consolidated in our reporting and appear in the figures for 2025 and 2026 in the table below. Please see our Group Corporate Responsibility Report at nextplc.co.uk for details of assurance on this data.

1. The methodology used to calculate our emissions aligns with our global direct carbon footprint and is measured in alignment with the GHG Protocol Corporate Accounting and Reporting Standard and RE100 reporting parameters. We adopt the conventional approach in calculating our carbon emissions through the collection of primary, secondary, or tertiary data in their source units (e.g. kilowatt-hours (kWh), litres (L), kilograms (kg), kilometres (km) etc.). The consumption figures relating to each energy source are converted into carbon emissions by applying the relevant carbon conversion factor. Factors are updated annually using the most recent factors published by the UK Department for Energy Security and Net Zero and the UK Department for Environment, Food and Rural Affairs (Defra); 2025 is the most recent accessible update.

2. Scope 1 being emissions from combustion of fuel and refrigerant gas losses.

3. Scope 2 being electricity (from location based calculations), heat, steam and cooling purchased for the Group’s own use.

4. The calculation of market based emissions is based on our energy suppliers fulfilling their contractual obligations under the terms of renewable tariffs to back all energy supplied to all of their customers on such tariffs. As members of RE100, our approach is informed by the RE100 quality criteria and GHG protocol guidance. RE100 requires claims to use of renewable electricity to be based on generation occurring in the same market for renewable electricity that use is claimed in, this includes the single market in Europe. The revised RE100 guidance published in December 2022 provided an updated list of countries that make up the single market. Although the UK has been excluded from the list, the RE100 guidance provided grandfathering provisions for contracts with operational commencement dates before 1 January 2024, allowing for the UK to continue to be recognised within the single market in Europe. The operational commencement dates of our contracts occurred prior to 1 January 2024, therefore we have applied the grandfathering provisions when calculating our market based emissions.

5. Energy from electricity, natural gas, gas oil, transport fuel and LPG have been included. We have used the 2025 Defra GHG conversion factors for company reporting to convert from passenger miles in company-owned vehicles to kWh.

6. We use tonnes of CO2e/Total Sales (£m) as our intensity metric. Sales used in the calculation of our intensity metric are based on the Total NEXT Trading sales and the gross transaction value of sales from our Total Platform, Franchise, Sourcing and other divisions. Total NEXT Trading sales is defined in the Glossary on page 260.

RS Restated from prior year. During the year an issue with Reiss’ third-party air conditioning contractor was identified whereby incorrect data had been submitted. This error accounted for 714 tCO2e, a -2% variance of total Group Scope 1 which is below our materiality threshold for materiality, but included here for casting. We have since worked with our third-party contractors to ensure this issue does not reoccur.

Changes in our SECR

This year, there has been a 2% increase in our Scope 1 emissions on the prior year. This has been driven largely through increases in fuel consumption by our retail distribution fleet and our new LPG fuelled steam tunnel in our rework operation at E3. The distribution increases have been driven by a higher number of sites being covered as a consequence of adding FatFace retail distribution to the Group’s fleet operations. This year has seen reduced natural gas consumption, following the closure of the Toftshaw site last year and a significant reduction in our refrigerant gas loss, largely driven by the closure of a site in Sri Lanka, which have lessened the impact of the increased fuel consumption. Our Scope 2 emissions have benefited significantly from a 14% decrease in the carbon intensity of the UK grid, alongside the closure of some sites which has offset the small increase in our electricity consumption.

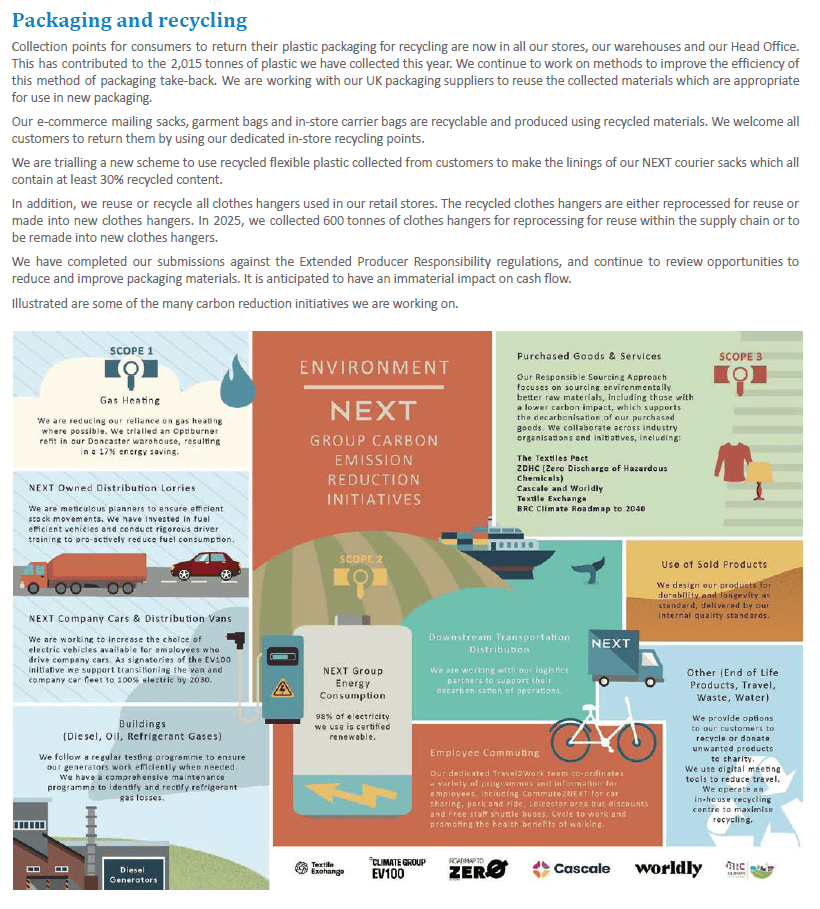

Energy consumption data is captured through monthly bills showing actual or estimated consumption. We continue to look for ways to improve energy efficiency as this reduces both carbon emissions and costs for our business, whilst noting that Scope 1 and 2 emissions only equate to 3% of our total carbon emissions. We actively track and review energy performance via a central data collection facility to ensure our properties are operating efficiently. The following initiatives were undertaken during the year:

- Trialled an optiburner retrofit in our Doncaster warehouse to drive efficiencies in gas heating, resulting in a 17% energy saving.

- Expanded our successful energy optimisation programme, achieving an average 6% energy saving. We continue to install high efficiency LED lighting and replace Generation I LEDs at end of life across our retail store estate including NEXT and Victoria’s Secret UK stores.

- Rolled out our Active Energy Management programme across all of NEXT stores with Building Management Systems (BMS) to ensure that heating, ventilation and cooling equipment is working correctly, such as switching on during trading hours and off during non-trading hours. We also upgraded our BMS controllers at NEXT Head Office.

Renewable energy

NEXT is a signatory to the RE100 initiative and has committed to using 100% renewable energy by 2030. Our UK and Ireland operations have been using 100% renewable energy since April 2017 and we continue to work towards achieving this target in our direct operations overseas.

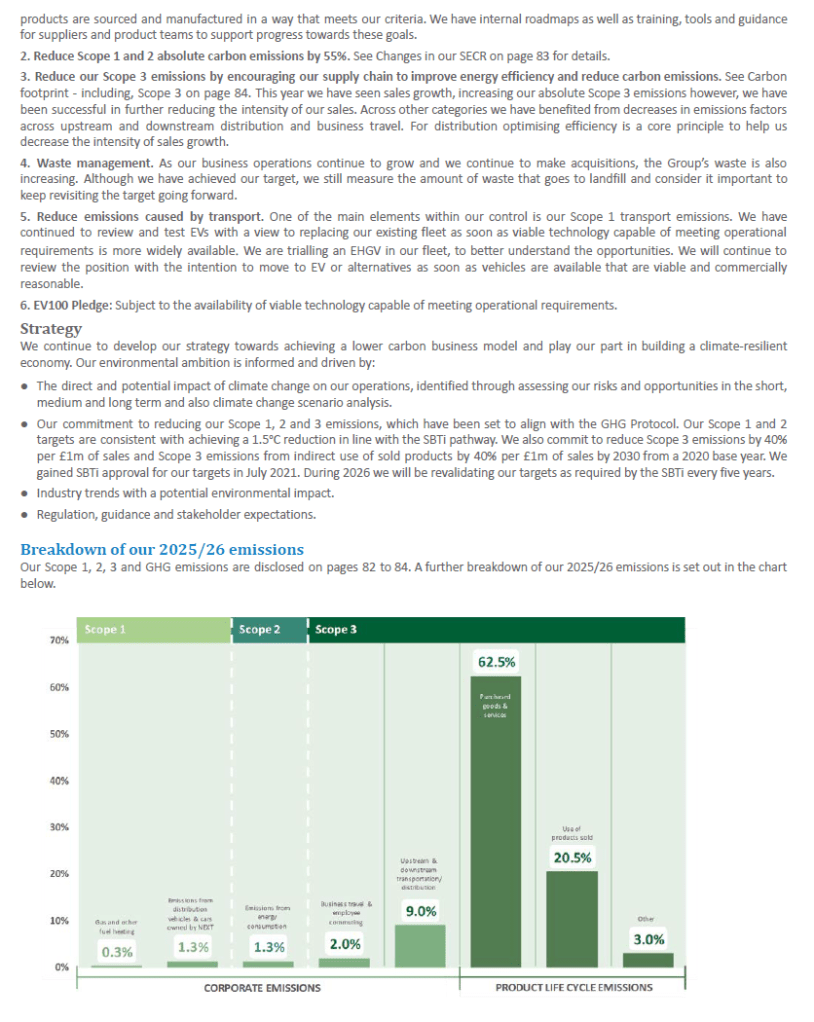

Carbon footprint – including Scope 3

Due to the nature of our business, most of our carbon footprint falls outside of our direct control and is reported under our Scope 3 emissions. Our Scope 3 total emissions disclosure (CO2e) covers the complete lifecycle of all the products we sell, including branded items sold through LABEL and Total Platform1.

Our Scope 3 disclosure extends from the production of raw materials through to the manufacture, transport, how our customers use and care for them and the eventual end of life treatment of the products we sell. The emissions have been estimated in line with the GHG Protocol Corporate Accounting and Reporting Standard and are based on a combination of internal data coupled with the best available public sources on CO2e emissions factors using conservative assumptions. Our total Scope 3 emissions are reported in the table below, together with our Scope 1 and 2 (location based) emissions. Our carbon reduction targets are set out on page 89.

1. The methodology used to calculate our emissions for 2026 is set out in our Reporting Principles & Criteria which can be found on our corporate website at nextplc.co.uk. Reiss, Joules and FatFace are included in the Scope 1, Scope 2 and Scope 3 data.

2. We have excluded franchises from our reporting at present due to challenges in obtaining accurate and reliable data.

3. PricewaterhouseCoopers LLP (PwC) carried out a limited assurance engagement on selected GHG emissions metrics for the 53 weeks ending 31 January 2026. The results of that assurance and a copy of PwC’s report are within our Group Corporate Responsibility Report which is published on our corporate website at nextplc.co.uk.

RS Restated from prior year.

Restatements

Scope 1: During the year an issue with Reiss’ third-party air conditioning contractor was identified whereby incorrect data had been submitted. This error accounted for 714 tCO2e, a -2% variance of total Group Scope 1 which is below our materiality threshold for materiality, but included here for casting. This accounts for -31% of the Group’s buildings emissions category.

Scope 3: An error in data received from our third-party haulier last year caused the weight of products being sent to our Middle Eastern hub to be overstated. This error has been corrected resulting in a restatement of -10% of Downstream Transportation and Distribution, -8% of the assured Scope 3 subtotal. It is not material to our total Scope 3 (-0.35%) but this has been restated for consistency.

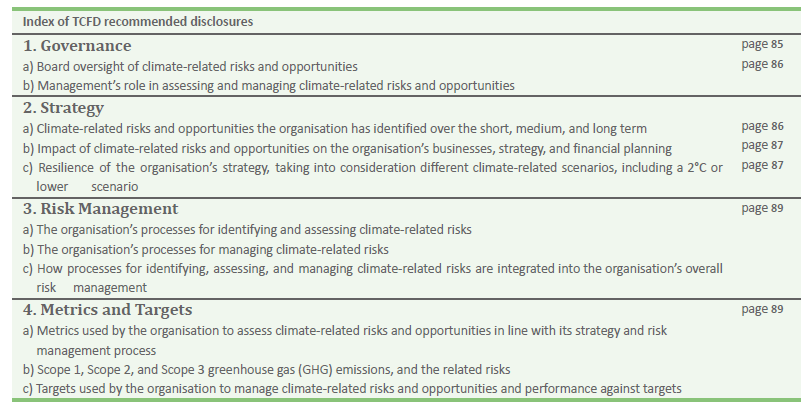

Task Force on Climate-related Financial Disclosures (TCFD)

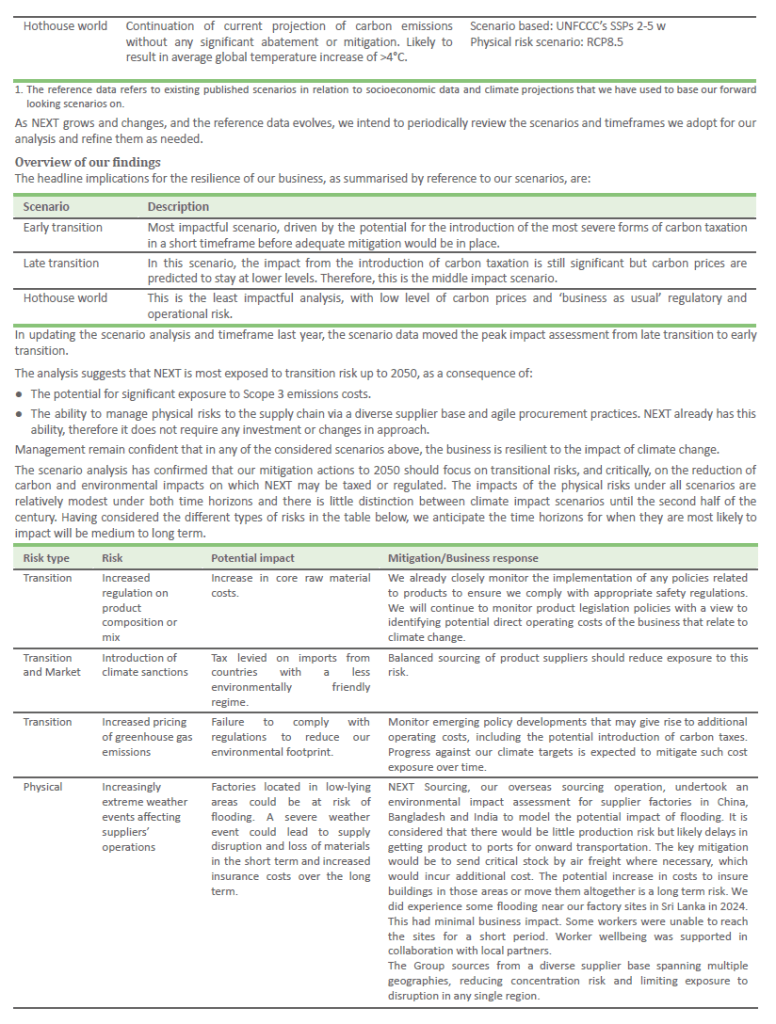

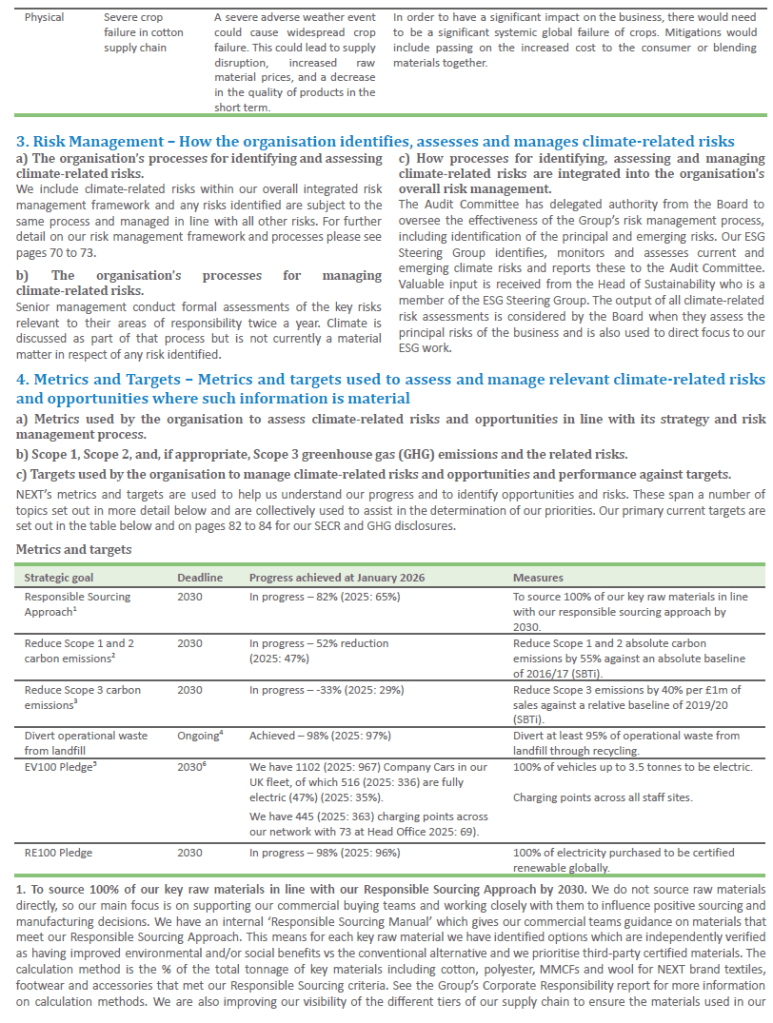

Climate change poses challenges for our business and supply chain. We look to support the Paris Agreement on climate to limit the rise in global temperatures to well below 2⁰C. Accurate and relevant disclosures are essential to demonstrate progress and ensure stakeholder accountability and this reporting helps us set a baseline from which appropriate and meaningful actions can be measured.

Statement of consistency

NEXT’s climate-related disclosures are consistent with the ‘Section C – All Sector Guidance’ within the Supplementary Guidance Report ‘Implementing the Recommendations of the TCFD’, and in compliance with the requirements of UK Listing Rule 6.6.6(8)(a).

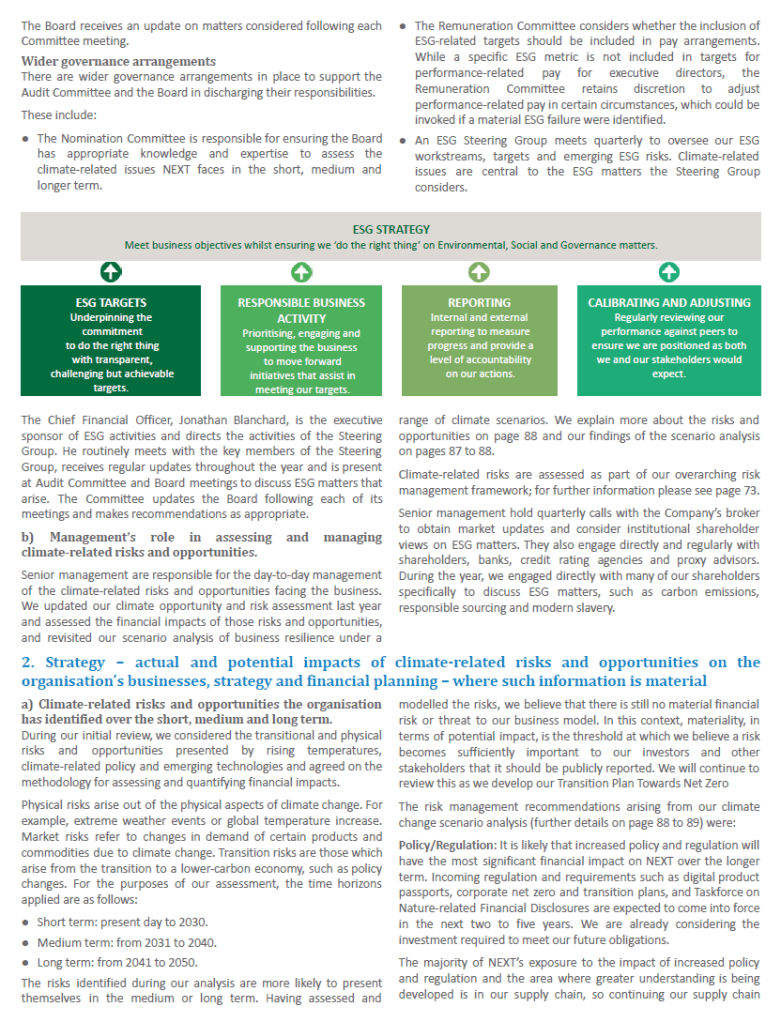

1. Governance– The organisation’s governance around climate-related risks and opportunities

Our simple governance structure around ESG-allows emerging issues and matters for decisions to be escalated quickly.