Redcentric plc – Annual report – 31 March 2017

Industry: manufacturing

FINANCIAL REVIEW (extract)

Accounting misstatements

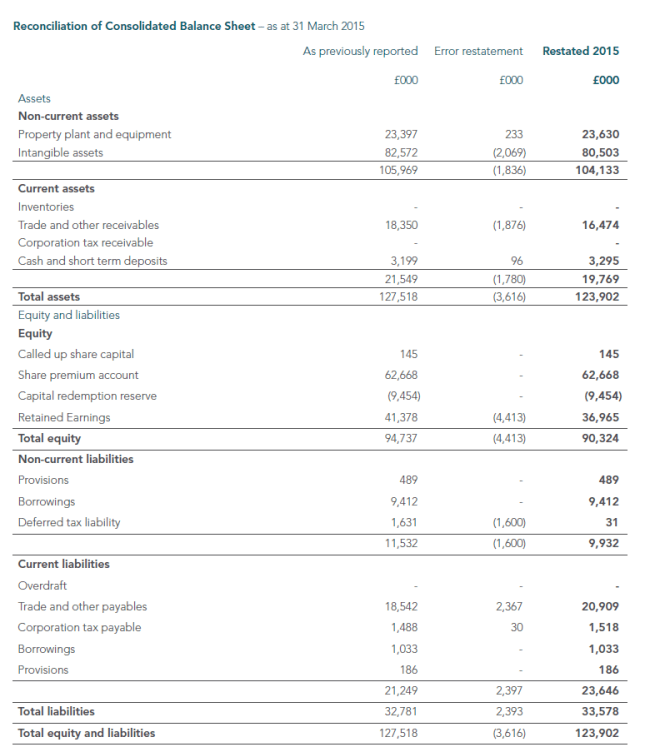

Net assets and net debt

Following an internal review by the Company’s Audit Committee in relation to the interim results for the six months ended 30 September 2016, materially misstated accounting balances in the Group’s balance sheet were discovered.

The Board acted promptly and appointed Deloitte and CMS Cameron McKenna Nabarro Olswang LLP to carry out an independent forensic review. The majority of misstatements arose in the group’s main subsidiary, Redcentric Solutions Limited. The forensic review found that both net assets and net debt as at 31 March 2016 had been materially misstated. The misstatements arose due a combination of wilful misstatement and poor application of basic accounting controls and processes. The investigation did not find any evidence of theft.

The review found that net assets as at 31 March 2016 had been overstated by £14.9m (subsequently revised to £15.8m as per note 28). A number of accounting policies and practices, specifically those in respect of cost accrual, cost deferment and revenue recognition had been incorrectly applied.

Net debt at 31 March 2016 had been understated by £12.5m. The forensic review uncovered misstatements regarding the timing of cash receipts and cash payments. Cash receipts from customers received post year end had been incorrectly recorded as having been received pre year end and cash payments to suppliers pre year end had been incorrectly recorded as being made post year end.

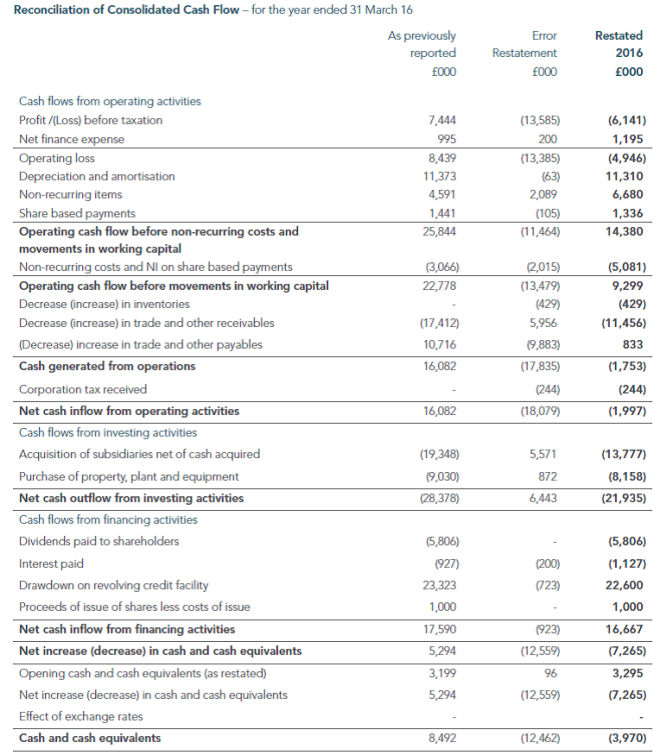

In addition to the accounting errors and misstatements, supplier payments had been very significantly delayed in order to present a better net debt position (cash flows and net debt below).

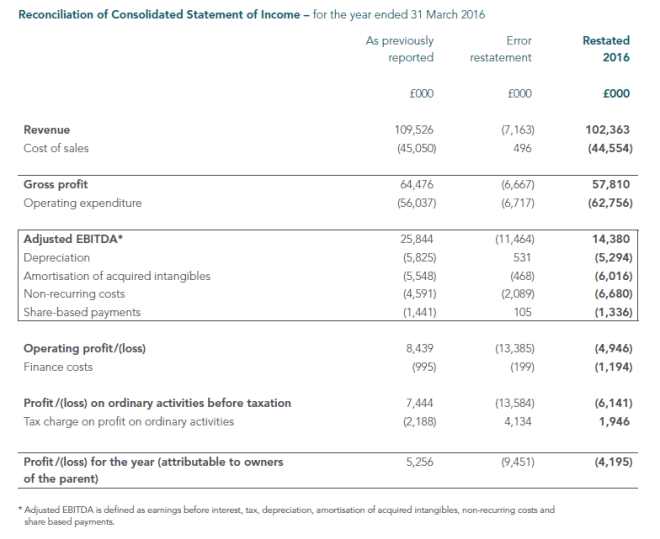

Income statement prior year comparative figures

The scale and complexity of the misstatements, along with the length of time over which the misstatement occurred, meant that the forensic review took a significant time to complete and a level of judgement was applied to the allocation of profit reduction over a number of accounting periods. The forensic review focused on the 30 September 2016 and 31 March 2016 balance sheets and additional work was undertaken by the Company to analyse and attribute the accounting misstatements back to 31 March 2015.

Whilst the audits of the subsidiary companies had been completed, the statutory accounts for the year ended 31 March 2016 were not filed at the same time as the Redcentric plc group accounts. Given the material misstatements discovered, the Group’s subsidiary accounts had to be re-audited by the predecessor auditor, PwC. This was a very time consuming exercise and was completed when the subsidiary accounts were drawn up again and filed with Companies House on 28 April 2017. Whilst all of the Group’s subsidiaries received unqualified audit reports on the Statements of Financial position, the Statement of Comprehensive income of Redcentric Solutions Limited received a qualified opinion as the company’s former auditors, PwC, were unable to form an opinion within reasonable timescales. The directors took the view that the time and cost of the further investigations necessary to provide sufficient audit evidence would be disproportionate, and this conclusion also applies to the comparative consolidated Statement of Comprehensive Income within these financial statements, leading to a qualified opinion being issued by KPMG.

As a result of the scale of the restatements to the comparative numbers and the qualification of the audit report on the 2016 income statement, we have not sought to comment on comparative trading figures.

Remedial plan

The forensic review identified a number of process and control failings which required prompt rectification action. Significant progress has been made in improving the financial control environment post the forensic review:

- The finance team has been significantly strengthened in terms of numbers, experience and capability.

- Significantly enhanced financial controls have been applied across the business.

- Clear cash cut off policies are rigorously applied.

- The replacement of the multiple legacy back office systems is underway and a fully integrated Microsoft platform will be implemented by the start of the next financial year.

Bank refinancing

As a result of the accounting misstatements, the Group’s historical financial results had to be restated and this meant that previously reported banking covenant ratios had been breached.

The Group received covenant waivers for the historical breaches from its Banking Syndicate (Barclays, NatWest and Lombard) and a revised facilities agreement was signed on 27 April 2017.

The revised facilities agreement was broadly in line with the original agreement save with an increased margin.

Financial Conduct Authority investigation

On 17 March 2017, the Financial Conduct Authority (“FCA”) notified Redcentric that it had commenced an investigation in connection with the Company’s publication of accounting information and other announcements concerning its financial position. This followed the completion of an independent forensic review commissioned by the Board of Redcentric.

Redcentric is co-operating fully with the FCA and other relevant authorities concerning this matter.

INDEPENDENT AUDITOR’S REPORT TO THE MEMBERS OF REDCENTRIC PLC (extract)

Basis for qualified opinion on financial statements

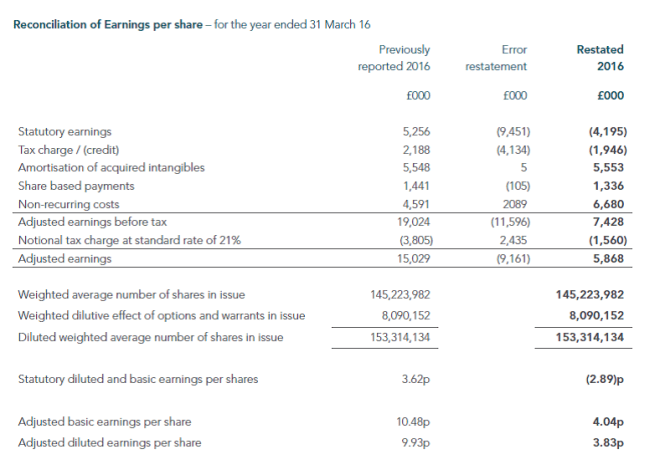

During the year ended 31 March 2017 the Audit Committee discovered a number of materially misstated balances in the Group’s accounting records. The Directors commissioned an independent forensic review, which identified a significant reduction in the previously reported net assets as at 31 March 2016 and 31 March 2015. During the preparation of the 31 March 2017 financial statements, the Directors identified additional misstatements in the previously reported Group financial statements. Consequently the Group has recognised multiple prior year adjustments, as further explained in note 28 to the financial statements, thus reducing net assets as at 31 March 2016 and 31 March 2015 by £15,771,000 and £4,413,000 respectively, and reducing the profit for the year ended 31 March 2016 by £9,451,000.

Certain key individuals no longer work for the Group and the Directors have assessed that further investigation into the above misstatements would represent a disproportionate cost and effort to the business. As a result, the Directors have not been able to distinguish whether certain of the adjustments, which in aggregate resulted in a £9,451,000 reduction in profit and net assets, related to the year ended 31 March 2016 or to prior periods, and consequently the income statement effect of these adjustments has been recognised wholly within the income statement for the year ended 31 March 2016.

We were appointed as auditors subsequent to the 2016 year end and due to the above circumstances we were unable to obtain sufficient appropriate audit evidence in relation to these misstatements. Any adjustments would have a consequential effect on the Group’s profit for the year ended 31 March 2016 and its net assets at 31 March 2015.

Qualified opinion on financial statements

In our opinion the parent company financial statements:

- give a true and fair view of the state of the parent company’s affairs as at 31 March 2017;

- have been properly prepared in accordance with UK Generally Accepted Accounting Practice; and

- have been prepared in accordance with the requirements of the Companies Act 2006.

In our opinion, except for the possible effect solely on the comparative information for the year ended 31 March 2016 and as at 31 March 2015 of the matters described in the basis for qualified opinion on financial statements paragraph, the group financial statements:

- give a true and fair view of the Group’s state of affairs as at 31 March 2017 and of its loss for the year then ended;

- have been properly prepared in accordance with IFRSs as adopted by the EU; and

- have been prepared in accordance with the requirements of the Companies Act 2006.

Opinion on other matters prescribed by the Companies Act 2006

In our opinion the information given in the Strategic Report and the Directors’ Report for the financial year is consistent with the financial statements.

Based solely on the work required to be undertaken in the course of the audit of the financial statements and from reading the Strategic Report and the Directors’ Report:

- we have not identified material misstatements in those reports; and

- in our opinion, those reports have been prepared in accordance with the Companies Act 2006.

Matters on which we are required to report by exception

In respect solely of the limitation on our work relating to the comparative Group information for the year ended 31 March 2016 and as at 31 March 2015, described above, we have not obtained all the information and explanations that we considered necessary for the purpose of our audit.

We have nothing to report in respect of the following matters where the Companies Act 2006 requires us to report to you if, in our opinion:

- adequate accounting records had not been kept by the parent company, or returns adequate for our audit have not been received from branches not visited by us; or

- the parent company financial statements are not in agreement with the accounting records and returns; or

- certain disclosures of Directors’ remuneration specified by law are not made.

28 Error restatement

On 7 November 2016 Redcentric plc (‘the Group’) announced that an internal review by the Group’s audit committee had discovered misstated balances in the Group’s accounting records and consequently a forensic review of the Group’s net assets was undertaken. Furthermore as part of the forensic review, work was undertaken to validate the previously reported net debt position of the Group.

The findings of the forensic review identified a reduction in net assets of the Group of £14.9m. This misstatement relates to prior periods and subsequently the prior year comparatives have been restated with net assets at 1 April 2015 reducing by £6.0m and as at 31 March 2016 by £14.5m.

Subsequent to this review, the Board have completed a further review of net assets as at 31 March 2016 as part of the finalisation of the 2017 annual report. As a result of this investigation further restatements have been recognised:

- Relating to the consolidation of the Group’s Indian subsidiary.

- Other items, predominantly in relation to misstatement of and taxation and deferred taxation balances.

The cumulative impact of the above adjustments on reported profit for the year ended 31 March 2016 was assessed to be £9.5m.

The following disclosure provides further detail of the composition of these adjustments, with reference to the affected primary statement captions where possible.

Impact of forensic review

Certain assets of the Group recognised as PPE were identified as relating to inventory. Accordingly these assets were reclassified from PPE to inventory (2016: £497k).

Certain amounts relating to accrued income and trade receivables were identified as being irrecoverable. As a result further provisions against receivables balances were recognised and other balances were adjusted against revenue. Overall, this reduced trade and other receivable balances (2016: £1,555k).

Certain customer receipts were recognised in advance of the date of the clearing of associated cash receipts. This resulted in an overstatement of cash and cash equivalents and an understatement of net debt (2016: £8,242k).

In addition, certain cash payments relating to trade creditors were recorded in the wrong period, resulting in an overstatement of cash and cash equivalents and an understatement of net debt (2016: £4,240k).

Certain costs relating to the year ended 31 March 2016 and 31 March 2015 had not been recorded as liabilities at the relevant period end. This resulted in an understatement of trade creditor and accrual balances (2016: £3,193k), along with associated cost of sales and operating expenses balances.

The deferred tax effect of the above items is £2,375k, driven by the increase in tax losses.

These forensic adjustments are consistent with those that were reflected in the financial statements of Redcentric Solutions Limited at 31 March 2016.

India

The assets and liabilities of the Group relating to a subsidiary company, Redcentric Solutions Private Ltd, were previously not consolidated into the Group’s financial statements.

The impact of this restatement is an increase in net assets of £0.4m as at 31 March 2016 with a corresponding increase in profit after tax as at 31 March 2016 of £0.4m.

Other

Certain assets of the Group relating to capitalised software were identified to have been recognised as part of property, plant and equipment instead of as an intangible asset. Accordingly management have reclassified these assets from PPE to intangible assets (2016: £2,242k).

In addition, certain purchases of property plant and equipment were recorded in the wrong period, resulting in an understatement of assets and trade payables (2016: £41k).

A further adjustment to reduce the intangibles balance by £317k has been recorded at 31 March 2016, relating to a reduction in carrying value.

Certain items of expenditure were incorrectly capitalised within the inventory caption and an adjustment was required to correct this (2016: £68k).

Further amounts relating to accrued income and trade receivables were identified as being irrecoverable. As a result further provisions against receivables balances were recognised in addition to the writing off of certain balances, reducing trade and other receivable balances (2016: £3,604k).

Borrowings falling due within one year were reclassified to the current liabilities caption (£523k).

A corporation tax receivable was not recorded (2016: £531k), and an increase to the deferred tax liability (2016: £356k) was recognised as a result of these other adjustments being recorded.

The forensic review identified certain costs relating to the year ended 31 March 2016 and 31 March 2015 as not having been recorded at the relevant period end. However some of these costs had already been accrued for and therefore needed to be reversed to avoid double counting. This adjustment resulted in a reduction of trade creditor and accrual balances (2016: £2,500k), along with associated cost of sales and operating expenses balances.

The accounting misstatements are discussed on pages 9-11 of the financial performance review. The impact of the prior year adjustments on the Group’s income, equity and cash flows arising from the restatement exercise are summarised on pages 77-81.