Swisscom Ltd – Annual report – 31 December 2025

Industry: telecoms

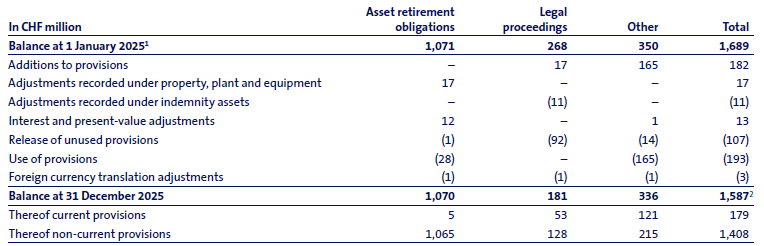

3.5 Provisions and contingent liabilities (extract 1)

Provisions

1 Incl. adjustments to the final purchase price allocation of Vodafone Italia. See Note 5.3.

2 Provisions of CHF 78 million are covered by indemnity assets relating to the acquisition of Vodafone Italia. See Note 5.3.

Provisions for asset retirement obligations

The provision for asset retirement obligations is determined based on estimated future cash outflows and discounted using an average discount rate of 1.23% (previous year: 0.86%). In 2025, adjustments resulting from reassessments in the amount of CHF 15 million were recognised as an adjustment to the carrying amount of property, plant and equipment, with no impact on the income statement. Of this amount, CHF –10 million related to changes in discount rates and CHF 25 million to updates of the cost index and other assumptions applied in determining asset retirement costs. A 10% increase in the estimated asset retirement costs would result in an increase of CHF 118 million in the provision. A deferral of the retirement activities by ten years would increase the provision by CHF 48 million.

3.5 Provisions and contingent liabilities (extract 2)

Significant judgements or estimates

The provisions for asset retirement obligations relate to the dismantling of telecommunications installations and transmitter stations as well as the restoration of sites owned by third parties to their original condition. The amount of these provisions depends primarily on estimates of future asset retirement costs and the expected timing of dismantlement. Provisions and contingent liabilities for legal proceedings primarily relate to regulatory and competition law proceedings. The legal and accounting assessment of these proceedings involves significant estimation uncertainties and judgement regarding the probability of occurrence and the potential amount of any cash outflows. The recognised provisions represent management’s best estimate of the obligation as at the reporting date. Possible obligations whose existence as at the reporting date cannot be determined, or for which the amount cannot be measured reliably, are presented as contingent liabilities.

Accounting policies

Provisions are recognised when Swisscom has a present legal or constructive obligation as a result of past events, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount can be made. Where the effect of the time value of money is material, provisions are measured at the present value of the expected expenditure to settle the obligation.

Provisions for asset retirement obligations

Swisscom is legally obligated to dismantle transmitter stations and telecommunications installations located on land owned by third parties upon decommissioning, and to restore such sites to their original condition. The estimated cost of asset retirement is capitalised as part of the costs of the related assets and is amortised over their useful lives. The provisions are measured at the present value of the expected future asset retirement costs and is presented under non-current provisions. When the provision is re-measured, any change in its present value is added to or deducted from the carrying amount of the related asset. A reduction in the asset’s carrying amount is limited to its recoverable amount; any excess reduction is recognised immediately in the income statement.