RS Group plc – Annual report – 31 March 2025

Industry: distribution

23 Financial risk management (extract)

Capital management

The Board’s policy is to maintain a strong capital base always, with an appropriate debt to equity mix, to ensure investor, creditor and market confidence and to support the future development of the business. The Board monitors ROCE (Note 3) and the level of dividends to ordinary shareholders.

The Group seeks to raise debt from a variety of sources and with a variety of maturities. See Note 22 for further details.

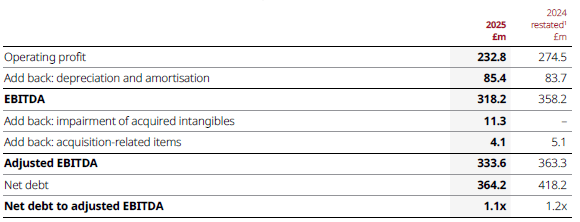

The Group’s debt covenants are net debt to adjusted EBITDA to be less than 3.25 times and EBITA to interest to be greater than 3 times, which are measured on a rolling 12-month basis at half year and year end. At the year end the Group comfortably met these covenants with net debt to adjusted EBITDA of 1.1x (2023/24 restated: 1.2x) and EBITA to interest of 10.9x (2023/24 restated: 10.3x).

There were no significant changes in the Group’s approach to capital management during the year.

3 Alternative Performance Measures (APMs) (extracts)

Adjusted profit measures

These are the equivalent UK IAS measures adjusted to exclude amortisation and impairment of intangible assets arising on acquisition of businesses, acquisition-related items, substantial reorganisation costs, substantial asset write-downs, one-off pension credits or costs, significant tax rate changes and, where relevant, associated income tax effects. Adjusted profit before tax is a performance measure for the annual incentive and the all employee Long Term Incentive Plan (LTIP) called the RS YAY! Award. Adjusted earnings per share is a performance measure for the LTIP and Journey to Greatness (J2G) LTIP Award. Adjusted operating profit conversion, adjusted operating profit margin and adjusted earnings per share are financial key performance indicators (KPIs) which are used to measure the Group’s progress in delivering the successful implementation of its strategy and monitor and drive its performance.

1. Operating profit margin is operating profit expressed as a percentage of revenue.

2. Operating profit conversion is operating profit expressed as a percentage of gross profit.

3. Please refer to Note 32 for further details of the restatement.

During the year, the customer contracts, relationships and distribution agreements were assessed for impairment. As a result of that review, the asset related to the acquisition of IESA was fully impaired, with an impairment cost of £10.9 million. In addition, £0.4 million of software acquired with IESA was also impaired.

Acquisition-related items comprise transaction costs directly attributable to the acquisition of businesses, any deferred consideration payments relating to the retention of former owners and key employees of acquired businesses expensed as remuneration, adjustments to acquisition-related indemnification assets and the related liabilities that result from events after the acquisition date and any remeasurements of contingent consideration payable on acquisition of businesses that result from events after the acquisition date.

Included in acquisition-related items for the year ended 31 March 2025 was £2.1 million in respect of legal costs for an ongoing dispute.

Included in acquisition-related items for the year ended 31 March 2024 was the release of the £0.4 million contingent consideration payable on acquisition of domnick hunter-RL (Thailand) Co., Ltd. given the conditions for payment were not met.

Earnings before interest, tax, depreciation and amortisation (EBITDA), net debt and net debt to adjusted EBITDA

EBITDA is operating profit excluding depreciation and amortisation. Net debt to adjusted EBITDA (one of the Group’s debt covenants) is the ratio of net debt to EBITDA excluding impairment of intangible assets arising on acquisition of businesses, acquisition-related items, substantial reorganisation costs, substantial asset write-downs and one-off pension credits or costs on an annualised basis covering the preceding twelve-month period. Net debt comprises cash and cash equivalents, borrowings and lease liabilities and is reconciled in Note 22.

1. Please refer to Note 32 for further details of the restatement.

Earnings before interest, tax and amortisation (EBITA) and EBITA to interest

EBITA is adjusted EBITDA after depreciation. EBITA to interest (one of the Group’s debt covenants) is the ratio of EBITA to finance costs including capitalised interest less finance income (interest per debt covenants).

1. Please refer to Note 32 for further details of the restatement.

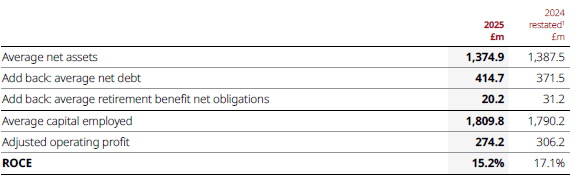

Return on capital employed (ROCE)

ROCE is adjusted operating profit expressed as a percentage of monthly average net assets excluding net cash/debt and retirement benefit obligations and is an underpin for the LTIP and J2G LTIP Award and a financial KPI.

1. Please refer to Note 32 for further details of the restatement.