Vodafone Group Plc – Half year report – 30 September 2022

Industry: telecoms

10 Post employments benefits

Significant movements have been recorded in respect of the gross assets held by and liabilities of the Group’s pension schemes in the period. The Group has obtained valuations for its most material schemes in the UK, Germany and Ireland. Key financial information is presented below.

The Group’s plan liabilities are measured using the projected unit credit method using the principal actuarial assumptions set out below.

Assumptions relating to life expectancy are unchanged from 31 March 2022.

Charges made to the consolidated income statement and consolidated statement of comprehensive income (‘SOCI’) on the basis of the assumptions stated above are:

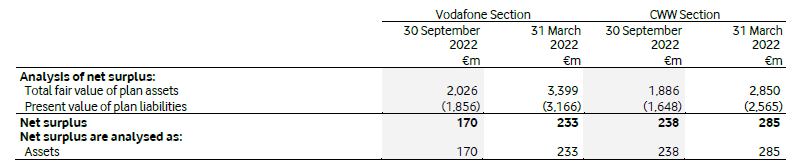

The Group’s overall net surplus is analysed as follows:

An analysis of the net surplus is provided below for the Vodafone UK Group Pension Scheme, comprising the Vodafone Section and the Cable & Wireless Section (‘CWW Section’).