FIFA – Annual report – 31 December 2016

Industry: sport and leisure

FINANCIAL REVIEW (extract)

EARLY ADOPTION OF IFRS 15 – REVENUE FROM CONTRACTS WITH CUSTOMERS

Under its new administration, FIFA strictly adheres to the International Financial Reporting Standards (IFRS) when preparing its annual financial statements. In May 2014, the International Accounting Standards Board and the Financial Accounting Standards Board jointly issued a new revenue standard: “IFRS 15 – Revenue from Contracts with Customers”, which will replace the existing IFRS revenue guidance. New qualitative and quantitative disclosure requirements aim to offer financial statement users greater clarity on the nature, amount, timing and uncertainty of revenue and cash flow arising from contracts with customers. Application of the IFRS 15 standard in annual reporting periods will be mandatory as of 1 January 2018.

To further strengthen the transparency of FIFA’s financial reporting and help its stakeholders better understand its financial position, FIFA has decided to adopt the IFRS 15 standard early, leading the way in the implementation of IFRS 15. With all years of the 2015-2018 cycle calculated using the same methodology, FIFA can also interpret the revenue and expenses of each year in a comparable and compatible way.

In the preparation of the 2016 financial statements, FIFA has applied the five-step model under IFRS 15 to determine when to recognise revenue, and in what amount, by:

- identifying the contracts with customers;

- identifying the separate performance obligations;

- determining the transaction price;

- allocating the transaction price to the separate performance obligations; and

- recognising revenue when each performance obligation is satisfied.

In FIFA’s previous financial statements, revenue was recognised according to a proportional timing method, even though most of FIFA’s revenue contracts contain one or more non-proportional performance obligation over the four-year cycle.

Compared with the previous accounting system, the new IFRS 15 standard leads FIFA to adopt a later pattern of revenue recognition because its flagship tournament, the FIFA World Cup™ – which delivers the majority of contractual performance obligations with FIFA’s Partners, Sponsors and customers – takes place in the final year of the financial cycle. Consequently, the new pattern of revenue recognition leads to a different allocation of costs, and so the expenses related to the FIFA World Cup are also deferred. The way in which revenue and contract costs are recognised is presented in detail in chapter 4: Financial Report.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (extract)

Adoption of new standards

FIFA has been early in adopting the new “IFRS 15 – Revenue from Contracts with Customers”, including amendments to IFRS 15 (clarifications), for the 2016 financial year. FIFA has applied the full retrospective transition method, resulting in adjustments to the comparative period, 2015. As a result, FIFA has changed its accounting policy for revenue recognition (as explained under “E Revenue recognition” below).

IFRS 15 replaces the existing standards IAS 11, IAS 18 and all revenue-related interpretations. IFRS 15 changes the basis for deciding whether revenue is to be recognised over time or at a particular point in time and expands and improves disclosures about revenue.

The core principle of IFRS 15 is to recognise revenue that depicts the transfer of promised goods or services to the customer in an amount that reflects the consideration to which FIFA expects to be entitled in exchange for those goods or services. To recognise revenue, IFRS 15 defines a five-step process that includes: identifying the contract(s) with the customer, identifying the performance obligations in the contract, determining the transaction price, allocating the transaction price and recognising revenue when a performance obligation is satisfied.

There was no material impact as at 1 January 2015. This is primarily a result of FIFA following a four-year business cycle, which started with the FIFA Women’s World Cup 2015™ in Canada and will end with the 2018 FIFA World Cup™ in Russia.

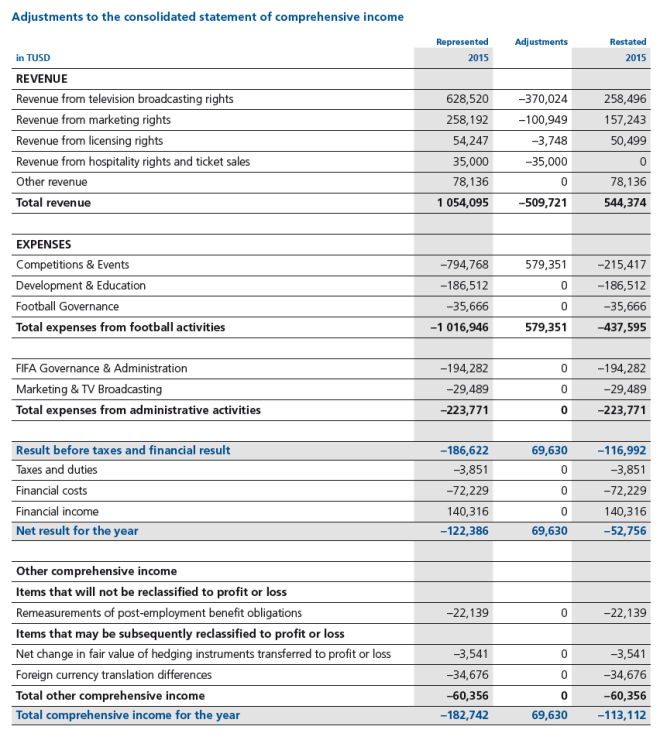

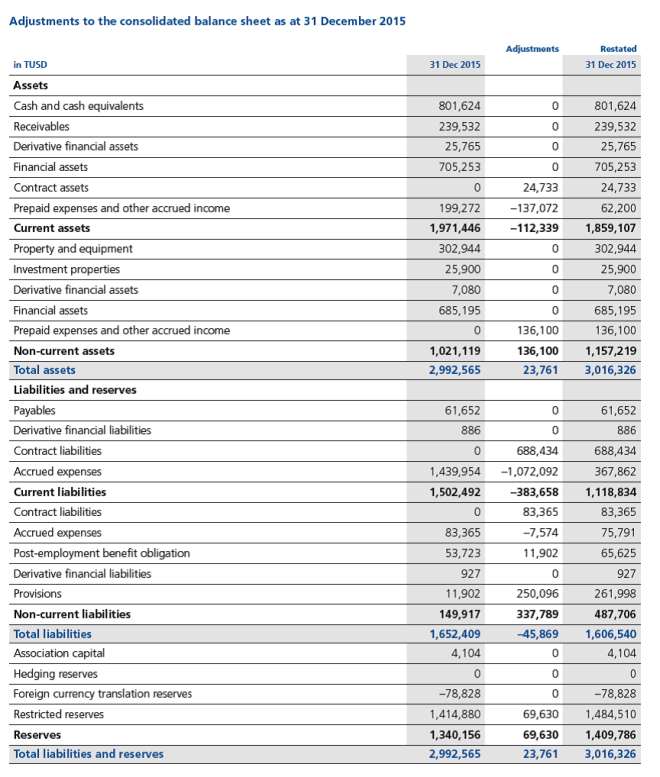

The following tables summarise the adjustments posted in FIFA’s consolidated financial statement as a result of the retrospective application of IFRS 15.

Also included in the figures stated below is a consolidated balance sheet reclassification of USD 262.0 million from accrued expenses to provisions (see also Note 24) and a reclassification of USD 11.9 million from provisions to post-employment benefit obligation (see also Note 28).

E REVENUE RECOGNITION

The main revenue streams for FIFA relate to the sale of the following rights:

- Television broadcasting rights

- Marketing rights

- Licensing rights

- Hospitality rights

- Ticket sales

The transaction price of a contract consists in general of fixed and variable consideration as well as, infrequently, non-cash components (value in kind).

Nature of performance obligations

The following is a description of the principal activities with which FIFA generates revenue:

Television broadcasting rights are granted primarily to TV stations and other broadcasting institutions. These rights are granted to broadcast the television signal for a defined period in a particular territory. The performance obligation is defined as the right to access intellectual property. Revenue related to television broadcasting rights is recognised over the rights period measured based on the pattern of broadcasting of the contractual events.

Marketing rights provide the FIFA Partners, FIFA World Cup Sponsors, and Regional and National Supporters with access to intellectual property by enabling them to enter into a long-term strategic alliance with FIFA which also includes a set of predefined rights. The performance obligations

under marketing rights contracts consist of both tangible and intangible marketing rights, which are separated. The tangible rights include event-related media and advertising rights which result in revenue recognition as the contractual events are broadcast. The intangible right is attributed to the promise to benefit from a strategic association with FIFA, its competitions and brand, resulting in a straight-line recognition of revenue over the contractual rights period.

Licensing rights are granted to licensees to both associate the licensee with FIFA and the FIFA competitions and obtain the right to use FIFA marks and brand elements as a platform to brand its related products and services. As the licensee has access to intellectual property, the amount of revenue is recognised over the rights period and is further determined by categorising each licensing right contract as follows:

- For the right to consideration of fixed fees only, revenue is recognised over the rights period on the basis of fixed-fee amounts.

- For the right to consideration of sales- or usage-based royalties with specified minimum guarantee amounts, FIFA assesses at each reporting date whether the royalty amounts to be received will exceed the contractual minimum guarantee threshold.

a. If the sales-based royalty is not expected to clearly exceed the minimum guarantee threshold, revenue is recognised over the rights period measured on the basis of the fixed guaranteed consideration. Any royalties received in one period in excess of the minimum guarantee due are deferred and recognised only when total royalties received exceed the contractual minimum guarantee threshold.

b. When FIFA has a reasonable expectation that royalty amounts to be received will clearly exceed the contractual minimum guarantee threshold, fixed and variable considerations are estimated and revenue is recognised as the performance obligation is satisfied. The amount of revenue recognised for the reporting period is subject to the royalty constraint (i.e. cumulative revenue amounts cannot exceed cumulative royalty amounts).

Hospitality rights provide the licensee with the right to provide hospitality and ticketing services for selected FIFA competitions, including the FIFA Women’s World Cup 2015™, the FIFA Confederations Cup Russia 2017 and the 2018 FIFA World Cup Russia™. The amount of revenue for the FIFA World Cup includes both fixed and variable considerations, whereas all other events have variable considerations only. Contractually determined fixed payments are recognised in the period in which the FIFA World Cup takes place. Revenue based on profit share agreements is recognised once the profit share for the event has been determined by the licensee.

Ticket sales in connection with the FIFA Confederations Cup Russia 2017 and the 2018 FIFA World Cup Russia are recognised in the year the event takes place.

Revenue from rendering of services is recognised in the accounting period in which the services are rendered.

Value-in-kind revenue consists of promises to receive predetermined services and the delivery of goods to be used in connection with the 2018 FIFA World Cup Russia or other FIFA events. The revenue related to value in kind forms part of the overall consideration receivable and is recognised applying the same measure of progress as the performance obligation it relates to. Value-in-kind consideration is measured at fair value.

Practical expedients

FIFA has elected to make use of the following practical expedients:

- Completed contracts under IAS 11 and IAS 18 before the date of transition have not been reassessed. ¢ Contract costs incurred related to contracts with an amortisation period of less than one year have been expensed as incurred.

- FIFA applies the practical expedient in paragraph 121 of IFRS 15 and does not disclose information about remaining performance obligations that have original expected durations of one year or less.

- FIFA also applies the practical expedient in paragraph C5(d) of IFRS 15 and does not disclose the amount of the transaction price allocated to the remaining performance obligations and an explanation of when FIFA expects to recognise that amount as revenue for the year ended 31 December 2015.

V SIGNIFICANT ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS (extract)

Revenue recognition

As set out in Note E, IFRS 15 – Revenue Recognition from Contracts with Customers requires judgments and estimates. Judgement relates to the determination of performance obligations in each of the major revenue streams, having the potential to impact the revenue recognition pattern under the contract. Furthermore, the allocation of consideration to different performance obligations requires estimation of the stand-alone selling price of each of these. Assumptions are required to determine an appropriate measure of progress when determining how control over promised goods or services transfers to the customer. All of the above have the potential to result in a different revenue recognition pattern.

NOTES TO THE CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME (extracts)

Television broadcasting rights are granted primarily to TV stations and other broadcasting institutions. These rights are granted to broadcast the television signal for a defined period in a particular territory. Revenue from television broadcasting rights is recognised when the actual broadcasting of the event in question takes place and is contingent on the number of broadcasting hours. As a consequence, a comparison against previous years is not meaningful. Until a full cycle has been presented according to IFRS 15 to provide a basis for comparison, revenue should be analysed considering the full four-year cycle of FIFA.

Other broadcasting revenue reflects value-in-kind considerations as well as additional revenue for services during the events in order to fulfill FIFA’s broadcasting obligations.

Revenue from broadcasting rights contracts, which include the right to broadcast other FIFA events for the years 2015 and 2016, but excluding the FIFA World Cup™ are presented as “Other FIFA event revenue”. Such other FIFA events for the year 2016 are the FIFA U-20 World Cup Papua New Guinea 2016, the FIFA U-17 World Cup Jordan 2016, the FIFA Futsal World Cup Colombia 2016, the FIFA Club World Cup Japan 2016, the Blue Stars/FIFA Youth Cup 2016 and the FIFA Interactive World Cup 2016.

Marketing rights provide the FIFA Partners with access to intellectual property by enabling them to enter into a long-term strategic alliance with FIFA which also includes a set of predefined rights. These rights are further split into tangible and intangible rights. Revenue for tangible marketing rights is recognised when the event in question is broadcast and is entirely dependent on the number of broadcasting hours. As such, due to the different nature and lower number of broadcasting hours of FIFA competitions in 2016, the revenue for the year is, logically, lower than that for 2015. A direct comparison of the two years is therefore not helpful. Until a full cycle has been presented according to IFRS 15 to provide a basis for comparison, revenue should be analysed considering the full four-year cycle of FIFA. National Supporters and Event Sponsors only have the contractual right for one single event in connection with the FIFA U-20 World Cup Papua New Guinea 2016, the FIFA U-17 World Cup Jordan 2016, the FIFA Futsal World Cup Colombia 2016, the FIFA Club World Cup Japan 2016, the Blue Stars/FIFA Youth Cup 2016 and the FIFA Interactive World Cup 2016. As a consequence, revenue for these contracts is recognised in the period in which the event takes place.

In 2016, the value of the services or goods received (i.e. value-in-kind consideration) amounted to USD 6.9 million (2015: USD 10.9 million) and is included in the revenue amounts recognised from marketing rights with FIFA Partners.

Brand licensing rights are related to FIFA marks and brand elements in connection with FIFA World Cup™ products and services.

Licensing rights from products and services for other FIFA events in 2016 – the FIFA U-20 World Cup Papua New Guinea 2016, the FIFA U-17 World Cup Jordan 2016, the FIFA Futsal World Cup Colombia 2016, the FIFA Club World Cup Japan 2016, the Blue Stars/FIFA Youth Cup 2016 and the FIFA Interactive World Cup 2016 – are presented as other licensing rights.

The majority of the licensing rights contracts consist of royalty payments with a specified minimum guarantee threshold. FIFA reassesses these contracts after each reporting period, whether or not the royalty amounts to be received will exceed the contractual minimum guarantee threshold. Where the expected total royalties to be received for significant contracts clearly exceed the minimum threshold, these have been estimated and included in the transaction price. This has resulted in an increased revenue of brand licensing in 2016 compared to 2015 as significant royalty amounts have been recognised, which were deferred throughout prior periods.

In 2016, the value of the services or goods received (i.e. value-in-kind consideration) amounted to USD 3.7 million (2015: USD 3.3 million) and is included in the revenue amounts recognised from licensing rights.

Hospitality rights have been granted to MATCH Hospitality AG for a fixed consideration of USD 140 million plus a variable profit-sharing component for the 2018 FIFA World Cup Russia™. The FIFA Women’s World Cup Canada 2015™ and FIFA Confederations Cup Russia 2017 have profit-share agreements only.

Ticket sales for the FIFA Confederations Cup Russia 2017 and the 2018 FIFA World Cup Russia™ are recognised in the year the event takes place.

Other revenue is recognised in the accounting period in which the services are rendered. It comprises, namely, revenue generated from the FIFA Club World Cup, the contributions received related to the Olympic Football Tournaments Rio 2016 and the FIFA Quality Programme. The latter contains revenue in connection with the test programmes for footballs, football turf and goal-line technology.

Rent income from real estate increased in lockstep with the opening of the FIFA World Football Museum, since the property used for the museum also contains apartments, which FIFA is renting out. Revenue from prior cycles and other includes various smaller sources of revenue such as revenue generated from players’ status-related proceedings and revenue from prior cycles. The majority of revenue shown in “other” in 2015 relates to revenue which is linked to the 2011-2014 cycle, and which is recorded in this category so as not to dilute any other revenue category with revenue, which should not belong in this cycle but was only recognised after 2014 was closed.

17 CONTRACT ASSETS

Contract assets relate to FIFA’s rights of consideration for services provided. In 2016 and 2015, there was no impairment loss in relation to the contract assets.

Significant changes in contract asset balances during the period are as follows:

FIFA has recognised contract acquisition costs arising from the capitalisation of incremental agency fees. These costs have been incurred in order to obtain certain Asian television broadcasting right and FIFA Partner contracts. FIFA expects that the fees paid are recoverable and there was no impairment loss in relation to the costs capitalised.

The above table includes revenue expected to be recognised in FIFA’s current four-year business cycle ending with the FIFA World Cup™ in 2018 and is related to performance obligations that are unsatisfied during the reporting period. Revenue from unsatisfied performance obligations at 31 December 2016, which are expected to be recognised in the cycles ending in 2022, 2026 and 2030 amount to USD 5’208 million. Contracted revenue will be recognised in line with the transfer of control over goods and services as described in Note E.

23 CONTRACT LIABILITIES

Contract liabilities relate to payments received in advance of FIFA’s performance under a contract. Contract liabilities are recognised as revenue as (or when) FIFA performs under the contract and control over the transfer of contractually agreed goods or services to the customer.