BP p.l.c. – Annual report – 31 December 2025

Industry: oil and gas

1. Material accounting policy information, significant judgements, estimates and assumptions (extract)

Inventories

Inventories, other than inventories held for short-term trading purposes, are stated at the lower of cost and net realizable value. Cost is typically determined by the first-in first-out method and comprises direct purchase costs, cost of production, transportation and manufacturing expenses. Net realizable value is determined by reference to prices existing at the balance sheet date, adjusted where the sale of inventories after the reporting period gives evidence about their net realizable value at the end of the period.

Inventories held for short-term trading purposes are stated at fair value less costs to sell and any changes in fair value are recognized in the income statement.

Supplies are valued at the lower of cost on a weighted-average basis and net realizable value.

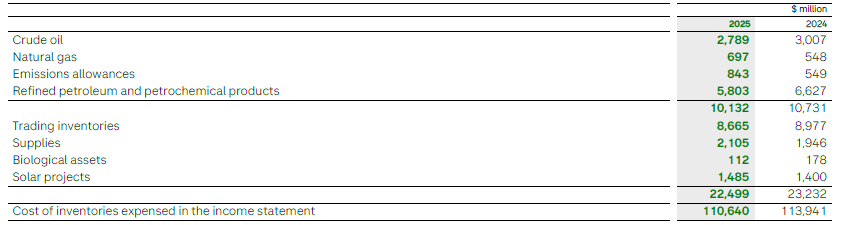

19. Inventories

The inventory valuation at 31 December 2025 is stated net of a provision of $475 million (2024 $388 million) to write down inventories to their net realizable value, of which $277 million (2024 $199 million) relates to hydrocarbon inventories. The net charge to the income statement in the year in respect of inventory net realizable value provisions was $137 million (2024 $77 million credit), of which $73 million charge (2024 $104 million credit) related to hydrocarbon inventories.

Trading inventories are valued using quoted benchmark prices adjusted as appropriate for location and quality differentials. They are predominantly categorized within level 2 of the fair value hierarchy.