Nikon Corporation – Annual report – 31 March 2017

Industry: manufacturing

- Basis of Preparation (extract)

(1) Compliance with IFRS and First-Time Adoption of IFRS

Since the Company is classified as a “Specified Company under Designated IFRS” as provided in Article 1-2 of the Ordinance on Consolidated Financial Statements, the consolidated financial statements have been prepared in accordance with IFRS.

The Group first adopted IFRS for the fiscal year ended March 31, 2017, with the date of transition to IFRS as of April 1, 2015 (hereinafter referred to as the “transition date”). The impacts on the financial position, results of operations, and cash flows derived from transition to IFRS are described in Note 40. First-Time Adoption of IFRS.

- First-time Adoption of IFRS

The Group has disclosed its consolidated financial statements in accordance with IFRS from the year ended March 31, 2017. The most recent consolidated financial statements prepared in accordance with Japanese generally accepted accounting principles (hereafter, “Japanese GAAP”) are for the year ended March 31, 2016. The date of transition to IFRS is April 1, 2015.

In principle, IFRS 1 requires first-time adopters to apply IFRS retrospectively. However, for some aspects of the requirements, IFRS 1 defines exceptions to and exemptions from retrospective application.

(Exceptions to the retrospective application under IFRS 1)

IFRS 1 prohibits retrospective application of estimates, derecognition of financial assets and financial liabilities, hedge accounting, and non-controlling interests and requires an entity to apply these items prospectively from the transition date.

(Exemptions from the retrospective application under IFRS 1)

The exemptions from the retrospective application that the Group has applied are described as follows.

- Business combinations

The Group has elected not to apply IFRS 3 Business Combinations retrospectively in regard to business combinations that occurred prior to the transition date. Goodwill that arose from the business combinations prior to the transition date was reported at carrying amount under Japanese GAAP less impairment losses recognized as a result of the impairment test as of the transition date in accordance with IAS 36.

- Exchange differences on translation of foreign operations

The Group has transferred all cumulative exchange differences on translation of foreign operations to retained earnings as of the transition date.

The statements of reconciliation are disclosed as follows, as required at the first- time adoption of IFRS.

The “Reclassifications” column in each reconciliation statement represents the items that do not affect retained earnings and comprehensive income. The “Differences in recognition and measurement” column in each reconciliation statement represents the items that affect retained earnings or comprehensive income.

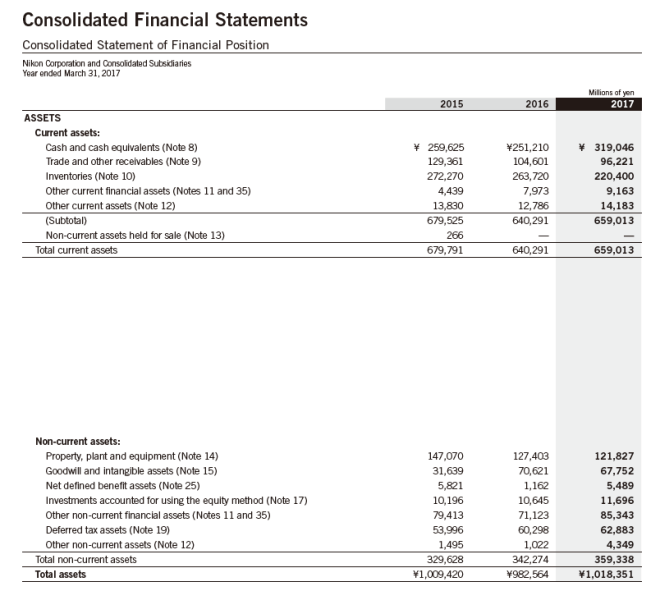

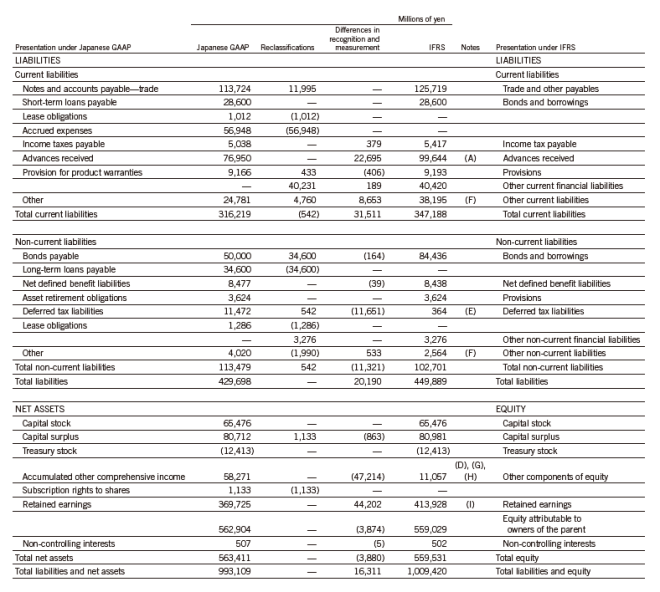

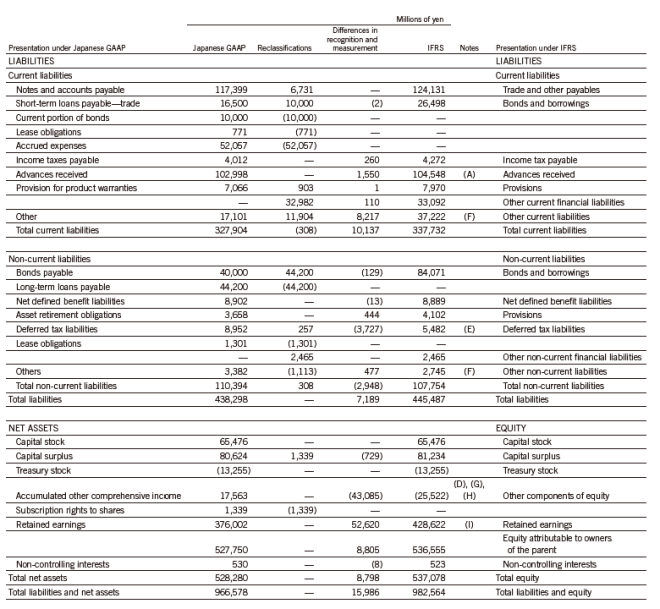

(1) Reconciliation of Equity

Reconciliation of Equity as of April 1, 2015 (At the Transition Date to IFRS)

Reconciliation of Equity as of March 31, 2016 (the End of the Previous Year)

Reconciliation of Equity as of April 1, 2015 (the Transition Date) and March 31, 2016 (the End of the Previous Year)

(Notes to Reconciliations of Equity)

The major reconciliations between Japanese GAAP and IFRS as presented in the statements of reconciliation of equity are described as follows:

(A) Revenue Recognition

Under Japanese GAAP, the Group has recognized revenue from sales of products that require installation upon completion of inspection by the customer. Under IFRS, however, revenue is recognized upon the completion of installation. As a result, under IFRS, “Trade and other receivables” as of April 1, 2015 and March 31, 2016 increased ¥626 million and ¥9 million, respectively; “Inventories” as of April 1, 2015 and March 31, 2016 increased ¥14,829 million and ¥645 million, respectively; and “Advances received” as of April 1, 2015 and March 31, 2016 increased ¥22,298 million and ¥1,004 million, respectively, compared with those accounted for under Japanese GAAP.

(B) Intangible Assets

Under Japanese GAAP, the Group has expensed research and development costs as incurred. Under IFRS, however, certain development costs that satisfy the capitalization requirements of development costs are capitalized. As a result, under IFRS, “Goodwill and intangible assets” as of April 1, 2015 and March 31, 2016 increased ¥3,257 million and ¥4,351 million, respectively, compared with those accounted for under Japanese GAAP.

(C) Goodwill

Under Japanese GAAP, the Group has amortized goodwill over the estimated useful life. Under IFRS, however, goodwill is not amortized and no amortization has been recognized since the date of transition to IFRS. Amortization of goodwill under Japanese GAAP after the transition date is adjusted in retained earnings. As a result, under IFRS, “Goodwill and intangible assets” as of March 31, 2016 increased ¥2,353 million, compared with those accounted for under Japanese GAAP.

(D) Equity Instruments

Under Japanese GAAP, the Group has recognized gains or losses on sales of equity instruments and impairment losses in profit or loss. Under IFRS, however, certain equity instruments have been designated to be classified as financial instruments measured at fair value through other comprehensive income, of which the changes in fair value are recognized in other comprehensive income and transferred to retained earnings at the derecognition of such equity instruments. As a result, under IFRS, “Other components of equity” as of April 1, 2015 and March 31, 2016 decreased ¥9,953 million and ¥9,436 million, respectively, compared with those accounted for under Japanese GAAP.

(E) Deferred Taxes

Under Japanese GAAP, deferred tax for the elimination of unrealized profit is measured using the effective tax rate of the seller. Under IFRS, however, it is required to use the buyer’s effective tax rate for deferred tax calculation.

Under IFRS, the Group recognizes deferred tax assets to the extent that it is probable that taxable profit of the Group will be available against which the temporary difference can be utilized.

(F) Paid Leave

Under IFRS, the Group recognizes a liability for unused paid leave, whereas there is no specific requirement for the accounting treatment under Japanese GAAP. As a result, under IFRS, “Other current liabilities” as of April 1, 2015 and March 31, 2016, increased ¥7,879 million and ¥7,891 million, respectively; and “Other non-current liabilities” as of April 1, 2015 and March 31, 2016 increased ¥557 million and ¥532 million, respectively, compared with those accounted for under Japanese GAAP.

(G) Adjustments on Defined Benefit Plans

Under IFRS, when there is a surplus in a defined benefit plan, the net defined benefit asset is measured at the lower of the surplus in the defined benefit plan and the asset ceiling, and the adjustment for the asset ceiling is recognized in other comprehensive income. On the other hand, there is no specific requirement for the accounting treatment under Japanese GAAP. As a result, under IFRS, “Net defined benefit assets” as of April 1, 2015 and March 31, 2016 decreased ¥3,799 million and ¥524 million, respectively, compared with those accounted for under Japanese GAAP.

(H) Exchange Differences on Translation of Foreign Operations

The Group has applied the exemption defined in IFRS 1, whereby all the cumulative exchange differences as of the transition date have been transferred from accumulated other comprehensive income to retained earnings. As a result, under IFRS, “Retained earnings” as of April 1, 2015 and March 31, 2016 increased ¥40,347 million, compared with those accounted for under Japanese GAAP.

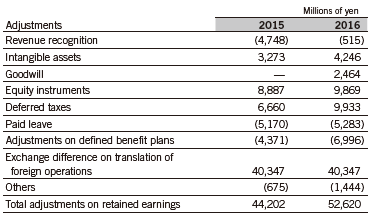

(I) Retained Earnings

The adjustments on retained earnings due to the transition to IFRS are as follows:

(Reclassifications)

The major reclassifications made for the transition to IFRS are as follows:

- Time deposits beyond three months of maturities at acquisition are reclassified to “Other current financial-assets” under current assets.

- Deferred tax assets and deferred tax liabilities that were presented as current items under Japanese GAAP have been reclassified to non-current items under IFRS.

- “Investments accounted for using the equity method” are disclosed separately.

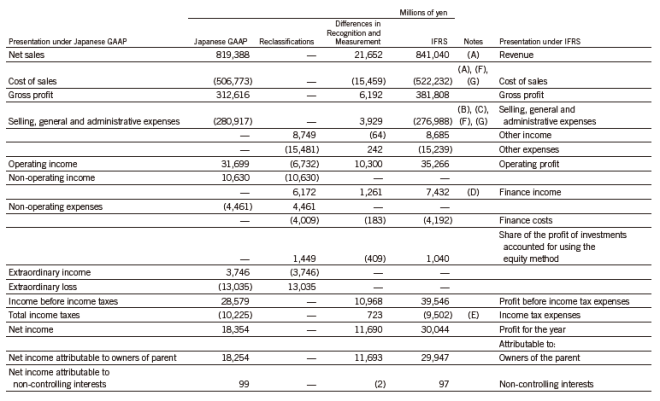

(2) Reconciliation of Profit or Loss and Comprehensive Income

Reconciliation of Profit or Loss and Comprehensive Income for the Year Ended March 31, 2016

Reconciliations of Profit or Loss and Comprehensive Income for the Year Ended March 31, 2016

(Notes to Reconciliations of Profit or Loss and Comprehensive Income)

The major reconciliations between Japanese GAAP and IFRS as presented in the statements of reconciliation of profit or loss and comprehensive income are described as follows.

(A) Revenue Recognition

Under Japanese GAAP, the Group has recognized revenue from sales of products that require installation upon completion of inspection by the customer. Under IFRS, however, revenue is recognized upon the completion of installation. As a result, under IFRS, “Revenue” and “Cost of sales” stated in the consolidated statement of profit or loss for the year ended March 31, 2016 increased ¥21,648 million and ¥15,469 million, respectively, compared with those accounted for under Japanese GAAP.

(B) Intangible Assets

Under Japanese GAAP, the Group has expensed research and development costs as incurred. Under IFRS, however, certain development costs that satisfy the capitalization requirements of development costs are capitalized and amortized over the estimated useful life. As a result, under IFRS, “Selling, general and administrative expenses” stated in the consolidate statement of profit or loss for the year ended March 31, 2016 decreased ¥1,228 million, compared with those accounted for under Japanese GAAP.

(C) Goodwill

Under Japanese GAAP, the Group has amortized goodwill over the estimated useful life. Under IFRS, however, goodwill is not amortized and no amortization has been recognized since the date of transition to IFRS. As a result, under IFRS, “Selling, general and administrative expenses” stated in the consolidated statement of profit or loss for the year ended March 31, 2016 decreased ¥2,464 million, compared with those accounted for under Japanese GAAP.

(D) Equity Instruments

Under Japanese GAAP, the Group has recognized gains or losses on sales of equity instruments and impairment losses in profit or loss. Under IFRS, however, certain equity instruments have been designated to be classified as financial instruments measured at fair value through other comprehensive income, of which the changes in fair value are recognized in other comprehensive income and transferred to retained earnings at the derecognition of such equity instruments.

(E) Deferred Taxes

Under Japanese GAAP, deferred tax for the elimination of unrealized profit is measured using the effective tax rate of the seller. Under IFRS, however, it is required to use the buyer’s effective tax rate for deferred tax calculation.

In addition, under IFRS, the Group recognizes deferred tax assets to the extent that it is probable that the taxable profit of the Group will be available against which deductible temporary differences can be utilized.

(F) Paid Leave

Under IFRS, the Group recognizes a liability for unused paid leave, whereas there is no specific requirement for the accounting treatment under Japanese GAAP.

(G) Adjustments on Defined Benefit Plans

Under Japanese GAAP, the Group has recognized the actuarial gain and loss in other comprehensive income as incurred, and subsequently amortized them through profit or loss over a certain period within the average remaining service period of employees. Under IFRS, however, the actuarial gains and losses are recognized in other comprehensive income as incurred and immediately transferred to retained earnings. As a result, under IFRS, “Cost of sales” and “Selling, general and administrative expenses” stated in the consolidated statement of profit or loss for the year ended March 31, 2016, decreased ¥120 million and ¥857 million, respectively, compared with those accounted for under Japanese GAAP.

In addition, under IFRS, when there is a surplus in a defined benefit plan, the net defined benefit asset is measured at the lower of the surplus in the defined benefit plan and the asset ceiling, and the adjustment for the asset ceiling is recognized in other comprehensive income. On the other hand, there is no specific requirement for the accounting treatment under Japanese GAAP.

(Reclassifications)

The major reclassifications made for the transition to IFRS are as follows:

For the items presented under Japanese GAAP as “Non-operating income,” “Non-operating expenses,” “Extraordinary income,” and “Extraordinary expenses,” under IFRS, those related to the finance and foreign exchange gain or loss are presented as “Finance income” or “Finance costs,” and the items other than the above are presented as “Other income,” “Other expenses,” and “Share of the profit of investments accounted for using the equity method.”

(3) Reconciliation of Cash Flows

There were no material differences between the consolidated statement of cash flows prepared under IFRS and that prepared under Japanese GAAP.