Tesco PLC – Annual report – 28 February 2026

Industry: retail

Note 1 Accounting policies, judgements and estimates (extract 1)

Leases

The Group assesses whether a contract is, or contains, a lease at inception of the contract.

The Group as a lessee

A right of use asset and corresponding lease liability are recognised at commencement of the lease.

The lease liability is measured at the present value of the lease payments, discounted at the rate implicit in the lease, or if that cannot be readily determined, at the lessee’s incremental borrowing rate specific to the term, country, currency and start date of the lease.

The lease liability is subsequently measured at amortised cost using the effective interest rate method. It is remeasured, with a corresponding adjustment to the right of use asset, when there is a change in future lease payments resulting from a rent review, change in an index or rate such as inflation, or change in the Group’s assessment of whether it is reasonably certain to exercise a purchase, extension or break option.

The right of use asset is initially measured at cost, comprising: the initial lease liability; any lease payments already made less any lease incentives received; initial direct costs; and any dilapidation or restoration costs. The right of use asset is subsequently depreciated on a straight-line basis over the shorter of the lease term or the useful life of the underlying asset, and tested for impairment.

Leases of low value assets (value when new less than £5,000) and short-term leases of 12 months or less are expensed to the Group income statement, as are variable payments dependent on performance or usage not arising on a sale and leaseback transaction, ‘out of contract’ payments and non-lease service components.

The Group as a lessor

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership to the lessee. All other leases are classified as operating leases, for which rental income is recognised on a straight-line basis over the term of the lease.

Sale and leaseback

Where the Group sells an asset and immediately reacquires use of it by entering into a lease with the buyer, a lease liability is recognised, the associated property, plant and equipment asset is derecognised, and a right of use asset is recognised at the proportion of the carrying value relating to the right retained. Any gain or loss arising relates to the rights transferred to the buyer.

In the cash flow statement, sale and leaseback proceeds received are classified as investing cash flows, unless the proceeds exceed the fair value of the asset sold, in which case the excess proceeds are classified as financing cash flows.

Property buybacks

A property buyback is where a property that is currently leased is bought back from the landlord. Property buybacks that are a direct purchase of the underlying asset, outside of a corporate wrapper, are viewed as the modification of the lease to include a purchase option, followed by the immediate exercise of that purchase option. The lease liability is settled and the right of use asset forms part of the cost of the property, plant and equipment acquired, and no gain or loss is recognised in the income statement from the property buyback.

Property buybacks inside a corporate wrapper (such as a special purpose vehicle or joint venture structure) that do not meet the definition of a business combination are asset acquisitions. The cost of the asset acquisition includes the cash consideration paid and the carrying values of pre-existing lease contracts and any previously held interests. No gain or loss is recognised in the income statement from the property buyback.

In the cash flow statement, property buyback net proceeds paid are classified as investing cash flows, unless the proceeds exceed the incremental asset purchased (difference between property, plant and equipment recognised and right of use asset derecognised), in which case the excess proceeds are classified as financing cash flows.

Note 1 Accounting policies, judgements and estimates (extract 2)

Judgements and sources of estimation uncertainty (extract)

Critical accounting judgements (extract)

Leases

Management exercises judgement in determining the likelihood of exercising break or extension options in determining the lease term. Break and extension options are included to provide operational flexibility should the economic outlook for an asset be different to expectations, and hence at commencement of the lease, break or extension options are not typically considered reasonably certain to be exercised, unless there is a valid business reason otherwise.

The discount rate used to calculate the lease liability is the rate implicit in the lease, if it can be readily determined, or the lessee’s incremental borrowing rate if not. Management uses the rate implicit in the lease where the lessor is a related party (such as leases from joint ventures) and the lessee’s incremental borrowing rate for all other leases. Incremental borrowing rates are determined monthly and depend on the term, country, currency and start date of the lease. The incremental borrowing rate is determined based on a series of inputs including: the risk-free rate based on government bond rates; a country-specific risk adjustment; a credit risk adjustment based on Tesco bond yields; and an entity-specific adjustment where the entity risk profile is different to that of the Group.

Refer to Note 13 for additional disclosures relating to leases.

Note 13 Leases

Group as lessee

Lease liabilities represent rentals payable by the Group for certain retail, distribution and office properties and other assets such as motor vehicles. The leases have varying terms, purchase options, escalation clauses and renewal rights. Purchase options and renewal rights, where they occur, are at market value. Escalation clauses are in line with market practices and include inflation-linked, fixed rates, resets to market rents and hybrids of these.

Right of use assets

(a) Refer to Note 15.

(b) Other movements include lease terminations, modifications and reassessments, foreign exchange, reclassifications between asset classes and entering into finance subleases.

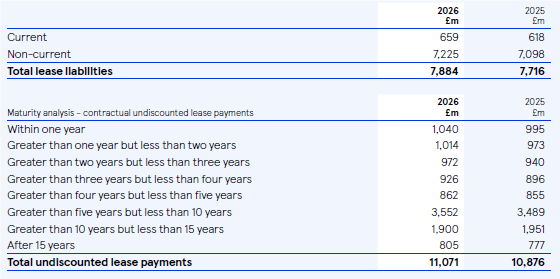

Lease liabilities The following tables show the discounted lease liabilities included in the Group balance sheet and a maturity analysis of the contractual undiscounted lease payments. A reconciliation of the Group’s opening to closing lease liabilities balance is presented in Note 31.

Amounts recognised in the Group income statement

* Interest expense on lease liabilities is presented gross of £14m hedging impact (2025: £7m).

Amounts recognised in the Group cash flow statement

Future possible cash outflows not included in the lease liability

Some leases contain break clauses or extension options to provide operational flexibility. Potential future undiscounted lease payments not included in the reasonably certain lease term, and hence not included in lease liabilities, total £14.7bn.

Future increases or decreases in rentals linked to an index or rate (not arising on a sale and leaseback transaction) are not included in the lease liability until the change in cash flows takes effect. Approximately 76% (2025: 76%) of the Group’s lease liabilities are subject to inflation-linked rentals, of which 91% (2025: 89%) have inflation caps, with a weighted average cap of 4.3% (2025: 4.3%). Of the inflation-linked leases with caps, 31% (2025: 33%) of the lease liability value was hedged through index-linked swaps. A further 17% (2025: 17%) of all leases are subject to rent reviews. Rental changes linked to inflation or rent reviews typically occur on an annual or five-yearly basis. Refer to Note 26.

The Group is committed to payments totalling £535m (2025: £125m) in relation to leases that have been signed but have not yet commenced.

Group as lessor

The Group leases out owned properties and sublets leased properties under operating and finance leases. Such properties include malls, mall units, stores, units within stores, distribution centres and residential properties.

Amounts recognised in the Group income statement

(a) Comprises sublease interest income.

(b) Includes £31m (2025: £28m) of sublease rental income.

Finance lease payments receivable

The finance lease receivable (net investment in the lease) included in the Group balance sheet is £27m (2025: £23m).

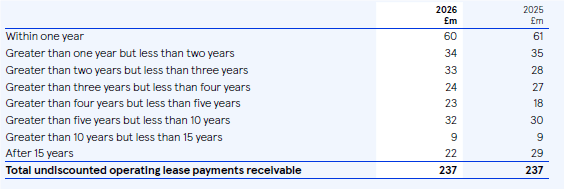

Operating lease payments receivable maturity analysis

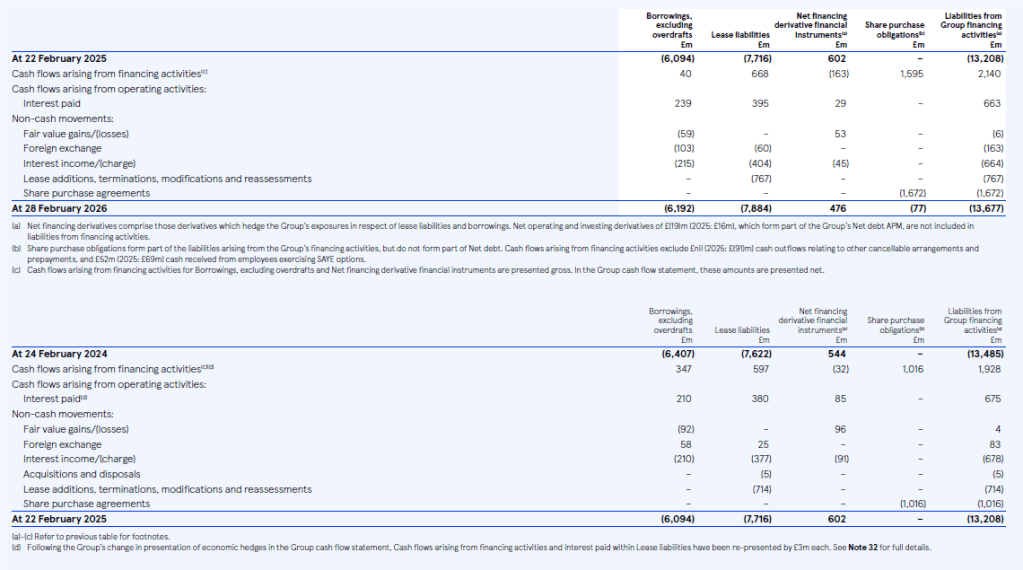

Note 31 Analysis of changes in net debt (extract)

The tables below set out the movements in liabilities from financing activities: