Hunting PLC – Annual report – 31 December 2016

Industry: oil and gas

- Post-Employment Benefits

(a) UK Pensions

Within the UK, the Group operates a funded pension scheme, which includes a defined benefit section with benefits linked to price inflation and a defined contribution section with benefits dependent on future investment returns. The defined benefit section closed to future accrual on 30 June 2016 and existing contributing members of that section joined the defined contribution section with effect from 1 July 2016. The majority of UK employees are members of the defined contribution section of the scheme.

The UK scheme is registered with HMRC for tax purposes, is operated separately from the Group and is managed by a board of trustees. The trustees are responsible for the payment of benefits and the management of the scheme’s assets.

The UK scheme is subject to UK regulations, which require the Group and the trustees to agree a funding strategy and contributions schedule for the defined benefit section of the UK scheme. Contributions due to the defined contribution section of the UK scheme and other Group defined contribution arrangements are charged directly to profit and loss.

Risk exposures and investment strategy

The scheme is managed so that it is well funded and represents a low risk to the Group. In particular, the scheme’s assets are invested in a range of deferred annuity and immediate annuity policies with a number of insurers, which largely match the benefits to be paid to members of the scheme. This strategy significantly reduces the Group’s investment, inflation and demographic risks in relation to the scheme’s liabilities. The position would change materially if one of the insurers was no longer able to meet its obligations as the pension obligation ultimately rests with the Group.

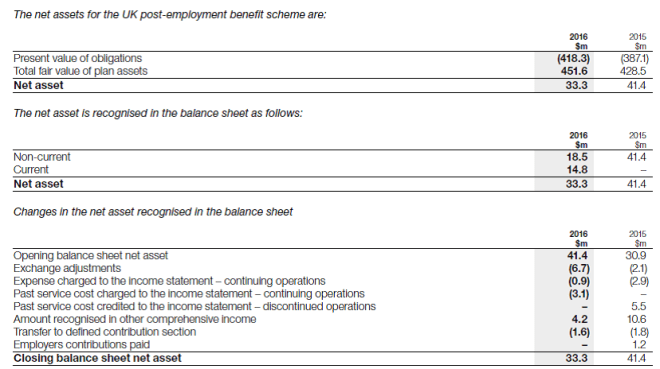

The decrease in the Group’s pension asset seen over 2016 principally reflects the agreement of the trustees and the Group to meet the contributions of the defined contribution section from the surplus in the scheme and the loss as a result of the closure of the defined benefit section, partially offset by the gain arising from the trustees’ decision to surrender part of one of their insurance annuity policies.

Funding strategy

The trustees and the Group together agree a funding strategy for the UK scheme every three years. As the defined benefit section is closed to future accrual and the benefits earned by the members are covered in full by annuity policies, the Group does not expect to pay any further contributions into the defined benefit section of the scheme. The trustees and the Group have also agreed that contributions to the defined contribution section can be met from the excess assets in the scheme for the time being and that a repayment of £12.0m ($14.8m) net of tax of £4.2m ($5.2m) from the scheme to the Group has been made on 24 February 2017.

The Group has concluded that it can recognise the full amount of the surplus on the grounds that it could gain sufficient economic benefit from a future reduction of its contributions to the defined contribution section of the scheme or through a future refund from the scheme. This is happening in practice as contributions to the defined contribution section are already being met from the scheme’s excess assets and a repayment to the Group has been agreed for 2017. Amendments to the current accounting rules on recognising a surplus (IFRIC 14 The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction) are currently being considered. The Group has concluded that the above accounting treatment will not be affected by the current proposed changes to these rules.

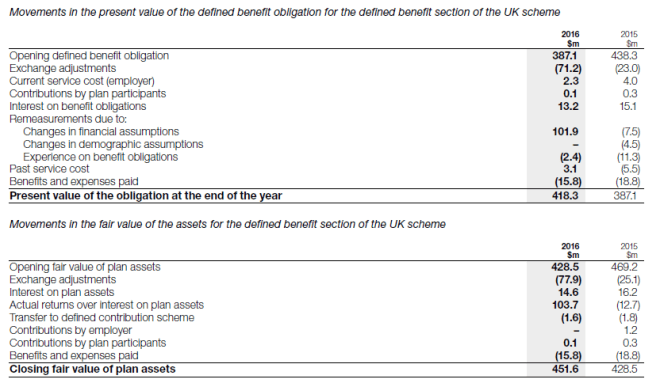

The “Actual returns over interest on plan assets” shown in the table above principally includes the impact of both a gain arising from the surrender of some of the annuity policies (about $3.1m) and from changes in the financial assumptions used to value the insurance annuity policies (about $100.6m) after allowing for membership experience. The gain due to the changes in the assumptions broadly offsets the corresponding loss on the remeasurement of the defined benefit obligation, demonstrating that the pensions related risks have largely been mitigated by the scheme’s investment strategy.

The fair value of the insurance annuity policies has been calculated using the same financial and demographic assumptions as those used to value the corresponding obligations. The scheme does not invest in property occupied by the Group or in financial securities issued by the Group.

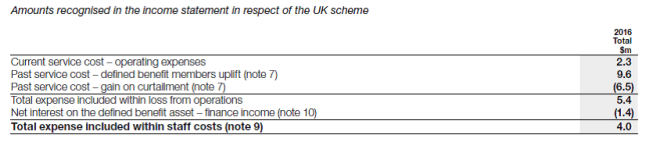

The current service cost includes $1.5m (2015 – $1.2m) of administration costs.

In addition, employer contributions of $6.7m (2015 – $8.3m) for various Group defined contribution arrangements (including the defined contribution section of the UK scheme) are recognised in the income statement.

Special events

As part of the closure of the defined benefit section, existing contributing members of that section were given a one-off uplift to their pensions. The net effect of the closure and these uplifts has been recognised in the income statement.

A repayment from the scheme to the Group of excess assets of £7.8m net of tax (approximately $9.6m) has been agreed for 2017. The impact of this repayment will be reflected in the 2017 financial statements. It has also been agreed that the defined benefit section of the scheme will be wound up, with the insurance annuity policies transferred into the names of the individual members.

The principal assumptions used for accounting purposes reflect prevailing market conditions are:

The assumptions used to determine the end-of-year benefit obligations are also used to calculate the following year’s cost.

Sensitivity analysis

The weighted average duration to payment of the projected future cash flows from the defined benefit section of the scheme is about 17 years. As the defined benefit section is closed to future accrual and members’ benefits are covered in full by annuity policies, any change in the obligation arising as a result of changes in the above assumptions is broadly matched by a corresponding change in the value of the insurance policies, so that the impact on the net balance sheet asset is significantly dampened.

The net balance sheet is therefore only largely sensitive to changes in the market value of the invested assets. The investment strategy for the defined benefit section, with all funds in either annuity policies or cash, should mean the surplus figure is stable.

(b) Other Pensions

The Group also operates a cash balance arrangement in the US for certain executives. Members build up benefits in this arrangement by way of notional contributions and notional investment returns. Actual contributions are paid into an entirely separate investment vehicle held by the Company, which is used to pay benefits due from the cash balance arrangement when the member retires.

Under IAS 19, the cash balance arrangement is accounted for as an unfunded defined benefit scheme, although in practice it operates like a defined contribution arrangement with the obligations matched by the assets in the separate investment vehicle.

The amounts recognised in the income statement during the year were $0.1m (2015 – $0.2m) for the employer’s current service cost (recognised in operating expenses) and $0.3m (2015 – $0.3m) interest cost (recognised in finance expense).

- Amortisation and Exceptional Items (extract)

On 11 March 2016, it was agreed that the defined benefit pension section of the Group’s UK pension scheme would be closed to future accrual of further benefits from 30 June 2016. The active members have been offered membership of the defined contribution section of the scheme from 1 July 2016. The effect of this change has been recognised in the 2016 financial statements, resulting in a gain on the curtailment of future defined benefit scheme accruals of $6.5m and a past service cost of $9.6m on defined benefit members’ uplift on 11 March 2016, the net charge being $3.1m.