Equinor ASA – Annual report – 31 December 2025

Industry: oil and gas

Note 25. Leases

Accounting policies

Leases

A lease is defined as a contract that conveys the right to control the use of an identified asset for a period of time in exchange for consideration. At the date at which the underlying asset is made available for Equinor, the present value of future lease payments (including extension options considered reasonably certain to be exercised) is recognised as a lease liability. The present value is calculated using Equinor’s incremental borrowing rate. A corresponding right-of-use (RoU) asset is recognised, including lease payments and direct costs incurred at the commencement date. Lease payments are reflected as interest expense and a reduction of lease liabilities. The RoU assets are depreciated on a systematic basis, over the shorter of each contract’s term and the assets’ useful life, and in line with Equinor’s policy for depreciation of similar or other relevant underlying assets.

Short-term leases (12 months or less) and leases of low-value assets are expensed or (if appropriate) capitalised as incurred, depending on the activity in which the leased asset is used.

Many of Equinor’s lease contracts, such as rig and vessel leases, involve several additional services and components, including personnel cost, maintenance, drilling related activities, and other items. For a number of these contracts, the additional services represent a not inconsiderable portion of the total contract value. Non-lease components within lease contracts are accounted for separately for all underlying classes of assets and reflected in the relevant expense category or (if appropriate) capitalised as incurred, depending on the activity involved.

Accounting judgement regarding leases

In the oil and gas industry, where activity frequently is carried out through joint arrangements or similar arrangements, the application of IFRS 16 Leases requires evaluations of whether the joint arrangement or its operator is the lessee in each lease agreement and consequently whether such contracts should be reflected gross (100%) in the operator’s financial statements, or according to each joint operation partner’s proportionate share of the lease.

In many cases where an operator is the sole signatory to a lease contract of an asset to be used in the activities of a specific joint operation, the operator does so implicitly or explicitly on behalf of the joint arrangement. In certain jurisdictions, and importantly for Equinor as this includes the Norwegian continental shelf (NCS), the concessions granted by the authorities establish both a right and an obligation for the operator to enter into necessary agreements in the name of the joint operations (licences).

As is the customary norm in upstream activities operated through joint arrangements, the operator will manage the lease, pay the lessor, and subsequently re-bill the partners for their share of the lease costs.

In each such instance, it is necessary to determine whether the operator is the sole lessee in the external lease arrangement, and if so, whether the billings to partners may represent sub-leases, or whether it is in fact the joint arrangement which is the lessee, with each participant accounting for its proportionate share of the lease. Where all partners in a licence are considered to share the primary responsibility for lease payments under a contract, Equinor’s proportionate share of the related lease liability and RoU asset will be recognised net by Equinor. When Equinor is considered to have the primary responsibility for the full external lease payments, the lease liability is recognised gross (100%).

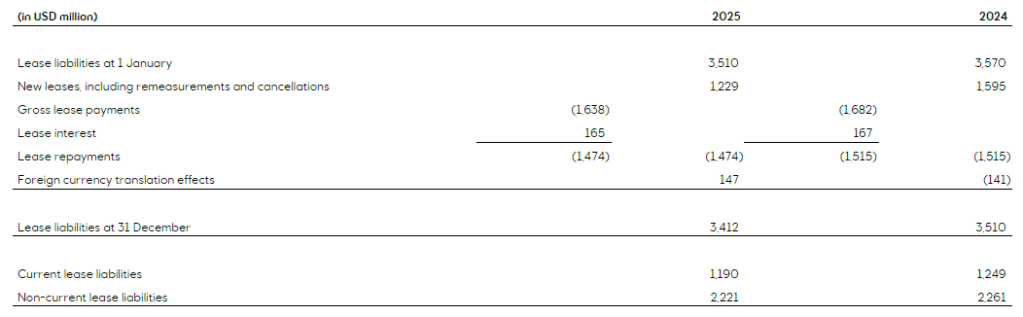

Equinor leases certain assets, notably drilling rigs, transportation vessels, storages and office facilities for operational activities. Equinor has the primary responsibility for the full external lease payments in the majority of the lease contracts, and the use of leases serves operational purposes rather than as a tool for financing.

Equinor recognised revenues of USD 294 million in 2025 and USD 269 million in 2024 related to lease costs recovered from licence partners related to lease contracts being recognised gross by Equinor.

Commitments relating to lease contracts which had not yet commenced at year-end are included within note 26 Other commitments, contingent liabilities and contingent assets.

A maturity profile based on undiscounted contractual cash flows for lease liabilities is disclosed in note 4 Financial risk and capital management.

Information related to lease payments and lease liabilities

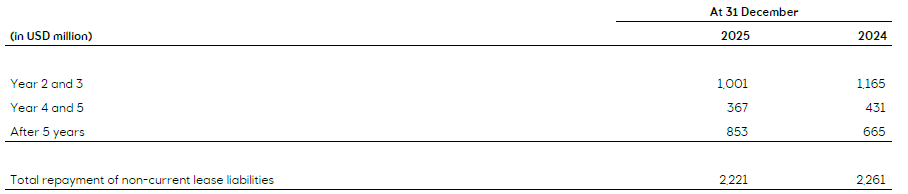

Non-current lease liabilities maturity profile

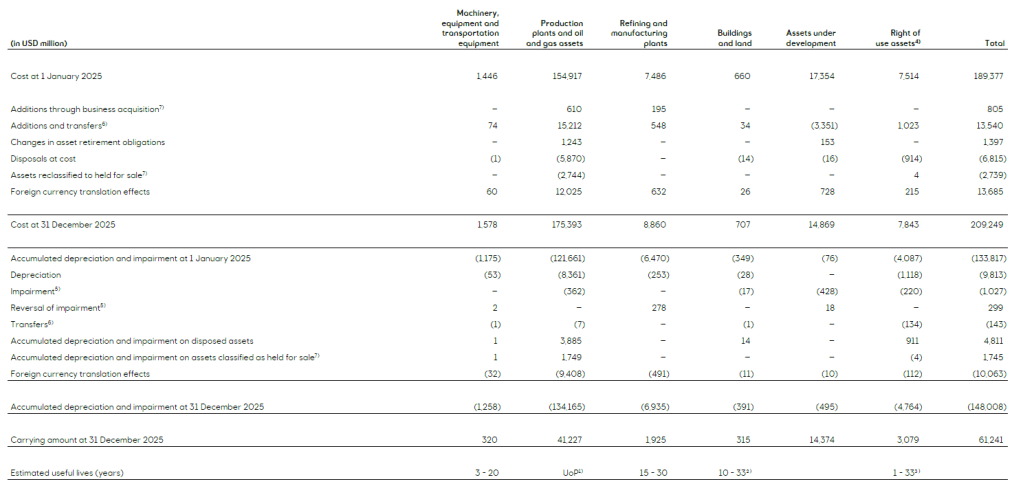

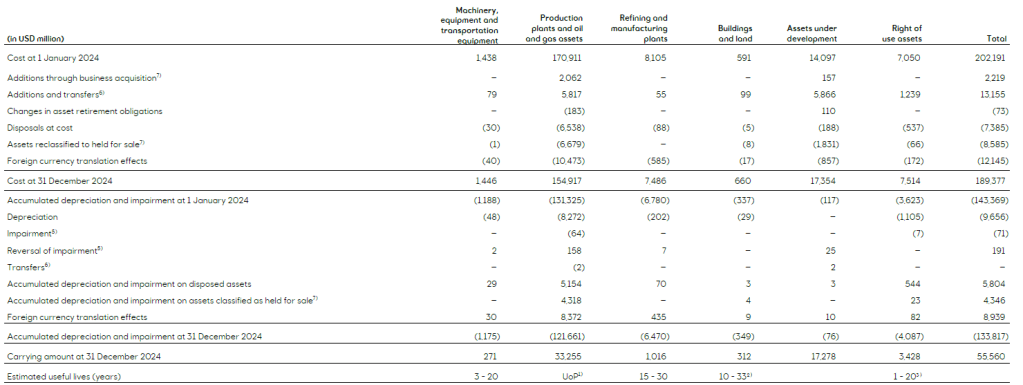

The Right of use assets are included within the line item Property, plant and equipment in the Consolidated balance sheet. See also note 12 Property, plant and equipment.

Note 12. Property, plant and equipment (extract)

1) Depreciation according to unit of production method.

2) Land is not depreciated. Buildings include leasehold improvements.

3) For depreciation method, see note 25 Leases.

4) Right of use assets at 31 December 2025 mainly consist of Land and buildings USD 1,083 million, Vessels USD 1,170 million and Drilling rigs USD 458 million.

5) See note 14 Impairments.

6) The carrying amount of assets transferred to Property plant and equipment from Intangible assets in 2025 and 2024 amounted to USD 230 million and USD 240 million, respectively.

7) For additions through business acquisition and assets reclassified to held for sale, see note 6 Acquisitions and disposals.

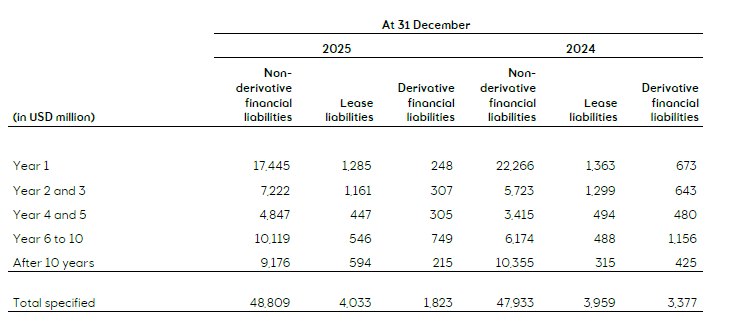

Note 4. Financial risk and capital management (extract)

The table below shows a maturity profile, based on undiscounted contractual cash flows, for Equinor’s financial liabilities.

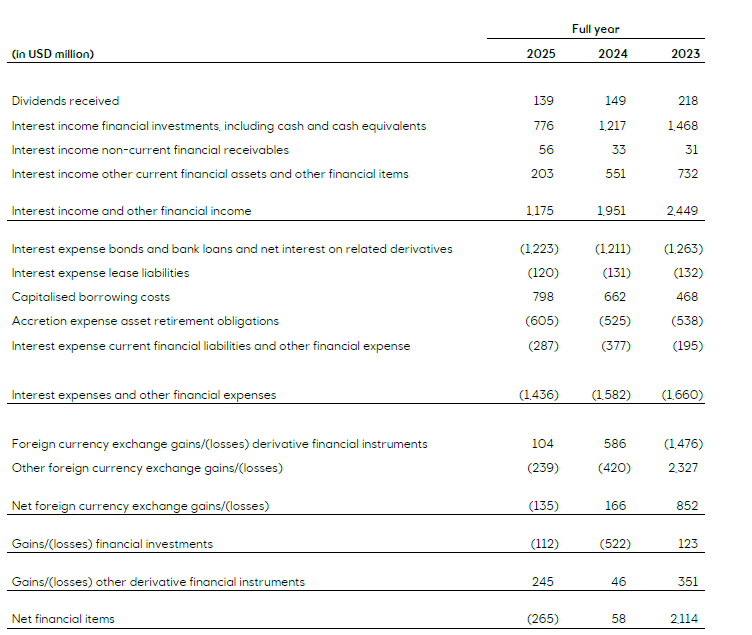

Note 10. Financial items (extract)

Note 26. Other commitments, contingent liabilities and contingent assets (extract)

Lease commitments

Equinor has entered into lease commitments for which the lease had not commenced as of year-end. These agreements include future leases for vessels, drilling rigs and other assets for operational activities. Total nominal minimum lease commitments for leases not yet commenced amounted to USD 2,118 million as of 31 December 2025. For commenced leases, please refer to note 25 Leases.