ČEZ, a. s. – Annual report – 31 December 2025

Industry: utilities

15. Provisions (extract 1)

The Group creates provisions when it has a present legal or constructive obligation as a result of a past event, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and the amount can be reliably estimated.

Nuclear Provisions, Provisions for Mine Reclamation and Mining Damages, Waste Storage Reclamation and Demolition and Dismantling of Fossil-fuel Power Plants

The provision recognized represents the best estimate of the expenditures required to settle the present obligation at the current balance sheet date. Such estimate, expressed at the price level at the date of estimate, is discounted using an estimated long-term risk-free real interest rate to take into account the timing of payments. While estimating future expenses, an associated risk related to these future expenses is taken into account. This risk adjustment can be expressed as a reduction of the used discount rate. The initial discounted cost amounts are capitalized as part of property, plant and equipment and are depreciated over the lives of property, plant and equipment or over a time for which power plants will generate electricity in case of nuclear provisions and provisions for demolition and dismantling of emission sources. In case of provisions for remediation, reclamation and mining damages over the period of ongoing mining or over the expected remaining active operating life of the landfill in the case of landfill reclamation provisions, if this period is shorter than the useful life of the power plant.

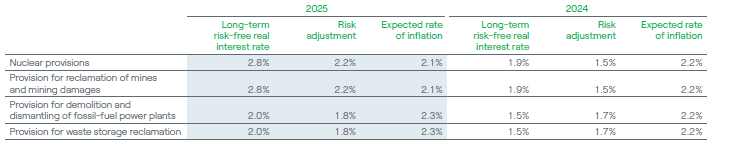

The overview of interest rates used for calculation of provisions as of December 31, 2025 and 2024:

Each year, the provisions are increased to reflect the accretion of discount and to accrue an estimate for the effects of inflation. These expenses are recognized in the statement of income in the line item Interest on provisions.

Changes in a decommissioning liability that result from a change in the current best estimate of timing and/or amount of cash flows required to settle the obligation or from a change in the discount rate are added to (or deducted from) the amount recognized as the related asset. However, to the extent that such a treatment would result in a negative asset, the effect of the change is recognized directly in profit or loss.

Although the Group made its best estimate of the amount of provisions, the actual costs could vary substantially from the above estimates because of new regulatory requirements, changes in technology, increased costs of labor, materials and equipment and/or the actual time required to complete all decommissioning, disposal and storage activities.

15. Provisions (extract 2)

15.1. Nuclear Provisions

The Group makes a provision for nuclear decommissioning, a provision for interim storage of spent nuclear fuel and other radioactive waste, and a provision for the funding of subsequent permanent disposal of spent nuclear fuel and irradiated reactor components.

The Company operates two nuclear power plants. The Dukovany Nuclear Power Plant comprises four units commissioned for continuous operation between 1985 and 1987. The Temelín Nuclear Power Plant consists of two units that were commissioned for continuous operation in 2002 and 2003. The Nuclear Energy Act sets down obligations for nuclear facility decommissioning and disposal of radioactive waste and spent nuclear fuel. In accordance with the Nuclear Energy Act, all the nuclear parts and equipment of a nuclear power plant must be disposed of after the end of operation. For the purpose of determining the amount of nuclear provisions, it is estimated that the Dukovany Nuclear Power Plant will stop generating electricity in 2047, the Temelín Nuclear Power Plant in 2062. The decommissioning of nuclear power plants is expected to continue for approximately 45 years after electricity generating would end. Decommissioning cost studies for the Dukovany Nuclear Power Plant from 2022 and for Temelín Nuclear Power Plant from 2023 assume that the total costs of decommissioning of so-called nuclear island and conventional part of these power plants will reach the amount of CZK 45.3 billion and CZK 36.9 billion, respectively. The Company makes contributions to restricted bank accounts in the amount of the nuclear provisions recorded under the Nuclear Energy Act. These funds can be invested in government bonds in accordance with legislation. These restricted financial assets are reported in the balance sheet as part of the line item Restricted financial assets (see Note 7.1).

It is assumed that a permanent repository for the storage of spent nuclear fuel and irradiated reactor components will be ready for operation in 2050. A disposing of stored spent nuclear fuel at the repository will continue until approximately 2090.

The Ministry of Industry and Trade established the Radioactive Waste Repository Authority (SÚRAO) as the central organizer and operator of facilities for the final disposal of radioactive waste and spent fuel. The SÚRAO operates, supervises and is responsible for disposal facilities and for disposal of radioactive waste and spent fuel therein. The activities of the SÚRAO are financed through a nuclear account funded by the originators of radioactive waste. Contribution to the nuclear account up to December 31, 2025, is stated by Nuclear Energy Act at CZK 55 per MWh produced at nuclear power plants. Starting in 2026, the Nuclear Energy Act only sets the maximum amount of this fee. Its specific amount is determined by government regulation, always for a five-year period. Between 2026 and 2030, the contribution is CZK 88 per MWh produced at nuclear power plants. In 2025 and 2024, the payments to the nuclear account amounted to CZK 1,764 million and CZK 1,633 million, respectively. The originator of radioactive waste and spent fuel directly covers all costs associated with interim storage of radioactive waste and spent fuel.

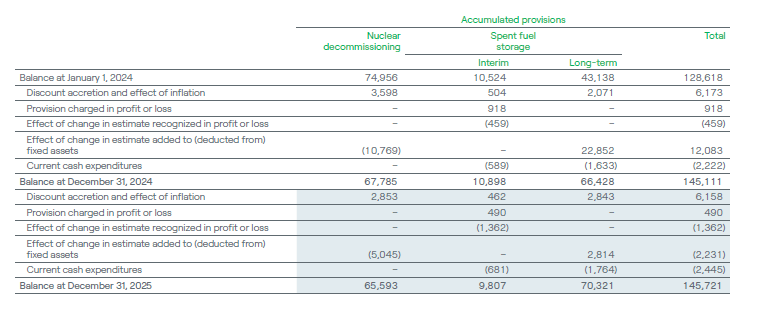

The overview of the provisions for the years ended December 31, 2025 and 2024 (in CZK millions):

The use of the provision for permanent disposal of spent nuclear fuel in the current year comprises payments made to the government-controlled nuclear account and the use of the provision for interim storage represents, in particular, purchases of containers for spent nuclear fuel and other related equipment for these purposes.

In 2025, the Company recorded the change in estimated provision for interim storage of spent nuclear fuel. The change relates to the change in discount rate. The change in estimated provision for nuclear decommissioning is due to the change in the amount of costs for decommissioning of Dukovany Nuclear Power Plant and Temelín Nuclear Power Plant and due to the change in discount rate. The change in estimated provision for long-term spent fuel storage is connected with the modification of the expected output of the nuclear power plants, change of expected contribution to the nuclear account per MWh in future years and change in discount rate.

In 2024, the Company recorded the change in estimated provision for interim storage of spent nuclear fuel. The change relates to the change in expected future storage costs and change in discount rate. The change in estimated provision for nuclear decommissioning is due to the change in the amount of costs for decommissioning of Dukovany Nuclear Power Plant and Temelín Nuclear Power Plant and due to the change in discount rate. The change in estimated provision for long-term spent fuel storage is connected with the modification of the expected output of the nuclear power plants, change of expected contribution to the nuclear account per MWh in future years and change in discount rate.

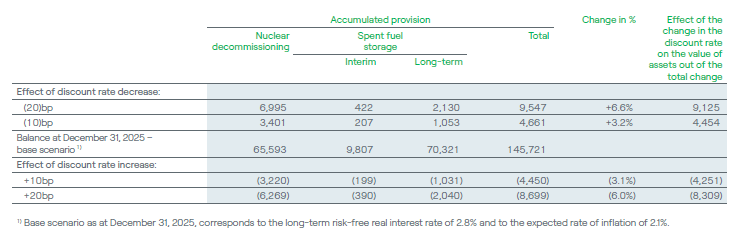

The following table shows the sensitivity of nuclear provisions to changes in the discount rate, keeping all other parameters unchanged, as at December 31, 2025 (in CZK millions):

15.2. Provisions for Mine Reclamation and Mining Damages, Waste Storage Reclamation and Demolition and Dismantling of Fossil-fuel Power Plants

The Group has recognized a provision for demolition and dismantling of fossil-fuel power plants after their decommissioning.

The Group creates a provision for waste storage reclamation in order to ensure reclamation and subsequent care of the waste storage after its operation has ended. Its amount is estimated on the basis of the expenditures which would be most likely required for the land reclamation. The Group makes contributions to restricted bank accounts in the amount of the provisions recorded under the Waste Act. These funds can be invested in government bonds in accordance with legislation. These restricted financial assets are reported in the balance sheet as part of the line item Restricted financial assets (see Note 7.1).

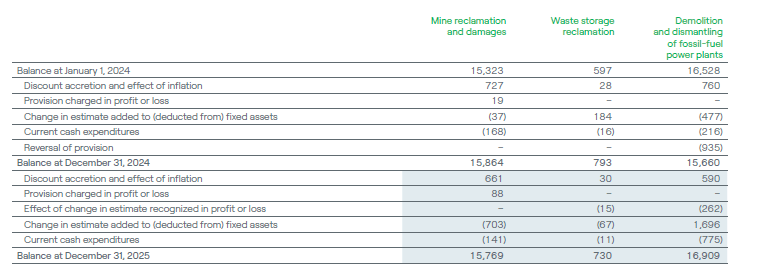

The following table shows the movements of provisions for the years ended December 31, 2025 and 2024 (in CZK millions):

The provision for decommissioning and reclamation of mines and the provision for mining damages were recorded by Severočeské doly a.s., a mining subsidiary of ČEZ. Severočeské doly a.s. operates open pit coal mines and is responsible for decommissioning and reclamation of the mines as well as for damages caused by the operations of the mines. Current cash expenditures represent cash payments for current reclamation of mining area and settlement of mining damages. The use of the provision for decommissioning and reclamation of mines is not so intense during the period, when the mining is in progress (the cease of mining is expected in 2030). The highest use of the provision is expected during years 2031–2040 (CZK 11.5 billion in present value) in relation to solution of the residual pits. Mine reclamation should be finalized in 2045, during years 2041–2045 is expected the use of provision of CZK 1.6 billion in present value. This expected future time course of using the provision is uncertain and corresponds to the current strategy of the Group. Changes in estimate in 2025 and 2024 represent change in provision as result of updated cost estimates in the current period, mainly due to changes in expected prices of reclamation activities, and also due to changes in their timing and in the discount rate.

The use of the provision for demolition and dismantling of fossil-fuel power plants in 2025 was related especially to Ledvice power plant. For the next years, the use of provision is expected mainly in 2029–2030 for power plant Dětmarovice (CZK 2.6 billion in present value), in 2031–2034 for remaining coal-fired power plants (CZK 11.0 billion in present value) and in 2047–2048 for combined-cycle gas turbine in Počerady (CZK 0.6 billion in present value). This expected future time course of using the provision may change. In 2025 and 2024, the Group recorded the change in estimate in provision for demolition and dismantling of fossil-fuel power plants due to the update of the amount and timing of the decommissioning costs and due to change in discount rate.

4. Property, Plant and Equipment (extract 1)

Property, plant and equipment are measured at cost less accumulated depreciation and impairments. The cost of property, plant and equipment comprises the purchase price and the related cost of materials and labor and the cost of debt financing used in the construction. The cost also includes the estimated cost of dismantling and removing a tangible asset to the extent specified by IAS 37, Provisions, Contingent Liabilities, and Contingent Assets. Government grants and similar subsidies received for the acquisition of property, plant and equipment decrease the cost.

4. Property, Plant and Equipment (extract 2)

Nuclear Fuel

The Group recognizes nuclear fuel as part of property, plant and equipment because the period for which it is used for electricity generation exceeds 1 year. Nuclear fuel is measured at cost less accumulated depreciation and, if applicable, impairments. Nuclear fuel includes a capitalized portion of the provision for interim storage of spent nuclear fuel. The depreciation of nuclear fuel in a reactor is determined on the basis of the amount of energy generated and presented in the statement of income in the line item Fuel and emission rights (see Note 21). The depreciation of nuclear fuel includes additions to the provision for interim storage of spent nuclear fuel (see Note 15).

2.3. Estimates and Accounting Judgments (extract)

In applying accounting policies, the Group makes judgments (other than judgments requiring estimates) that have a significant effect on the amounts reported in the consolidated financial statements, and further makes estimates and assumptions in determining the carrying amounts of assets and liabilities when an adequate value for such estimates or assumptions is not readily available from other sources. These estimates and related assumptions are based on historical experience and other factors that are considered to be relevant. The Group makes significant estimates when determining the recoverable amounts of property, plant and equipment and intangible assets (see Note 6), accounting for the nuclear provisions (see Note 15.1), provisions for reclamation of mines, mining damages and waste storage reclamation (see Note 15.2), provision for demolition and dismantling of fossil-fuel power plants (see Note 15.2), unbilled electricity and gas (see Note 12), fair value of commodity contracts and non-commodity derivatives (see Note 8), incremental borrowing rate and lease terms to measure lease liabilities (see Note 17) and deferred tax calculation (see Note 28). Actual outcome may vary from these estimates. Estimates and their underlying assumptions are reviewed on an ongoing basis using available data, including macroeconomic data. Changes in these accounting estimates are recognized in the period in which the accounting estimate is revised. A change in estimate may affect the profit or loss of the current or future periods.

The most significant changes in estimates in 2025 related to the provision for nuclear decommissioning due to the change of the discount rate and further related to the provision for long-term spent fuel storage due to the expected adjustment of generation in nuclear power plants, due to the change of expected contribution to the nuclear account depending on electricity generated in nuclear power plants and to the change of the discount rate and provision for nuclear decommissioning and due to the change of the discount rate.

The most significant changes in estimates in 2024 related to the provision for long-term spent fuel storage due to the increase of expected contribution to the nuclear account depending on electricity generated in nuclear power plants and to the change of the discount rate and provision for nuclear decommissioning due to the change of the discount rate.

Another significant change in estimates in 2024 related to adjustment of depreciations and depreciating methods of certain asset classes. Regarding the effects of decarbonization and the assumptions of further market development, the Group reassessed depreciation methods. The result is a change in the accounting estimate for the depreciation method for coal generation resources 1) and for assets used in lignite mining (collectively “coal assets”). Up to September 30, 2024, coal assets were depreciated on a linear basis over the expected remaining useful life. From October 1, 2024, the Group depreciates coal assets using a method in which depreciation decreases evenly over the remaining useful life (the so-called sum-of-years’ digits method).

The depreciable amount of the Group’s coal assets was CZK 73.2 billion as at September 30, 2024. The following table shows the depreciation schedule as a percentage of the depreciable amount as at September 30, 2024, after the change in the depreciation method until 2030, which represents the currently expected end of operation of the coal assets:

Compared to the linear method of depreciation previously used, there was therefore a significant change in the distribution of depreciation over time. With regard to the different effective income tax rate in individual years, which is affected by the windfall tax until December 31, 2025, there was an increase of deferred tax liability as at September 30, 2024, in the amount of CZK 4,885 million. The related deferred income tax expense was reported as a one-off item in the line item Income tax in the statement of income as at September 30, 2024.

1.1. Strategy of the Company in the Context of Climate Changes

The “VISION 2030 – Clean Energy of Tomorrow” strategy is focused on dynamic transformation of the generation portfolio to low-emission one, responsible and sustainable business, the fulfillment of the growth strategy while maintaining the set level of debt and achievement of full climate neutrality by 2040. The strategy includes a commitment to fundamentally limit the generation of heat and electricity from coal by 2030. In areas of distribution and sales, the basic goal is to provide the most advantageous energy solutions and the best customer experience on the market. The goal to develop CEZ Group responsibly and sustainably in accordance with ESG principles is also part of the strategy.

The impacts of climate changes, but also a number of other factors, are evaluated in the various estimates and accounting judgments that the preparation of financial statements according to IFRS requires (see Note 2.3). Mainly it relates to determination of recoverable amount of property, plant and equipment and intangible assets (Note 6), of the provision for mine reclamation and mining damages (Note 15.2), of the provision for demolition and dismantling of fossil-fuel power plants (Note 15.2) and of remaining useful life and depreciation methods of property, plant and equipment used for depreciation (Note 4).

7.1. Restricted Financial Assets

The overview of restricted financial assets at December 31, 2025 and 2024, is as follows (in CZK millions):

The Czech government bonds are measured at fair value through other comprehensive income.