MTN Group Limited – Annual report – 31 December 2024

Industry: telecoms

1 ACCOUNTING FRAMEWORK AND CRITICAL JUDGEMENTS (extract)

1.1 Basis of preparation

The consolidated financial statements of MTN Group Limited (the Company) comprise the Company and its subsidiaries and the Group’s interest in associates and joint ventures and controlled structured entities (together referred to as the Group and individually as Group entities).

The consolidated financial statements and Company financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS Accounting Standards) as issued by the International Accounting Standards Board (IASB) and Interpretations as issued by the IFRS Interpretations Committee (IFRIC), and comply with the South African Institute of Chartered Accountants (SAICA) Financial Reporting Guides as issued by the Accounting Practices Committee (APC), Financial Reporting Pronouncements as issued by the Financial Reporting Standards Council (FRSC), the Johannesburg Stock Exchange (JSE) Listings Requirements and the requirements of the South African Companies Act, No 71 of 2008, as amended (Companies Act).

The Group and the Company have considered all new accounting pronouncements and interpretations that became effective in the current reporting period. These had no material impact on the Group’s or Company’s financial statements except for Supplier Finance Arrangements – Amendments to IAS 7 and IFRS 7 resulting in additional disclosure. Refer to note 4.5 and 6.1.

The financial statements have been prepared on the historical cost basis adjusted for the effects of inflation where entities operate in hyperinflationary economies and for certain financial instruments that have been measured at fair value, where applicable.

Amounts are rounded to the nearest million with the exception of earnings per share and the related number of shares (note 2.5), number of ordinary shares (note 8.1), share-based payments (note 8.4) and directors’ emoluments and interests (note 10.2).

The preparation of financial statements in conformity with IFRS Accounting Standards requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Information about significant areas of estimation uncertainty and critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements are included in note 1.5.

1.3.2 Foreign currency

Functional and presentation currency

Items included in the financial statements of each entity in the Group are measured using the entity’s functional currency. The Group financial statements are presented in South African rand, which is the functional and presentation currency of the Company.

Transactions and balances

Foreign currency transactions are translated into the functional currency using the exchange rates at the dates of the transactions. Foreign exchange gains or losses resulting from the settlement of such transactions and from the translation at reporting date exchange rates of monetary assets and liabilities denominated in foreign currencies are recognised in profit or loss.

Translation of foreign operations

The results, cash flows and financial position of Group entities which are not accounted for as entities operating in hyperinflationary economies and that have a functional currency different from the presentation currency of the Group are translated into the presentation currency as follows:

- Assets and liabilities, including goodwill and fair value adjustments arising on acquisition, are translated at rates of exchange ruling at the reporting date.

- Specific transactions in equity are translated at rates of exchange ruling at the transaction dates.

- Income and expenditure and cash flow items are translated at weighted average exchange rates for the period or translated at exchange rates at the date of the transaction, where applicable.

- Foreign exchange translation differences are recognised in OCI and accumulated in the foreign currency translation reserve (FCTR), except to the extent the difference is allocated to non-controlling interests.

The results, cash flows and financial position of the Group entities, which are accounted for as entities operating in hyperinflationary economies and that have functional currencies different from the presentation currency of the Group are translated into the presentation currency of its immediate parent at rates of exchange ruling at the reporting date. As the presentation currency of the Group is that of a non-hyperinflationary economy, comparative amounts are not adjusted for changes in the price level or exchange rates in the current financial year.

An entity may have a monetary item that is receivable from a foreign operation. An item for which settlement is neither planned nor likely to occur in the foreseeable future is, in substance, a part of the entity’s net investment in that foreign operation. On consolidation, exchange differences arising from the translation of the net investment in foreign operations are taken to OCI and accumulated in the FCTR.

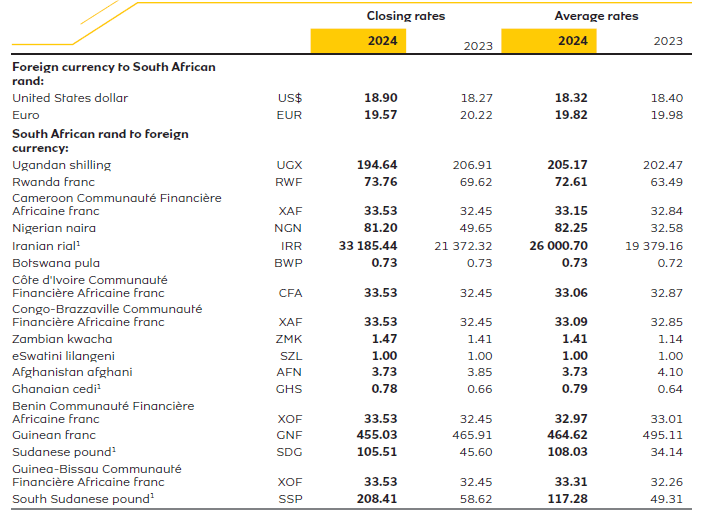

The exchange rates relevant to the Group are disclosed in note 7.6. For more details on judgements applied in the selection of exchange rates in countries operating in dual exchange rate economies, please refer to note 1.5.3.

Disposal of foreign operations

On disposal of a foreign operation, all exchange differences accumulated in equity in respect of that operation attributable to the equity holders of the Group are reclassified to profit or loss. The amount of FCTR reclassified to profit or loss is calculated based on the appreciation or devaluation in the functional currency of the foreign operation disposed against the functional currency of the Company. As the Group’s functional and presentation currency is South African rand and the FCTR is based on the appreciation or devaluation of the South African rand against the equity of the underlying operations in the Group, the Group uses the direct method to recycle the FCTR.

Exchange differences accumulated in equity in respect of a monetary item that is part of the Group’s net investment in a foreign operation, are not reclassified to profit or loss on settlement of the monetary item.

In the case of a partial disposal that does not result in the Group losing control over a subsidiary that includes a foreign operation, the proportionate share of accumulated exchange differences is reattributed to non-controlling interests and is not recognised in profit or loss. For all other partial disposals, the accumulated exchange differences are reclassified to profit or loss.

1.3.3 Hyperinflation

The financial statements (including comparative amounts) of the Group entities whose functional currencies are the currencies of hyperinflationary economies are adjusted in terms of the measuring unit current at the end of the reporting period.

As the presentation currency of the Group or the Company is that of a non-hyperinflationary economy, comparative amounts are not adjusted for changes in the price level in the current year. Differences between these comparative amounts and current year hyperinflation adjusted equity balances are recognised in OCI.

The carrying amounts of non-monetary assets and liabilities are adjusted to reflect the change in the general price index from the date of acquisition to the end of the reporting period. An impairment loss is recognised in profit or loss if the restated amount of a non-monetary item exceeds its estimated recoverable amount. On initial application of hyperinflation prior period gains and losses are recognised directly in equity.

Gains or losses on the net monetary position are recognised in profit or loss.

All items recognised in the income statement are restated by applying the change in the general price index from the dates when the items of income and expenses were initially earned or incurred.

At the beginning of the first period of application, the components of equity, except retained earnings, are restated by applying a general price index from the date the components were contributed or otherwise arose. These restatements are recognised directly in equity as an adjustment to opening retained earnings. Restated retained earnings are derived from all other amounts in the restated statement of financial position. If on initial application of hyperinflation accounting the restated value of the non-monetary assets exceed their recoverable amount, the initial adjustment is capped at the recoverable amount and the net increase is recorded directly in retained earnings. At the end of the first period and in subsequent periods, all components of equity are restated by applying a general price index from the beginning of the period or the date of contribution, if later.

All items in the statement of cash flows are expressed in terms of the general price index at the end of the reporting period.

The Iranian, Sudanese, South Sudanese and Ghanaian economies have been classified as hyperinflationary. Accordingly, the results, cash flows and financial position of the Group’s subsidiaries: MTN Sudan Company Limited (MTN Sudan), MTN South Sudan Limited (MTN South Sudan), Scancom PLC (MTN Ghana) and the Group’s joint venture, Irancell Telecommunication Company Services (PJSC) (Irancell), have been expressed in terms of the measuring unit current at the reporting date. For further details, refer to note 1.5.5.

1.5 Critical accounting judgements, estimates and assumptions (extract)

1.5.3 Dual exchange rates

Significant judgement

The Group operates in a number of foreign jurisdictions that have multiple quoted exchange rates. When several quoted exchange rates are available in a foreign jurisdiction, the Group uses judgement to determine the rate at which the future cash flows represented by foreign denominated transactions or balances could have been settled if those cash flows had occurred at the measurement date in these foreign entities. For the translation of the results, cash flows and financial position of the foreign entities into the presentation currency of the Group, the Group uses the rate at which dividends can be remitted. If exchangeability between two currencies is temporarily lacking, the rate used is the first subsequent rate at which exchanges could be made.

Further information on the relevant exchange rates is provided in note 7.6.

1.5.5 Hyperinflation

Significant judgement

The Group exercises significant judgement in determining the onset of hyperinflation in countries in which it operates, and whether the functional currency of its subsidiaries, associates or joint ventures is the currency of a hyperinflationary economy.

Various characteristics of the economic environment of each country are taken into account. These characteristics include, but are not limited to, whether:

- The general population prefers to keep its wealth in non-monetary assets or in a relatively stable foreign currency.

- Prices are quoted in a relatively stable foreign currency.

- Sales or purchase prices take expected losses of purchasing power during a short credit period into account.

- Interest rates, wages and prices are linked to a price index.

- The cumulative inflation rate over three years is approaching, or exceeds, 100%.

The analysis of the cumulative inflation rate over three years resulted in the Group considering whether Nigeria’s economy was hyperinflationary. Based on the available information, the Group concluded that this economy is currently not hyperinflationary.

As at 31 December 2023, the information available indicated that South Sudan had ceased to be in hyperinflation from 1 July 2023. However, the latest information indicates that South Sudan remains hyperinflationary. This has been treated as a change in estimate in the current period.

Following management’s assessment, the Group’s subsidiaries, MTN South Sudan, MTN Sudan, MTN Ghana and the Group’s joint venture, Irancell have been accounted for as entities operating in hyperinflationary economies. The results, cash flows and financial positions of MTN Sudan, MTN South Sudan, MTN Ghana and Irancell have been expressed in terms of the measuring units current at the reporting date.

MTN Sudan

The economy of Sudan was assessed to be hyperinflationary during 2018, and hyperinflation accounting has been applied since.

The general price index used as published by the International Monetary Fund is as follows:

The cumulative inflation rate over three years as at 31 December 2024 is 1 267% (2023: 2 550%). The average adjustment factor used for 2024 was 2.31 (2023: 2.29).

MTN South Sudan

The economy of South Sudan has been assessed as hyperinflationary in the year 2016, and hyperinflation accounting has been applied.

The general price index used as published by the National Bureau of Statistics is as follows:

1 The general price index was rebased in August 2024, however, the full year inflation was extrapolated from the original base year of 2007 together with the inflation from August 2024 onwards.

The cumulative inflation rate over three years as at 31 December 2024 is 491% (2023: 30%). The average adjustment factor used for 2024 was 2.62 (2023: 1.04).

Irancell

The economy of Iran was assessed to be hyperinflationary effective 1 January 2020, and hyperinflation accounting has been applied since.

The general price index used as published by the International Monetary Fund is as follows:

The cumulative inflation rate over three years as at 31 December 2024 is 165% (2023: 190%). The average adjustment factor used for 2024 was 1.16 (2023: 1.22).

MTN Ghana

The economy of Ghana was assessed to be hyperinflationary effective 1 January 2023, and hyperinflation accounting has been applied since.

The general price index used as published by the Ghana Statistical Services is as follows:

The cumulative inflation rate over three years as at 31 December 2024 is 118% (2023: 114%). The average adjustment factor used for 2024 was 1.13 (2023: 1.10).

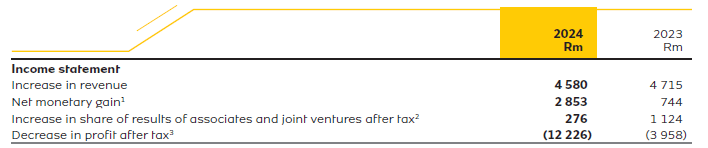

The cumulative impact of adjusting the Group’s results for the effects of hyperinflation is set out below:

1 Significant increase in net monetary gain is mainly due to MTN South Sudan which was accounted for as not being in hyperinflation for the period 1 July 2023 to 31 December 2023.

2 Significant decrease in share of results of associates and joint ventures after tax is mainly due to the decrease in Iran’s inflation rates and devaluation of Iran’s currency (IRR).

3 Significant decrease in profit after tax is due to the impairment of MTN Sudan’s hyperinflated non-current assets, refer to note 5.3.

7.6 Exchange rates to South African rand

1 The financial results, positions and cash flows of foreign operations trading in hyperinflationary economies are translated as set out in note 1.3.3.