Adecoagro S.A. – Half year report – 30 June 2016

Industry: agriculture

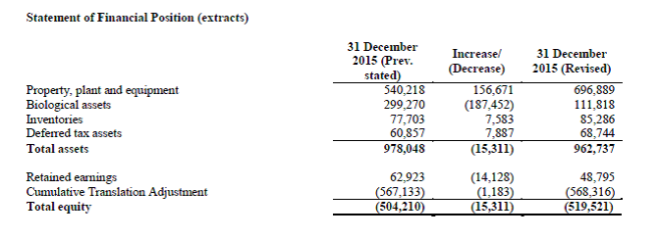

- Basis of preparation and presentation (extract)

Changes in accounting policies

As explained in note 2 below, the group has adopted the amendments made to IAS 16 Property, Plant and Equipment and IAS 41 Agriculture in relation to bearer plants this year. These amendments have resulted in changes in accounting policies and adjustments to the amounts recognized in the financial statements.

(a) Bearer plants

In June 2014, the IASB made amendments to IAS 16 Property, Plant and Equipment and IAS 41 Agriculture which distinguish bearer plants from other biological assets. Bearer plants are solely used to grow produce over their productive lives and are seen to be similar to an item of machinery. They will therefore now be accounted for under IAS 16. However, agricultural produce growing on bearer plants will remain within the scope of IAS 41 and continue to be measured at fair value less cost to sell.

The Group’s sugarcane qualify as bearer plants under the new definition in IAS 41. As required under IAS 8, the change in accounting policy has been applied retrospectively. As a consequence, the sugarcane planting and coffee plantations were reclassified to property, plant and equipment and measured at amortized cost, effective January 1, 2016 and comparative figures have been retrospectively revised accordingly. Sugarcane planting are depreciated on straight-line basis over their useful life which was reassessed from 5 to 6 years as from January 1, 2016.

As permitted under the transitional rules, the fair value of the sugarcane as of January 1, 2014 was deemed to be their cost going forward. The difference between the fair value and the previous carrying amount of was recognized in retained earnings on transition.

However, agricultural produce growing on sugarcane and coffee plantations will remain under the line biological asset and continue to be measured at fair value less cost to sell.

(b) Impact on financial statements

As a result of the changes in the entity’s accounting policies, prior year financial statements had to be revised. The following tables show the adjustments recognized for each individual line item. Line items that were not affected by the change have not been included. As a result, the sub-totals and totals disclosed cannot be recalculated from the numbers provided. As permitted under the transitional rules, the impact on the current period is not disclosed.