Telstra Corporation Limited – Annual report – 30 June 2025

Industry: telecoms

Section 1. Basis of preparation (extract)

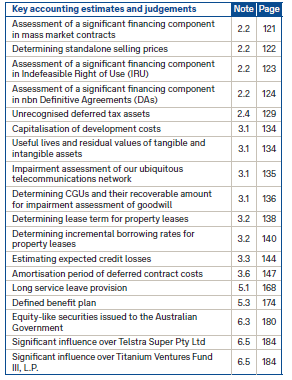

1.4 Key accounting estimates and judgements

Preparation of the financial report requires management to make estimates and judgements.

1.4.1 Summary of key management judgements

The accounting policies and significant management judgements and estimates used, and any changes thereto, are set out in the relevant notes. The key accounting estimates and judgements are included in the following notes:

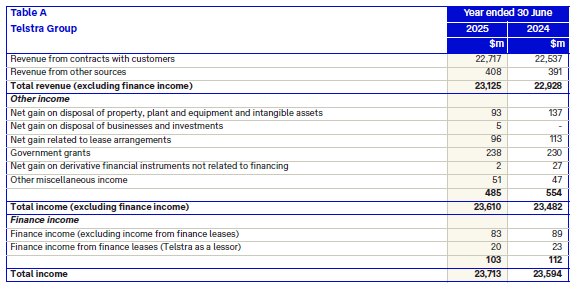

2.2 Income

Revenue from other sources includes income from:

- customer contributions to extend, relocate or amend our network assets, where the customer does not purchase any ongoing services under the same (or linked) contract(s)

- late payment fees

- our lease arrangements, including finance leases where Telstra is a dealer-lessor and operating leases (refer to note 3.2.2 for further details about our lease arrangements).

Net gain on disposal of property, plant and equipment and intangible assets includes $74 million (2024: $110 million) net gain on sale of our legacy copper assets which has been presented net of the disposal costs in the financial year 2025 (2024: presented excluding the disposal costs).

Net gain related to lease arrangements includes $45 million net gain (2024: $1 million net loss) on lease modifications, $20 million (2024: $63 million) gain on finance leases and $31 million (2024: $50 million) net gain on sale and leaseback of certain exchange properties.

Government grants include income under the Telstra Universal Service Obligation Performance Agreement, the Federal Government’s Mobile Black Spot Program and other individually immaterial government grants. There are no unfulfilled conditions or other contingencies attached to these grants.

Net gain on derivative financial instruments not related to financing reflects changes in the fair value of our energy power purchase agreements accounted for as derivative financial instruments.

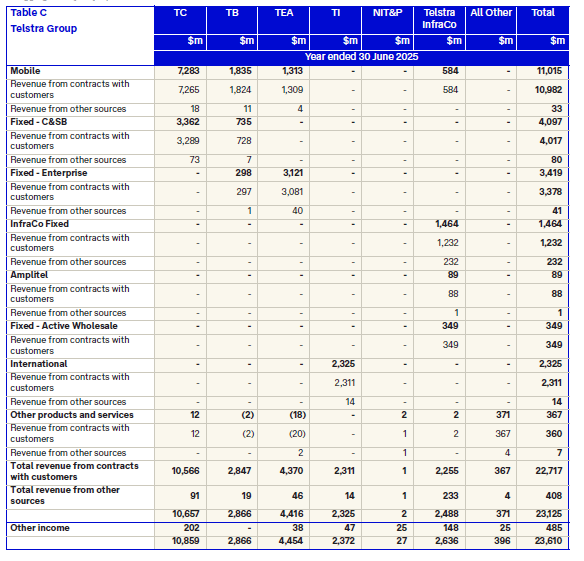

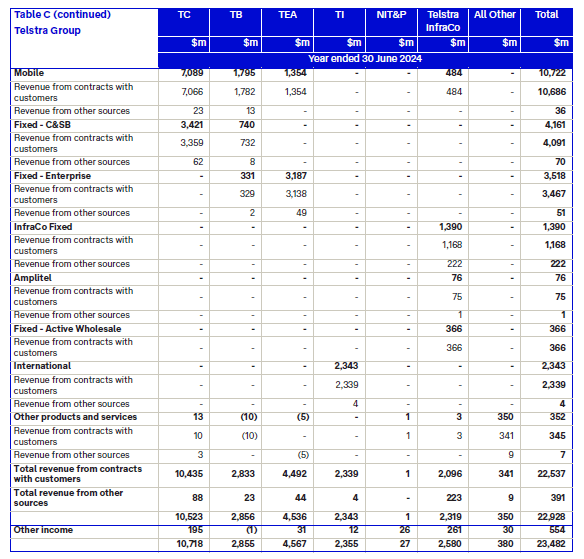

2.2.1 Disaggregated revenue

Table B presents the disaggregated revenue from contracts with customers based on the nature and the timing of transfer of goods and services.

We recognise revenue from contracts with customers when the control of goods or services has been transferred to the customer. Revenue from sale of services is recognised over time, whereas revenue from sale of goods is recognised at a point in time.

Other revenue from contracts with customers includes licensing revenue (recognised either at a point in time or over time) and agency revenue (recognised over time). Refer to note 2.2.2 for further details about our contracts with customers.

Table C presents total revenue from external customers disaggregated by major products.

Revenue from other products and services includes revenue generated by Telstra Health and miscellaneous income.

Negative revenue amounts disclosed in the tables above related to certain corporate level adjustments and consolidation eliminations.

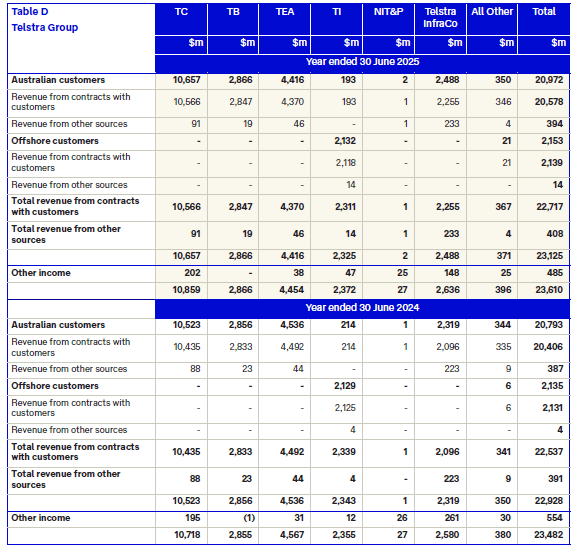

Table D presents total revenue from external customers disaggregated by geographical markets.

Our geographical operations are split between our Australian and offshore operations. No individual foreign country within our offshore operations has material revenue.

We generate revenue from external customer contracts, which vary in their form (standard or bespoke), term (casual, short-term and long-term) and customer segment (consumer, small to medium business, government and large enterprise), with the main contracts being:

- retail consumer contracts (mass market prepaid and post-paid mobile, fixed and media plans)

- retail small to medium business contracts (mass market and off-the-shelf technology solutions)

- retail enterprise and government contracts (carriage, standardised and bespoke technology solutions and their management)

- network capacity contracts, mainly Indefeasible Right of Use (IRU)

- wholesale contracts for telecommunication services

- nbn Definitive Agreements (nbn DAs) and related arrangements.

We sell a wide range of goods and services, which are provided either directly by us or by third parties. Generally, we act as principal rather than an agent in our contracts with customers.

The nature and type of contracts with customers are further described below.

(a) Telstra Consumer (TC) and Telstra Business (TB) contracts

We offer prepaid and post-paid services to our TC and TB mass market customers. Our mass market contracts are homogeneous in nature and sold directly by us or via our dealer channel. These contracts often offer a bundle of goods and services. Some also include options to purchase additional goods or services free of charge or at a discount (i.e. material rights).

We offer no-lock-in (month to month) post-paid service plans to our mobile mass market TC and TB customers. In those arrangements, our customers can purchase a device, either outright or on a device repayment contract, together with a no-lock-in service plan. If a customer cancels their no-lock-in service plan, any outstanding device balance becomes payable immediately.

Where we sell a service plan and a device on a device repayment contract together with that plan, and offer a discount to the customer who takes up that bundle and purchases directly from us, or through a dealer that is acting as our agent, we allocate the discount between the device and services based on their relative standalone selling prices. For our service bundle plans sold via dealers, who in their own right also sell the device to the customer, the whole discount is allocated to services only.

TB also offers fixed plans and technology solutions under fixed term contracts, which incur early termination charges if cancelled by the customer during the fixed term. Fixed term contracts typically have a two to three year term, with the majority of fixed and technology solutions contracts being 24 month contracts.

In some of our fixed post-paid service plans we also act as a lessor in an operating lease for modem devices. Lease components of those contracts are separately accounted for as revenue from other sources.

Generally, we allocate the consideration, and any relevant discounts, to all products in the bundle based on a mixture of observable and estimated standalone selling prices of these products.

By and large we recognise revenue from the sale of goods on their delivery and from sale of services based on the passage of time. The consideration allocated at contract inception to material rights is recognised as revenue either when the customer exercises the option and benefits from the free or discounted products or when the rights are forfeited.

We offer deferred payment terms when customers purchase certain handsets and other devices under a device repayment contract.

Generally, mass market TC and TB contracts are not modified due to their homogeneous nature. However, because our no-lock-in mass market fixed and mobile post-paid service plans are month to month contracts, customers can change plans once each month or cancel their services altogether.

We offer a loyalty program, Telstra Plus, under which our consumer and small business customers can earn points redeemable in the future for certain goods and services. The program also provides customers access to tier benefits in the form of free or discounted entertainment and other services. Points awarded for purchases of Telstra goods and services are accounted for as material rights, with any amount allocated to the points initially recognised as a contract liability in the statement of financial position. When a customer redeems the points or they expire we recognise revenue from sale of goods or services transferred or from forfeiture of the material rights. We also recognise revenue when, based on customers redemption patterns, we expect that the likelihood of the customers utilising the points is remote (i.e. breakage). Discretionary bonus points that do not relate to accounting contracts are classified as a marketing offer and expensed at the time the points are awarded. Tier benefits reduce revenue of the related accounting contracts.

TB offers loyalty programs and technology funds for medium business customers under which they can obtain additional free products. At contract inception, a portion of the consideration is allocated to such products and recognised as a contract liability in the statement of financial position. We recognise revenue when the customer either exercises the option and benefits from the free products or when the rights are forfeited.

(b) Telstra Enterprise Australia (TEA) contracts

TEA transacts with large enterprise and government customers. Large and complex TEA contracts are usually bespoke in nature as they deliver tailored solutions and services. Outside of the large customers, the contracts are mostly standard.

Our TEA legal contracts often are in a form of multi-year framework agreements under which customers can order goods and services. These arrangements include performance conditions and grant different types of discounts or incentives. Such framework agreements are rarely considered contracts for accounting purposes. Instead, revenue recognition rules are applied to goods and services ordered under each valid purchase order or a statement of work raised under the terms of the framework agreement.

In some of our TEA contracts we also act as a dealer-lessor for certain customer premise equipment used by our customers as part of the solutions management and outsourcing services. Leases embedded in those contracts are separately accounted for, usually as dealer-lessor finance leases with finance lease receivables recognised in the statement of financial position.

Some of our TEA contracts include two phases: a build phase followed by the management of the technology solutions. Due to the complex nature of those arrangements, we analyse the facts and circumstances of each contract in order to determine goods and services ordered and timing of revenue recognition. If the build phase (or its components) qualifies as a separate service, we recognise the build phase revenue over the term of the build or at its completion depending on when the customer obtains control over the technology solution.

From time to time our bespoke TEA contracts are varied or renegotiated. When this happens, we assess the scope of the modification or its impact on the contract price in order to determine whether the amendment must be treated as a separate contract, as if the existing contract were terminated and a new contract signed, or whether the amendment must be considered as a change to the existing contract.

Under some of our enterprise arrangements, we receive customer contributions to extend or amend our network assets to ultimately enable delivery of telecommunication services to that customer. Where the counterparty makes a contribution for network construction activities and purchases ongoing services under the same (or linked) contract(s), the upfront contribution is added to the total consideration in the customer contract and is allocated to the goods and services to be delivered under that contract.

Our TEA accounting contracts include multiple goods and services. Generally, we allocate the consideration and any relevant discounts to all the products in the accounting contract based on the standalone selling prices. However, some discounts granted under the framework agreements may be allocated to selected goods or services only if specific performance conditions apply. Any consideration allocated to a lease component is based on the relative standalone selling price of the lease.

We recognise revenue from management services or fixed fee services based on passage of time and from usage-based carriage contracts when the services have been consumed.

Some of our framework agreements offer enterprise loyalty programs and technology funds under which a customer can obtain additional free products. At contract inception, a portion of the consideration is allocated to such products and recognised as a contract liability in the statement of financial position. We recognise revenue when the customer either exercises the option and benefits from the free products or when the rights are forfeited.

Our large commercial arrangements often incorporate service level agreements, e.g. agreed delivery time or service reinstatement time. If we fail to comply with these commitments, we will compensate the customer. The expected amount of such compensation reduces the revenue for the period in which a service level commitment has not been met, and it is recognised as soon as not meeting the commitment becomes probable. Some arrangements also include benchmarking or consumer price index clauses, which are accounted for as variable consideration, usually from the time the price changes take effect.

(c) Telstra International (TI) contracts

TI offers prepaid and post-paid mobile services to consumer customers in South Pacific through Digicel Pacific business. These contracts often offer a bundle of goods and services, including products such as hardware, voice, text and data services, media content and others. TI also offers mobile services, fixed broadband services and technology solutions to small business and enterprise customers.

TI contracts are either fixed term contracts, where early termination charges apply if the customer cancels the contract; or casual month-to-month contracts, where the customer may cancel the contract at any time without any significant termination penalty. Fixed term contracts are typically short term and rarely exceed five years, with the majority of consumer, small business and enterprise contracts with a term of up to three years.

We recognise TI revenue from sale of goods on their delivery and service revenue is generally recognised based on passage of time.

Where goods and services are provided as a bundle, we allocate the consideration and any relevant discounts to all products in the bundle based on their estimated relative standalone selling prices. Where observable prices are not available, we estimate standalone selling prices based on the cost plus margin approach.

Some of our international arrangements include long-term network capacity arrangements (some being take-or-pay arrangements) as well as managed services such as security and backups, for which revenue is usually recognised based on passage of time. IRU arrangements often include upfront payments for services which will be delivered over multiple years.

(d) Telstra InfraCo contracts (excluding contracts with nbn co)

Telstra InfraCo typically transacts with carriage services providers and internet service providers, who in turn sell their services to their end users.

Revenue arises from fixed network service contracts, including usage-based contracts and fixed bundles, with a term typically of up to three years. Other contracts provide data and IP and mobile products such as interconnect, bulk SMS and pre- and post-paid mobile services.

Telstra InfraCo legal contracts are generally signed as multi-year framework agreements, which set out pricing for the agreed services, the term and any renewal options, incentives, discounts and one-off fees.

Some of our framework agreements specify a minimum spend commitment (i.e. a take-or-pay arrangement), in which case the accounting contract may exist also at the framework agreement level.

Customer contributions to extend or amend our network assets to ultimately enable delivery of telecommunication services are recognised when those services are delivered.

Telstra InfraCo’s service revenue is generally recognised over time during the period over which the services are rendered, mostly based on passage of time as the service provider (i.e. our customer) receives unlimited calls and data.

Some of Telstra InfraCo contracts include multiple goods and services. We allocate the consideration, and any relevant discounts, generally to all the products in the accounting contract based on the negotiated prices, which are largely aligned to the estimated standalone selling prices of goods and services promised under the contracts. However, some discounts granted under the framework agreements may be allocated only to selected goods or services based on the specific performance conditions in the framework agreement.

Some of our Telstra InfraCo contracts grant customers access to our passive infrastructure assets. Lease component(s) in those contracts are classified as either operating or finance leases, for which we recognise revenue from other sources or other income, respectively.

(e) Agreements with nbn co

The main contracts with nbn co are nbn DAs and related arrangements.

Revenue from contracts with nbn co is reported within the Telstra InfraCo segment. Amounts recognised as other income are recorded in TC and Telstra InfraCo segments.

Our nbn DAs and related arrangements include a number of separate legal contracts with both nbn co and the Commonwealth Government which have been negotiated together with a common commercial objective. These contracts have been combined for revenue assessment. The combined contract has a minimum term of 30 years for accounting purposes.

The combined nbn DAs and related arrangements include a number of separately priced elements, some of which are not accounted for under the revenue recognition standard. For example, income recognised under the separately priced Telstra Universal Service Obligation Performance Agreement is accounted for as government grant and presented as other income.

Services provided under the Infrastructure Services Agreement (ISA) are accounted for under the revenue recognition standard. We recognise revenue from providing long-term access to our infrastructure, including ducts and pits, dark fibre and exchange rack spaces, over time, initially based on the cumulative nbn network rollout percentage and after rollout completion based on passage of time.

The ISA consideration includes a number of fixed and variable components depending on the progress of the nbn network rollout and the final number of the existing fixed line premises as defined and determined under ISA. Given the nbn network rollout is substantially complete and following contract amendments signed in March 2024, significant variability in the ISA consideration has been removed. However, payments for services delivered under the ISA will continue to be indexed to consumer price index for the remaining contracted period.

The build of nbn related infrastructure was not considered a separate service, therefore payments received for it under a separate legal agreement have been combined and accounted for together with the ISA long-term access services. These upfront payments have been recorded as a contract liability in the statement of financial position and are recognised as services transfer over the ISA average contracted period of 35 years. The remaining contracted period of the ISA is 22 years.

We deliver a number of different services under the nbn DAs and related arrangements, some of which are transferred at different periods to those when we receive the consideration.

2.2.3 Revenue for contracted goods and services yet to be delivered

Sometimes goods and services purchased under the same customer contract will be transferred to the customer over multiple reporting periods.

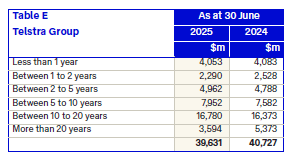

Table E presents aggregate consideration allocated to the remaining goods, services and material rights promised under the contracts where a customer has made a firm commitment before the balance date but goods and services will be transferred after 30 June 2025. Any future amounts arising from contracts where the customer has not made a firm commitment, such as usage-based contracts, are not included in the disclosed amounts. Presented time bands best depict the future revenue recognition profile.

Future revenue arising from nbn DAs is estimated based on assumptions which are reassessed at each reporting period. However, given its size, long-term nature and variable consideration components (refer to note 2.2.2 for details), the actual amounts recognised in the future periods may still materially differ from our estimates.

Any amounts arising from our existing customer contracts which will be recognised as ‘revenue from other sources’ or ‘other income’, for example operating lease income or net gain on sale of assets, are excluded from revenue for contracted goods and services yet to be delivered.

2.2.4 Recognition and measurement

Our revenue recognition accounting policies are described below.

(a) Revenue from contracts with customers

Revenue from contracts with customers arises from goods and services sold as part of our ordinary activities.

(i) Accounting contracts with customer

Revenue recognition principles are applied to accounting contracts which are agreements between two or more parties that create enforceable rights and obligations.

The accounting contract may not align with the legal contract and in some cases multiple legal contracts may need to be combined to form one accounting contract. In other instances, a legal contract may only provide a framework agreement (i.e. an offer) and an accounting contract only exists when the customer commits to purchase goods or services.

Any components of the contract which are accounted for under other accounting standards are separated out and accounted for under those other standards.

(ii) Goods, services and/or material rights

Revenue is recognised when Telstra fulfils its contractual obligation to deliver promised goods and services (or a bundle of goods and services) to the customer.

A contractual promise giving the customer an option to purchase additional goods and services at a discount (i.e. material right) must be accounted for separately if the incremental discount is at least five per cent compared to other customers. For arrangements with an incremental discount lower than five per cent, judgement is required to determine if material rights should be accounted for separately if the aggregate impact is significant. For example, this might be the case for arrangements offering material rights to our retail customers.

A good or service is separately accounted for if a customer can benefit from it on its own or together with other readily available resources, and no transformative relationship exists with other promised goods or services.

(iii) Variable consideration

If a contractual amount includes a variable component, we estimate the amount to which we will be entitled in exchange for promised goods and services. Examples of variable consideration include discounts, rebates, refunds, credits and price concessions. To estimate an amount of variable consideration, we use either the most likely amount or the expected value method depending on which better predicts the variable amount. The variable consideration is estimated at contract inception and constrained until it is highly probable that a significant reversal of cumulative revenue recognised will not occur.

(iv) Significant financing component

If the period between when we would transfer the good or service to the customer and when the customer would pay for them is expected to be greater than one year, we assess whether revenue should be adjusted for significant financing component, i.e. reduced if we offer deferred payment terms or increased if we receive an advance payment from customer. The significance of financing is assessed relative to the total contract value and interest rates used reflect credit characteristics of the counterparty receiving financing.

(v) Allocation of revenue to goods and services

We allocate the consideration to the goods and services based on their relative standalone selling prices. Standalone selling price is the price for which we would sell the goods or services on a standalone basis, i.e. not in a bundle. We determine standalone selling price at contract inception using an observable price for a standalone sale of substantially the same good or service under similar circumstances and to a similar class of customers. If no observable price is available, we estimate the standalone selling price using an appropriate method, e.g. adjusted market assessment approach, expected cost plus a margin approach or a residual approach.

In some instances, in order to correctly reflect the amount of revenue we expect to be entitled to, we allocate variable consideration, discounts or a significant financing component to some but not all goods, services and/or material rights.

(vi) Timing of revenue recognition

Revenue is recognised when control of the good or service is transferred to the customer, i.e. when the customer can benefit from the good or service and decide how to use them.

We recognise revenue over time when the customer simultaneously receives and consumes the benefits provided to them or we create or enhance an asset controlled by the customer. Otherwise, we recognise revenue at a point in time.

We use either input or output methods to measure progress when selling goods or services. Output methods use direct measurements of the value to the customer, for example, milestones reached. Input methods use our efforts or inputs in measuring the performance, for example, our labour hours used relative to the total expected labour hours.

When revenue is recognised at a point in time, the allocated consideration is recognised when control over a good is transferred to the customer. In determining this, we consider the customer’s obligation to pay, transfer of legal title to the good, physical possession of the good, the customer’s acceptance, and risks and rewards of ownership.

(vii) Contract modifications

From time to time, our contracts are renegotiated after contract inception and their scope and/or price change. A contract modification will result in a cumulative change to revenue already recognised only when the remaining goods and services are not separate from those already delivered.

(viii) Gross versus net presentation

When we control the promised goods and services before they are transferred to the customer and we have primary obligation for their delivery, we act as principal in the contract with a customer and recognise revenue at gross amounts. When we act as an agent of a third-party provider, we recognise revenue net of amounts payable to that third party.

(b) Revenue from other sources

Revenue from other sources includes income arising from arrangements other than those accounted for under the revenue recognition standard.

Contract terminations generally trigger different rights and obligations. These rights and obligations are not related to our performance and were not considered at inception of the accounting contract. Therefore, where relevant, any income over and above the recovery of the consideration due for the delivered goods or services is not classified as revenue from customer contracts. Instead, we classify it as revenue from other sources.

We earn revenue from some of our lease arrangements described in note 3.2. This includes revenue from operating leases and from finance leases where Telstra is a dealer-lessor of customer premise equipment. We recognise revenue from operating leases over the lease term, and revenue from sale of goods as a dealer-lessor at a point in time at the commencement date of the lease.

Where a (combined) accounting contract includes lease and non-lease components and Telstra is a lessor, we allocate the consideration to lease and non-lease components applying the relative standalone selling prices requirements for revenue from contracts with customers.

We receive contributions to extend, relocate or amend our network assets. Where the counterparty makes a contribution for network construction activities that is neither a government grant nor relates to the purchase of ongoing services under the same (or linked) contract(s), we recognise revenue over the period of the network construction activities.

Revenue from other sources also includes late payment fees, which are recognised when charged and their collectability is reasonably assured.

(c) Government grants

Government grants are recognised where there is reasonable assurance that the grant will be received and Telstra will comply with all attached conditions. Government grants relating to costs are deferred and recognised in the income statement as other income over the period necessary to match them with the costs that they are intended to compensate.

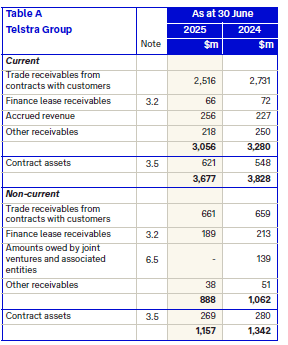

3.3 Trade and other receivables and contract assets (extracts)

3.3.1 Current and non-current trade and other receivables and contract assets (extracts)

The majority of our receivables are in the form of contracted agreements with our customers. In general, the terms and conditions of these contracts require settlement between 14 and 30 days from the date of invoice. Credit risk associated with trade and other receivables and contract assets has been provided for.

Our trade receivables include receivables with deferred payment terms over 12, 24 or 36 months arising from mass market plans of hardware and services. Amounts expected to be collected within 12 months from the reporting date are presented as current assets.

Trade receivables from contracts with customers represent an unconditional right to receive consideration (primarily cash) which normally arises when the goods and services have been delivered and/or a valid invoice has been issued. By contrast, contract assets relate to our rights to consideration for goods or services provided to the customer but for which we do not have an unconditional right to payment at the reporting date.

In general, we invoice customers in advance for services provided under our prepaid or fixed fee (usually monthly) contracts and in arrears for usage-based contracts (e.g. carriage services under enterprise contracts). In those cases, we would recognise a contract liability and a contract asset, respectively.

Refer to note 3.5 for movements in net contract assets and contract liabilities.

Other current receivables include funds that do not meet the criteria to be classified as cash and cash equivalents as they are not available for use by the Telstra Group. They mainly include $15 million (2024: $12 million) monies held on behalf of our Digicel Pacific customers in respect of the mobile money business.

Refer to note 6.5.1 for further details on amounts owed by joint ventures and associated entities.

(a) Impairment of trade and other receivables and contract assets

Trade and other receivables and contract assets are exposed to customers’ credit risk and are subject to impairment assessment.

If a credit loss (i.e. a shortfall between the contractual and expected cash flows) is expected, an allowance for doubtful debt is raised to reduce the carrying amount of trade and other receivables and contract assets. For both receivables and contract assets we estimate the expected credit loss using one or a combination of a portfolio approach and/or an individual account by account assessment as detailed below.

(i) Portfolio approach

The portfolio approach is based on historical credit loss experience and, where appropriate, adjusted to reflect current conditions and estimates of future economic outlook. This approach is mostly applied to balances arising from our consumer and small to medium business customer contracts. Under this approach, receivables and contract assets are grouped based on shared credit risk characteristics, such as:

- account status (services still active or not)

- customers’ payment history

- the days past due.

For each grouping, the expected credit loss is then calculated on the probability that an account within the group will default (i.e. it will become past due by more than 90 days, or when an invoice will be overdue for our no-lock-in consumer plans) and the expected loss rate when they default, both represented as a percentage of the exposure at default and determined at the customer account level.

Our provision rates range from 0.1 per cent (2024: 0.1 per cent) for balances not past due to 91.0 per cent (2024: 91.0 per cent) for balances where the payment is overdue by more than 90 days and the customer’s services have been deactivated.

(ii) Individual approach

The individual approach is an account by account assessment based on credit history, knowledge of debtor’s financial situation, such as insolvency or entering a payment plan, or other known credit risk specific to the debtor, such as judgement based on the debtor’s industry. This approach is applied to balances arising from contracts with large enterprise and government customers as well as to other accounts in TEA, TI, Telstra InfraCo, TC and TB segments where some detrimental change in payment behaviour has been noticed or certain thresholds have been exceeded by a customer.

Balances arising from our transactions with nbn co (reported in Telstra InfraCo and TC segments) are separately assessed based on the Australian government credit risk rating.

We estimate our allowance for impairment as detailed below.

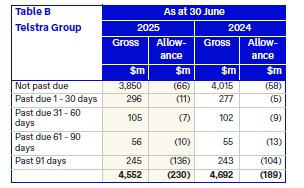

The aging analysis and loss allowance in relation to trade receivables from contracts with customers, finance lease receivables and contract assets are detailed in table B. The analysis is based on the original due date of the receivables, including where repayment terms for certain long outstanding receivables have been renegotiated. Contract assets are not yet due for collection, thus the entire balance has been included in the ‘not past due’ category. Unallocated receipts from or credits granted to customers have been included in the ‘not past due’ category.

Accrued revenue, amounts owed by joint ventures and associated entities, and other receivables (before allowance for doubtful debts) totalling $524 million (2024: $675 million) are subject to impairment assessment using the general approach and include 55 per cent (2024: 33 per cent) of balances with counterparties with an external credit rating of A- or above, and 19 per cent (2024: 40 per cent) of balances with counterparties with an external credit rating between B+ and B-. The remaining balance is related to individually insignificant debtors, and there is no concentration of credit risk in those amounts.

We hold security for a number of trade receivables, including past due or impaired receivables, in the form of guarantees, letters of credit and deposits. During the financial year 2025, the securities we called upon were insignificant. These trade receivables, along with our trade receivables that are neither past due nor impaired, comprise customers who have a good debt history and are considered recoverable. Further, we limit our exposure to credit risk from trade receivables by establishing a maximum payment period and, in certain instances, cease providing further services after 90 days from the past due date (or 30 days for our no-lock-in consumer plans).

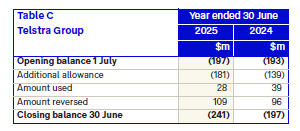

Movements in the allowance for doubtful debts in respect of all our trade and other receivables and contracts assets, regardless of the method used in measuring the impairment allowance, are detailed in table C.

Impairment allowance related to accrued revenue, amounts owed by joint ventures and associated entities, and other receivables (i.e. balances not presented in table B) amounted to $11 million (2024: $8 million).

3.3.2 Recognition and measurement

Trade and other receivables and contract assets are financial assets which are initially recorded at fair value and subsequently measured at amortised cost using the effective interest method.

Contract assets are initially recorded at the transaction price allocated as compensation for goods or services provided to customers for which the right to collect payment is subject to providing other goods or services under the same contract (or group of contracts) and/or we are yet to issue a valid invoice. Contract assets are subsequently measured to reflect relevant transaction price adjustments (where required) and are transferred to trade receivables when the right to payment becomes unconditional.

(a) Impairment of financial assets

We estimate the expected credit losses for our financial assets (including contract assets) measured at amortised cost depending on their nature on either of the following basis:

- for accrued revenue, amounts owed by joint ventures and associated entities, and other receivables – using a general approach, i.e. 12-month expected credit loss which results from all possible default events within the 12 months after the reporting date. However, if the credit risk of a financial asset at the reporting date has increased significantly since its initial recognition, loss allowance is calculated based on lifetime expected credit losses.

- for trade receivables from contracts with customers, contract assets and lease receivables – using a simplified approach, lifetime expected credit loss which results from all possible default events over the expected life of a financial instrument.

Any expected credit loss is discounted at the original effective interest rate.

Any customer account with debt more than 90 days past due (or when an invoice is overdue for our no-lock-in (month to month) mass market plans) is considered to be in default.

Trade and other receivables and contract assets are written off against the impairment allowance or directly against their carrying amounts and expensed in the income statement when all collection efforts have been exhausted and the financial asset is considered uncollectable. Factors indicating there is no reasonable expectation of recovery include insolvency and significant time period since the last invoice was issued.

3.4 Contract liabilities and other revenue received in advance

Contract liabilities arise from our contracts with customers and represent amounts paid (or due) to us by customers before receiving the goods and/or services promised under the contract.

Other revenue received in advance comprises upfront consideration under contracts giving rise to revenue from other sources or other income, for example from sale of assets.

Amounts expected to be recognised as revenue within 12 months from the reporting date are presented as current liabilities.

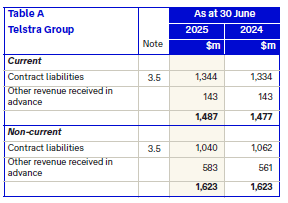

Table A presents customer payments received in advance under different types of our commercial arrangements.

3.5 Net contract assets and contract liabilities

Contract assets and contract liabilities arise due to the timing differences between revenue recognition and customer invoicing. Our billing arrangements for goods and services as well as different types of discounts, credits or other incentives can vary depending on the type and nature of the contracts with customers. As a result, at times under the same accounting contract, we may recognise both a contract asset and a contract liability. At each reporting date, any balances arising from the same accounting contract are presented net in the statement of financial position as either a net contract asset or a net contract liability.

The net presentation mainly impacts our small to medium business and enterprise framework arrangements that offer loyalty programs and technology funds, and nbn Definitive Agreements, where multiple legal contracts have been combined as one accounting contract.

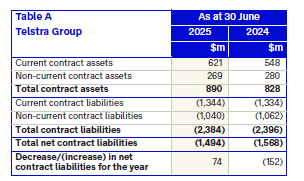

Table A presents opening and closing balances of our current and non-current contract assets and contract liabilities and their total net movement for the period.

Generally, contract assets increase when we recognise revenue for goods and services transferred to the customer before billing and decrease when we invoice customers for already provided goods and services.

On the other hand, contract liabilities increase when we receive consideration in advance of transferring the goods and services to the customer, and decrease when we recognise revenue for the goods and services previously prepaid by the customer.

Other changes in our contract assets and contract liabilities represent movements resulting from changes in the transaction prices due to timing of invoicing and recognition of discounts, credits and other incentives.

The following selected movements contributed to the overall decrease of $74 million (2024: $152 million increase) in the net contract liabilities:

- $1,382 million (2024: $1,441 million) revenue recognised in the reporting period that was included in the contract liabilities balance at the beginning of the reporting period

- $7 million increase (2024: $14 million) reflecting cumulative catch-up adjustments to revenue recognised in the prior reporting periods

- $11 million net decrease (2024: nil) reflecting reclassification to assets and liabilities classified as held for sale.

Refer to note 3.3.1 for details regarding impairment assessment of contract assets.

3.6 Deferred contract costs

We pay dealer commissions to acquire customer contracts and we incur upfront set-up and other costs related to customer contracts. When those costs support the delivery of goods and services in the future and are expected to be recovered, they are deferred in the statement of financial position and amortised on a basis consistent with the transfer of goods and services to which these costs relate.

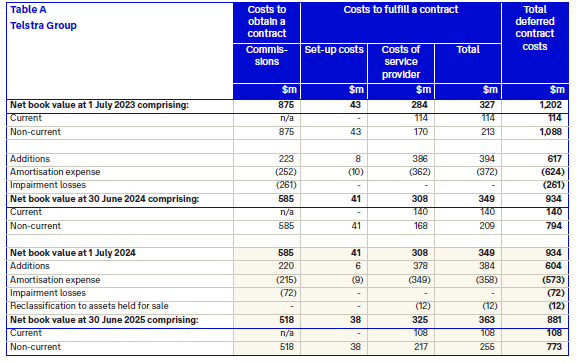

Table A provides movements in net book values of the deferred contract costs.

3.6.1 Recognition and measurement

We capitalise costs to obtain an accounting contract when the costs are incremental, i.e. would not have been incurred if the contract had not been obtained and are recoverable either directly via reimbursement by the customer or indirectly through the contract margin.

We immediately expense the incremental costs of obtaining contracts if the period of benefit is one year or less.

Costs to fulfil a contract relate directly to an identified good or service or indirectly to other activities that are necessary under the contract but that do not result in a transfer of goods or services.

Costs to fulfil a contract include set-up costs and prepaid costs of a service provider related to goods and services which will be transferred in the future reporting periods.

We capitalise costs to fulfil a contract if:

- the costs relate directly to a contract or a specifically identified anticipated contract

- the costs generate or enhance resources that we control and will use when transferring future goods and services

- we expect to recover the costs.

We amortise deferred contract costs in ‘goods and services purchased’ expense over the term that reflects the expected period of benefit of the expense. This period may extend beyond the initial contract term to the estimated customer life or average customer life of the class of customers. We use the amortisation pattern consistent with the method used to measure progress and recognise revenue for the related goods or services.

We assess whether deferred contract costs are impaired whenever events or changes in circumstances indicate that the carrying amounts may not be recoverable. We recognise impairment losses in ‘other expenses’.