Sysmex Corporation – Annual report – 31 March 2020

Industry: healthcare

3. SIGNIFICANT ACCOUNTING POLICIES (extract)

(4) Financial instruments (extract)

1) Financial assets (extract)

2) Impairment of financial assets

In terms of financial assets measured at amortized cost, an assessment is made at each reporting date as to whether or not the credit risk on financial assets has increased significantly since the initial recognition, and the following amounts are recognized as an impairment loss depending on whether or not a significant increase in credit risk has occurred since the initial recognition:

(i) If credit risk has not increased significantly since initial recognition:

Amount equal to 12-month expected credit losses

(ii) If credit risk has increased significantly since initial recognition:

Amount equal to lifetime expected credit losses

However, for trade receivables, contract assets, and lease receivables, impairment losses in the amount equivalent to lifetime expected credit losses are recognized, regardless of whether the credit risk has increased significantly since initial recognition.

Expected credit losses are calculated in the following manner:

(i) Trade receivables, contract assets, and lease receivables

- Assets for which credit risk has not increased significantly since initial recognition:

Expected credit losses are calculated by multiplying the probability of default expected to occur in the future of similar assets by the carrying amount.

- Assets for which credit risk has increased significantly since initial recognition and assets that fall under credit-impaired financial assets:

The recoverable amounts are estimated individually, and the difference between the recoverable amounts and the carrying amounts is recognized as expected credit loss.

(ii) Assets other than (i) above

- Assets for which credit risk has not increased significantly since initial recognition:

Expected credit losses are calculated by multiplying the probability of default expected to occur in the future of similar assets by the carrying amount.

- Assets for which credit risk has increased significantly since initial recognition and assets that fall under credit-impaired financial assets:

The recoverable amounts are estimated individually, and each expected credit loss is measured as the difference between the present value of such assets discounted by the initial effective interest rate and the carrying amount.

The carrying amount of financial assets for which an impairment loss has been recognized is reduced through loss allowance, and impairment loss is recognized in profit or loss. In addition, when the Group has no reasonable expectations of recovering a financial asset, the carrying amount of the financial asset is reduced directly and the corresponding allowance account is also reduced.

If, after recognition of an impairment loss, the amount of impairment loss is reduced, the amount of reduction of the impairment loss is reversed in net profit or loss through the allowance account.

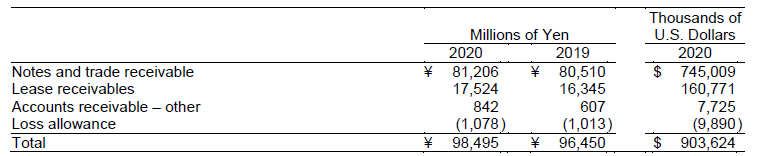

7. TRADE AND OTHER RECEIVABLES Trade and other receivables consist of the following:

Trade and other receivables are classified as financial assets measured at amortized cost.

15. LEASES (extract)

(1) Lessor

For the fiscal year ended March 31, 2019, the Group has applied IAS 17 (Lease).

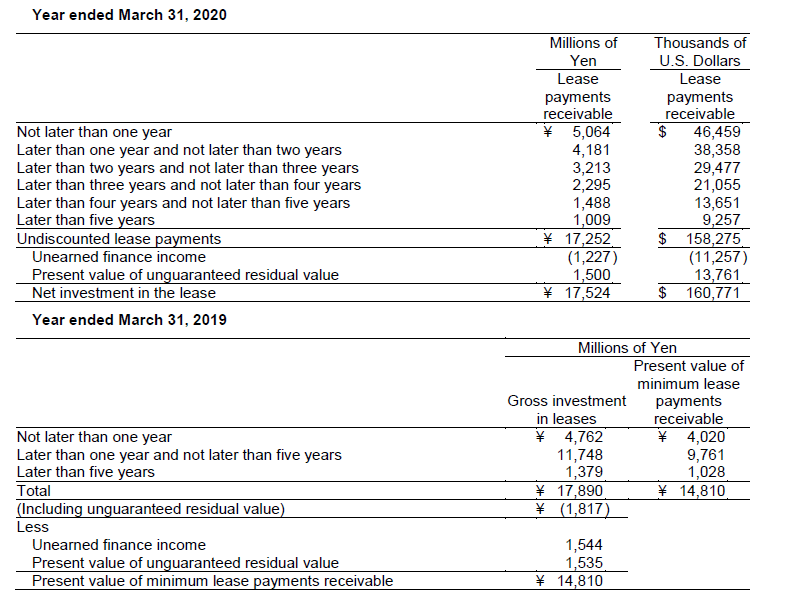

1) Finance leases

The Group leases diagnostic instruments and others under finance leases.

Risks related to the underlying assets are reduced by providing maintenance services throughout the lease period.

Lease payments receivable (gross investment in leases, present value of minimum lease payments receivable, and adjustments for prior fiscal year) relating to finance leases are as follows:

2) Operating leases

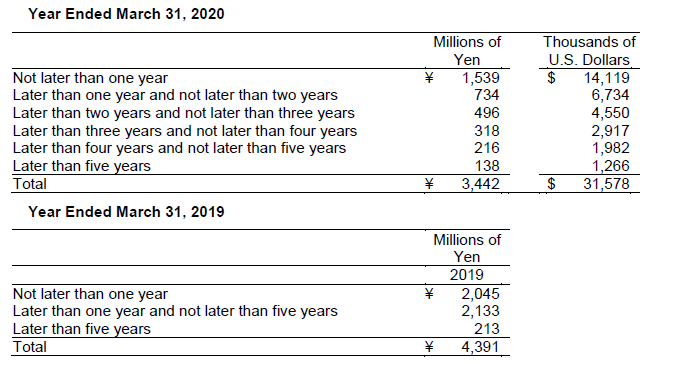

The Group leases diagnostic instruments and others under operating leases.

Risks related to the underlying assets are reduced by providing maintenance services throughout the lease period.

Future minimum lease payments expected to be received under operating leases (non-cancellable operating leases in previous fiscal year) are as follows:

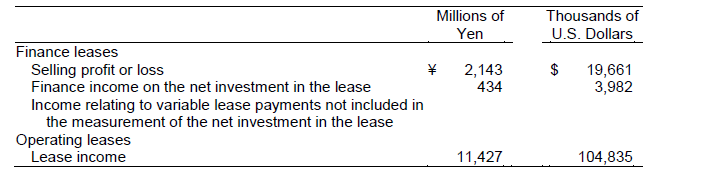

Lease income from lease contracts in which the Group serves as a lessor for the year ended March 31, 2020, is as follows:

In the lease income, ¥5,574 million ($51,138 thousand) of variable lease payments which do not depend on index or rate is included for the year ended March 31, 2020.

19. OTHER ASSETS AND LIABILITIES

Other current assets, other non-current assets, other current liabilities, and other non-current liabilities consist of the following:

29. FINANCIAL INSTRUMENTS (extract)

(3) Credit risk management

The Company manages its credit risk from receivables on the basis of internal guidelines, which include monitoring of payment terms and balances for major customers by each business administration department in order to identify at an early stage any customer default risks due to deteriorating finances. The credit risk regarding subsidiaries is also managed in the same manner.

Credit risk from derivatives is minimized due to dealing only with large financial institutions.

The carrying amounts of financial assets after impairment loss stated in the consolidated statement of financial position represent the maximum exposure to credit risk at reporting dates that do not take into account collateral and other credit enhancements. The counterparties and trading areas of the Group are extensive, and no significant concentration of the credit risk has occurred.

The Group calculates the loss allowance by classifying them into the categories of trade, contract assets, and lease receivables, and non-trade and non-lease receivables. Both types of financial assets are treated as defaults at the point when contracted payment terms and conditions cannot be met.

The Group recognizes loss allowance for all trade and lease receivables at an amount equal to the lifetime expected credit loss. Loss allowance is calculated to reflect the following factors:

- Unbiased, probability-weighted amounts derived by evaluating the probable results within a certain range;

- Time value of money;

- Reasonable and supportable information that is available without undue cost or effort at the reporting date, about past events, current conditions, and future economic conditions.

For both types of financial assets, when evaluating whether or not the credit risk has increased significantly, in addition to information on due dates, the Group considers information that can be reasonably used and supported by the Group. Both types of financial assets are treated as credit-impaired financial assets in the event that the borrower requests revision of the payment terms and conditions, the borrower falls into serious financial difficulty, or legal liquidation procedures commence due to the borrower’s bankruptcy, etc. In terms of amounts that are clearly not capable of being collected in future periods, the carrying amounts of financial assets are directly reduced and the corresponding loss allowance is also decreased.

Changes in the loss allowance are as follows:

Note:

There are no financial assets for which credit risk is significantly increasing for the whole period, except for trade and lease receivables.

Changes in the gross carrying amount of financial assets are as follows:

Note:

There are no financial assets for which credit risk is significantly increasing for the whole period, except for trade and lease receivables.

No financial assets for which loss allowance was recorded at initial recognition were recognized for the years ended March 31, 2020 and 2019.

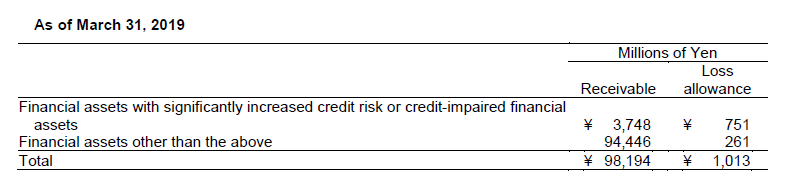

The carrying amounts of financial assets for which loss allowance was recognized are as follows: