Chemring Group PLC – Annual report – 31 October 2020

Industry: manufacturing

Environment (extract)

Reducing our environmental impact (extract)

Our goal of zero harm goes beyond the management of safety. We are committed to environmental sustainability, both globally and in our local communities, and reducing our environmental impact.

Introduction

Our environmental performance information is presented in accordance with the Streamlined Energy and Carbon Reporting (“SECR”) Guidance (March 2019), as specified under the Companies Act 2006 (Strategic Report and Directors’ Report) Regulations 2013. Data is presented for our financial year, from 1 November through to 31 October, and includes information on our most significant environmental aspects: energy consumption and associated greenhouse gas (“GHG”) emissions; freshwater use; and waste generation. The scope of the reporting includes all continuing global businesses under our operational control and does not include several small leased office spaces used for drop-in needs, where we do not have energy data and they are not in our operational control.

Our GHG emissions calculations are undertaken in accordance with the GHG Protocol Corporate Accounting and Reporting Standard. We are reporting 2019 and 2020 data and include scope 1 GHG emissions, as well as location- and market-based approaches for scope 2 emissions of purchased electricity. Our key scope 1 emissions sources are natural gas and fuel oil used for building and process heating, with small contributions from fuels used in on-site vehicles and refrigerant releases. Primary scope 1 emissions are CO2, with small contributions from CH4, N2 and HFCs.

For the purpose of this report, we are restating our 2019 data, excluding companies no longer under our operational control, to allow 2019 to be used as a baseline for GHG emissions and to compare progress made in 2020. We have reviewed and adjusted, where needed, 2019 figures following our data review. For waste generation, we are using 2020 as a baseline.

Our approach

We are actively seeking ways to reduce our impact on the environment and build resilience to climate change by focusing on energy, waste and water, and understanding the impact of global climate change on our operations. These four focus areas have been identified based on an overall evaluation of environmental impacts and risks, with a focus on impacts that we can influence. These focus areas will be periodically reviewed by our newly established Environmental Committee, consistent with broader sustainability goals and reporting guidelines.

Many of our Chemring businesses have environmental management systems and have undertaken local initiatives and programmes to reduce environmental impacts. This year we have implemented a more centralised, robust approach to drive environmental performance and collect more accurate data.

Our strategy

Our strategy is to reduce our global GHG emissions through improving energy efficiency to reduce consumption and by purchasing electricity from renewable sources. In 2018, Chemring made a conscious decision to purchase its UK electricity using REGO-backed renewable energy contracts.

This purchasing covers our UK businesses, namely Chemring Energetics UK, Roke, Chemring Countermeasures UK and our HQ based in Romsey, and reduced our total CO2e impacts by over 9% as noted in the market-based CO2e values below.

To improve our energy efficiency, we have made improvements to our operations, including installing new energy-efficient buildings to replace old buildings, upgrading HVAC systems and improving lighting. Improvements in lighting technology provide safety, maintenance and energy savings.

Several of our businesses have implemented relamping projects to replace fluorescent lighting with LED lighting. LED lighting provides significant advantages over more traditional fluorescent lighting in terms of reduced energy consumption, less maintenance and provides a safer way to light our operational areas. Fluorescent and HID bulbs need regular replacement and are more costly to operate than LEDs.

In our Chicago operations, 75 460-watt fixtures have been replaced with 232-watt fixtures, giving a total energy saving of 17,100 watts. Similarly, our North Carolina facility has replaced all Hi-Bay lighting with LED lamps providing 30,000 watts of savings. In addition, replacing fluorescent fixtures at that facility with LEDs provided 50,000 watts of savings. Our Scotland facility, one of larger energy users, is performing a similar exercise.

Climate change resilience

We recognise that climate change has the potential to have an impact on our operations, having experienced flooding from a severe weather event at our Tennessee facility in 2018 and wildfires in areas surrounding our Australia operations in 2019. We intend to review the physical and transition risks of global climate change on our operations and supply chain. Mitigation measures taken to date include improving drainage at our Tennessee facility and maintaining lower vegetation heights at the Australian and Norwegian sites.

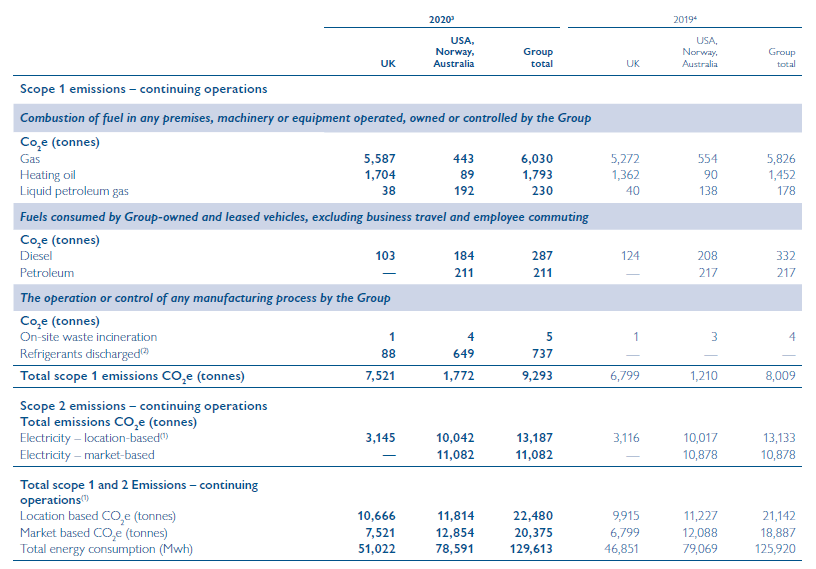

Energy use and associated GHG emissions for 2020 and 2019

In 2020, we recorded a 14% reduction in energy usage normalised to sales. Our Countermeasure & Energetics businesses in Norway and Scotland are responsible for 37% and 28%, respectively, of the energy usage of the Group. This is followed by our business in Tennessee, which consumed 15% of annual energy consumption. Norway and Scotland have energy reduction plans in place, and the Tennessee business is reviewing energy reduction opportunities. Our UK operations account for 81% of our scope 1 emissions, 24% of our scope 2 emissions and 39% of our energy use. In terms of GHG emissions, in 2020 we observed an 6% increase in scope 1 and 2 emissions from 21,142 tCO2e in 2019 to 22,480 tCO2e in 2020 using location-based emission factors. When normalised for gross revenues, this reflects a decrease of 11.5%, from 63.1 to 55.8.

Notes:

1. Our 2019 annual report noted total scope 1 and 2 GHG emissions of 28,591 tonnes of CO2 equivalents. Following a re-evaluation of energy use data and calculations, and with the removal of discontinued operations to allow 2019 to be used as a baseline, the new 2019 total is 21,142 CO2e tonnes.

2. Impacts from the release of refrigerants are included in the 2020 scope 1 data (representing 8% of the scope 1 total) however, this information was not available and thus not included in restated 2019 figures.

3. Our 2020 and restated 2019 data does not include environmental impacts associated with Chemring Ordnance, Chemring Energetic Devices Torrance and Santa Clarita, and Chemring Defence UK, which were sold or closed during the reporting period.

4. As part of our data validation, several discrepancies were noted in last year’s report; these have been addressed in the table above. The previous 2019 values overstated the CO2e emissions by 6.7%.