CLP Holdings Limited – Annual report – 31 December 2025

Industry: utility

16. Derivative Financial Instruments

Accounting Policy

A derivative is initially recognised at fair value on the date a derivative contract is entered into and is subsequently remeasured at fair value. The method of recognising the resulting gain or loss depends on whether the derivative is designated as a hedging instrument, and if so, the nature of the item being hedged. Fair value gain or loss arising from derivatives not designated or not qualified for hedge accounting are recognised immediately in profit or loss.

The Group designates certain derivatives as either fair value hedges, which are hedges of the fair value of recognised financial assets or financial liabilities or firm commitments (e.g. fixed interest rate loans and foreign currency trade receivables) or cash flow hedges, which are hedges of the cash flows of recognised financial assets or financial liabilities or highly probable forecast transactions (e.g. floating interest rate loans and future purchases of fuels denominated in US dollar).

The Group documents at the inception of the hedging the economic relationship between hedging instruments and hedged items, as well as its risk management objectives and strategy for undertaking hedge transactions. The Group also documents its assessment, both at hedge inception and on an ongoing basis, of whether the hedging relationship meets the hedge effectiveness requirements.

(A) Fair value hedges

Changes in the fair values of derivatives that are designated and qualify as fair value hedges are recognised in profit or loss, which offset any changes in the fair values recognised in profit or loss of the corresponding hedged asset or liability that are attributable to the hedged risk and achieve the overall hedging result.

(B) Cash flow hedges

The effective portion of changes in the fair values of derivatives that are designated and qualify as cash flow hedges is recognised in other comprehensive income. The ineffective portion is recognised immediately in profit or loss.

Amounts accumulated in equity are reclassified to profit or loss in the periods when the hedged items affect profit or loss. Such reclassification from equity will offset the effect on profit or loss of the corresponding hedged item to achieve the overall hedging result. However, when the highly probable forecast transaction that is hedged results in the recognition of a non-financial asset (for example, inventory or fixed assets), the gains and losses previously deferred in equity are transferred from equity and included in the initial measurement of the cost of the asset at the time of acquisition. The deferred amounts are ultimately recognised in fuel costs in the case of inventory or in depreciation in the case of fixed assets.

When a hedging instrument expires, or is sold or terminated, or when a hedge no longer meets the criteria for hedge accounting, hedge accounting is discontinued prospectively. Any cumulative gain or loss remains in equity at that time is accounted for according to the nature of the underlying transactions (as discussed above) once the hedged cash flow occurs. When a forecast transaction is no longer expected to occur, the cumulative gain or loss that has been recorded in equity is reclassified to profit or loss immediately.

(C) Costs of hedging

Forward element of forward contracts and foreign currency basis spread of financial instruments may be separated and excluded from the designated hedging instruments. In such case, the Group treats the excluded elements as costs of hedging. The fair value changes of these elements are recognised in a separate component of equity. For time-period related hedged items, these elements at the date of designation (to the extent that it relates to the hedged item) are amortised on a systematic and rational basis to profit or loss over the hedging period. For transaction related hedged items, the cumulative change of these elements is included in the initial carrying amount of any non-financial asset recognised when the hedged transaction occurs or is recognised in profit or loss if the hedged transaction affects profit or loss.

(D) Rebalancing of hedge relationships

If the hedge ratio for risk management purposes is no longer optimal but the risk management objective remains unchanged and the hedge continues to qualify for hedge accounting, the hedge relationship will be rebalanced by adjusting either the volume of the hedging instrument or the volume of the hedged item so that the hedge ratio aligns with the ratio used for risk management purposes. Any hedge ineffectiveness is calculated and accounted for in profit or loss at the time of the hedge relationship rebalancing.

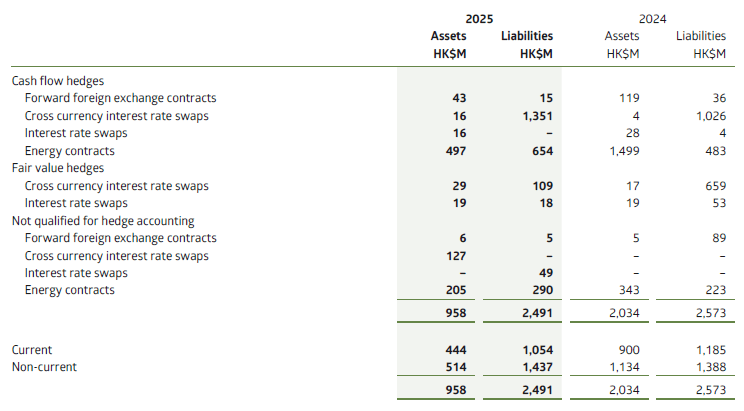

At 31 December 2025, the contractual maturity profile of the hedging instruments from the end of the reporting period is summarised below:

Financial Risk Management (extract 1)

1. Financial Risk Factors

The Group’s activities expose it to a variety of financial risks: market risk (including foreign exchange risk, fair value and cash flow interest rate risks, and energy portfolio risk), credit risk and liquidity risk. The Group’s overall risk management programme focuses on the unpredictability of financial markets and seeks to minimise the impact of exchange rate, interest rate and energy price fluctuations on the Group’s financial performance. The Group uses different derivative financial instruments to manage its exposure in these areas. All derivative financial instruments are employed solely for hedging purposes.

Financial risk management for Hong Kong operations is carried out by the Group’s central treasury department (Group Treasury) under policies approved by the Board of Directors or the Finance & General Committee of relevant Group entities. Overseas subsidiaries conduct their risk management activities in accordance with policies approved by their respective Boards. Group Treasury identifies, evaluates and monitors financial risks in close co-operation with the Group’s operating units. The Group has written policies covering specific areas, such as foreign exchange risk, interest rate risk, credit risk, use of derivative financial instruments and cash management.

Foreign exchange risk

The Group operates in the Asia-Pacific region and is exposed to foreign exchange risk arising from future commercial transactions, and from recognised assets and liabilities and net investments in foreign operations. This is primarily with respect to Australian dollar and Renminbi. Additionally, the Group has significant foreign currency obligations relating to its foreign currency denominated debts and major capital project payments, US dollar denominated nuclear power purchase offtake commitments and other fuel related payments. The Group uses forward contracts and currency swaps to manage its foreign exchange risk arising from future commercial transactions, and from recognised assets and liabilities which are denominated in a currency that is not the functional currency of the respective Group entity. Hedging is only considered for firm commitments and highly probable forecast transactions.

SoC Companies

Under the SoC, the SoC Companies are allowed to pass-through foreign exchange gains and losses arising from future non-capital projects related commercial transactions and recognised liabilities which are denominated in a currency other than Hong Kong dollar, thus retaining no significant foreign exchange risk of such payments over the long term. The SoC Companies use forward contracts and currency swaps to hedge all their debt repayment obligations denominated in foreign currencies for the full tenor, and a significant portion of their US dollar obligations on fuel and nuclear power purchases, provided that for US dollar the hedging can be accomplished at rates below the Hong Kong Government’s historical target peg rate of HK$7.8 : US$1. The objective is to reduce the potential impact of foreign exchange movement on electricity tariffs. The SoC Companies also use forward contracts to manage the foreign exchange risks arising from non-Hong Kong dollar payment obligations for major capital projects, for which the exchange gains and losses are capitalised.

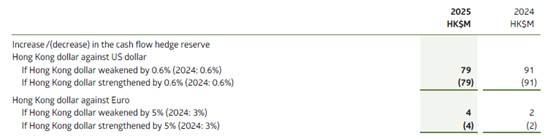

At the end of the reporting period, the fair value movement of the derivative financial instruments in a cash flow hedge relationship is recorded in equity. The extent of the impact to the cash flow hedge reserve under equity due to exchange rate movements, with all other variables held constant, is as follows:

The Group’s Asia-Pacific Investments

With respect to the power project investments in the Asia-Pacific region, the Group is exposed to both foreign currency translation and transaction risks.

The Group closely monitors translation risk using a Value-at-Risk (VaR) approach but does not hedge foreign currency translation risk because translation gains or losses do not affect the project company’s cash flow or the Group’s annual profit until an investment is sold. At 31 December 2025, the Group’s net investment subject to translation exposure was HK$44,113 million (2024: HK$43,150 million), arising mainly from our investments on the Chinese Mainland, Australia, India, and Taiwan Region and Southeast Asia. This means that, for each 1% (2024: 1%) average foreign currency movement, our translation exposure will vary by about HK$441 million (2024: HK$432 million). All the translation exposures are recognised in other comprehensive income and therefore have no impact on the profit or loss.

We consider that the non-functional currency transaction exposures at the individual project company level, if not managed properly, can lead to significant financial distress. Our primary risk mitigation is therefore to ensure that project-level debt financings are implemented on a local currency basis to the maximum extent possible. Each overseas subsidiary and project company has developed its own hedging programme into local currency taking into consideration any indexing provision in project agreements, tariff reset mechanisms, lender requirements, and tax and accounting implications.

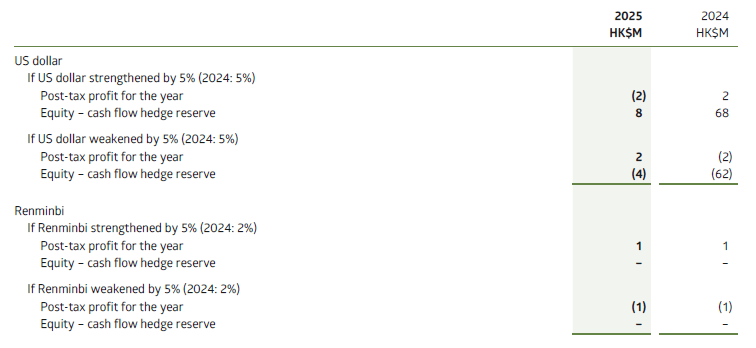

Most foreign currency exposures of the Group entities are hedged and / or their transactions are predominantly conducted through the functional currency of the respective entity. The following analysis presents the Group’s (apart from the SoC Companies) sensitivity to a reasonably possible change in the functional currencies of the Group entities against the US dollar and Renminbi, with all other variables held constant. The sensitivity rates in US dollar and Renminbi used are considered reasonable given the current level of exchange rates and the volatility observed in the different functional currencies of the Group entities. These are both on a historical basis and market expectations for future movement at the end of the reporting period and under the economic environments in which the Group operates. The extent of the impact to post-tax profit or equity due to exchange rate movements of US dollar and Renminbi against different functional currencies of Group entities, with all other variables held constant, is as follows:

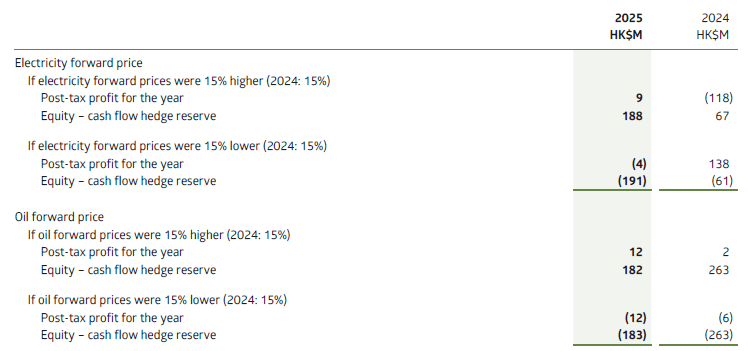

Energy portfolio risk

EnergyAustralia’s activity in energy markets exposes it to financial risk.

The electricity market is a competitive power pool. In this market generation supply and retail demand are exposed to spot (5-minute intervals) prices. EnergyAustralia purchases and sells majority of its electricity through the pool, at the same time EnergyAustralia enters into electricity spot-price-linked derivative financial instruments to manage the spot electricity price risk against forecast retail and generation exposures.

The gas market is a balancing market. To meet retail demand, EnergyAustralia procures gas supply agreements from various gas producers. The contract prices of certain agreements comprise a fixed component, and a variable component that is linked to oil spot prices on the global markets. EnergyAustralia enters into oil-price-linked derivative financial instruments to manage this oil price risk component.

Energy portfolio exposure is managed through an established risk management framework. The framework consists of policies which place appropriate limits on overall energy market exposures, hedging strategies and targets, delegations of authority on trading, approved product lists, regular exposure reporting, and segregation of duties. The corporate governance process also includes oversight by an Audit & Risk Committee (ARC-EA) which acts on behalf of EnergyAustralia’s Board.

At the end of the reporting period, the extent of the impact to the Group’s post-tax profits and other comprehensive income due to the change of the observable energy forward market prices is as follows:

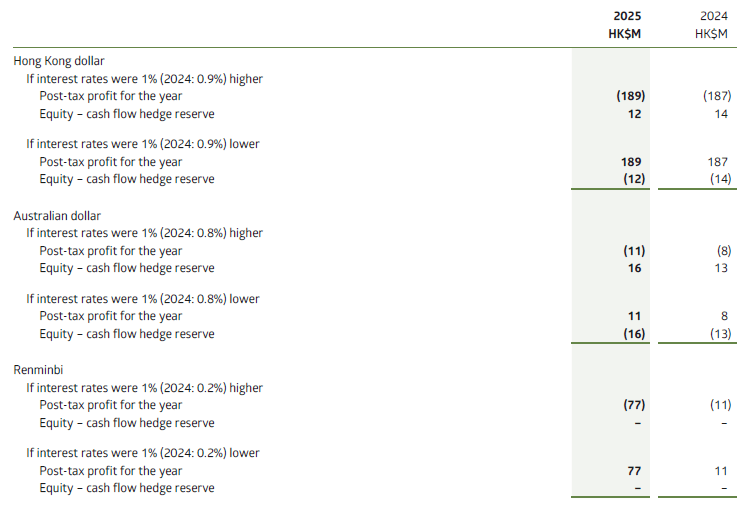

Interest rate risk

The Group’s interest rate risk arises from borrowings. Borrowings issued at variable rates expose the Group to cash flow interest rate risk, and borrowings issued at fixed rates expose the Group to fair value interest rate risk. The risks are managed by monitoring an appropriate mix between fixed and floating rate borrowings, and by the use of interest rate swaps.

The appropriate level of the fixed / floating mix is determined for each operating company subject to a regular review. For instance, SoC Companies conducts an annual review to determine a preferred fixed / floating interest rate mix appropriate for its business profile. Each overseas subsidiary and project company has developed its own hedging programme taking into consideration project debt service sensitivities to interest rate movements, lender requirements, tax and accounting implications.

The sensitivity analysis below presents the effects on the Group’s post-tax profit for the year (as a result of change in interest expense on floating rate borrowings) and equity (as a result of change in the fair value of derivative instruments which qualify as cash flow hedges). Such amounts accumulated in equity are reclassified to profit or loss in the periods when the hedged items affect profit or loss, and offset one another in the profit or loss.

The analysis has been determined based on the exposure to interest rates for both derivative and non-derivative financial instruments at the end of the reporting period. For floating rate borrowings, the analysis is prepared assuming the amount of liability outstanding at the end of the reporting period was outstanding for the whole year. The sensitivity to interest rates used is considered reasonable given the market forecasts available at the end of the reporting period and under the economic environments in which the Group operates, with all other variables held constant.

Financial Risk Management (extract 2)

2. Hedge Accounting

The Group seeks to apply, wherever possible, hedge accounting to present its financial statements in accordance with the economic purpose of the hedging activity. The Group determines the economic relationship between the hedged items and the hedging instruments by reviewing their critical terms. As a result, the Group concludes that the risk being hedged for the hedged items and the risk inherent in the hedging instruments are sufficiently aligned. There is no inherent mismatch in the hedging relationships. Certain ineffectiveness can arise during the hedging process. The main sources of hedge ineffectiveness are considered to be the effects of re-designation of the hedging relationships and the counterparty credit risks on the hedging instruments.

Hedges on debt related transactions

The Group applies various types of derivative financial instruments (forward foreign currency contracts, cross currency interest rate swaps and interest rate swaps) to mitigate exposures arising from the fluctuations in foreign currencies and / or interest rates of debt. In most of the cases, the hedging instruments have a one-to-one hedge ratio with the hedged items. In view of the nature of the hedging activities, no significant ineffectiveness is expected at inception.

Hedges on non-debt related transactions

The SoC Companies use forward contracts to manage its foreign exchange risk arising from fuel and nuclear purchases obligations, and payments for major capital projects. The SoC Companies hedge a high portion of committed and highly probable forecast transactions.

EnergyAustralia uses electricity spot-price-linked forward contracts and oil-price-linked forward contracts to mitigate exposures arising from the fluctuations in electricity spot price and oil spot price embedded in gas contracts. In most of the cases, the hedging instruments have a one-to-one hedge ratio with the hedged items.

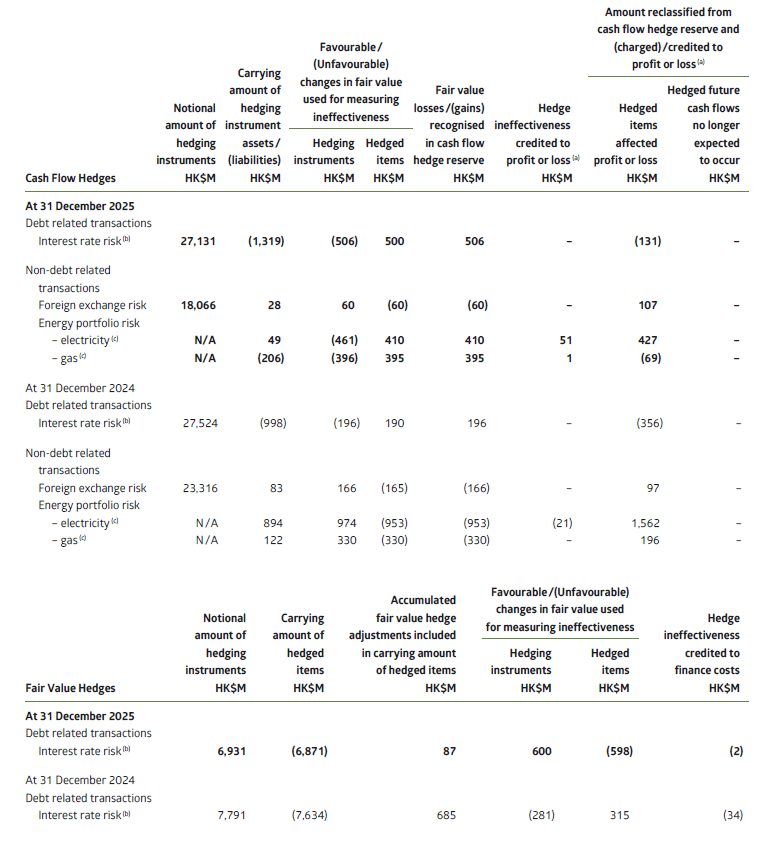

Effects of hedge accounting

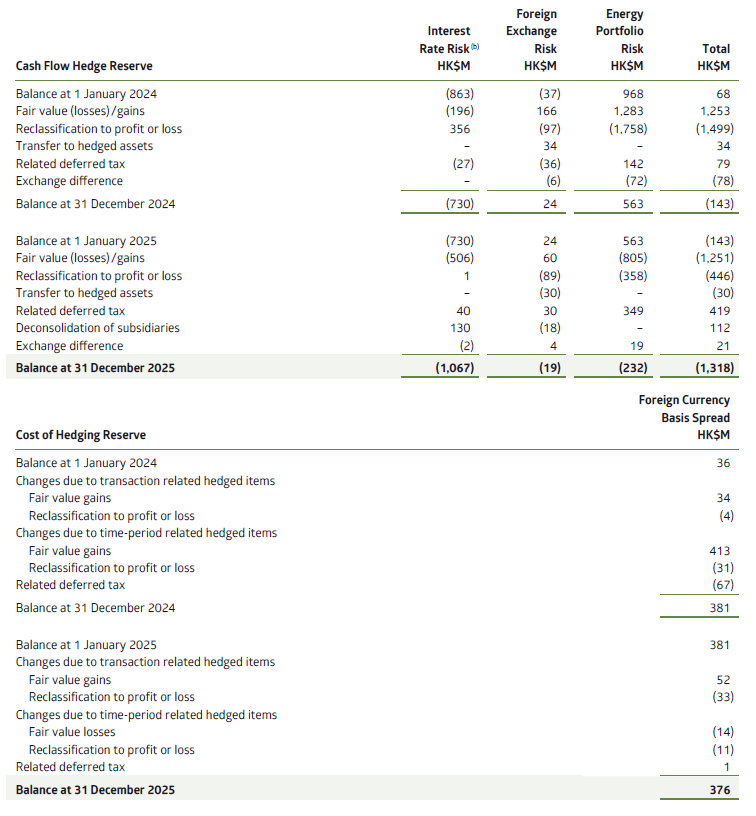

The tables below summarise the effect of the hedge accounting on financial position and performance of the Group for the year ended 31 December 2025 and 2024:

Notes:

(a) Hedge ineffectiveness and amounts reclassified from cash flow hedge reserve on non-debt and debt related transactions were recognised in fuel and other operating expenses and finance costs respectively.

(b) Interest rate risk included foreign exchange risk in case of foreign currency debts.

(c) The aggregate notional volumes of the outstanding energy derivatives were 40,250GWh (2024: 40,944GWh) for and 3.9 million barrels (2024: 4.4 million barrels) for electricity and oil respectively.

An analysis of other comprehensive income by risk category and the reconciliation of the components in equity that arises in connection with hedge accounting are as follows: