Nidec Corporation – Annual report – 31 March 2023

Industry: manufacturing

[Note there is no share of equity accounted associates and joint ventures in this example]

3. Significant accounting policies (extract)

(11) Financial instruments (extract)

FVTOCI financial assets

(a) FVTOCI debt financial assets

Financial assets are classified as FVTOCI debt financial assets if both of the following conditions are met:

- It is held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

- The contractual terms of the financial assets give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

A change in fair value of FVTOCI debt financial assets except for impairment gain or loss and foreign exchange gain or loss is recognized as other comprehensive income until derecognition. Upon derecognition the cumulative gain or loss previously recognized in other comprehensive income is reclassified to consolidated statement of income.

(b) FVTOCI equity financial assets

Upon initial recognition, NIDEC may make an irrevocable election to present changes in the fair value of an investment in equity financial assets that is not held for trading as other comprehensive income.

FVTOCI equity financial assets are measured at fair value after initial recognition, and its change in fair value is recognized as other comprehensive income, which is immediately transferred directly to retained earnings from other components of equity. It does not flow through consolidated statement of income. However, dividends from such investments are recognized in consolidated statement of income as part of financial income.

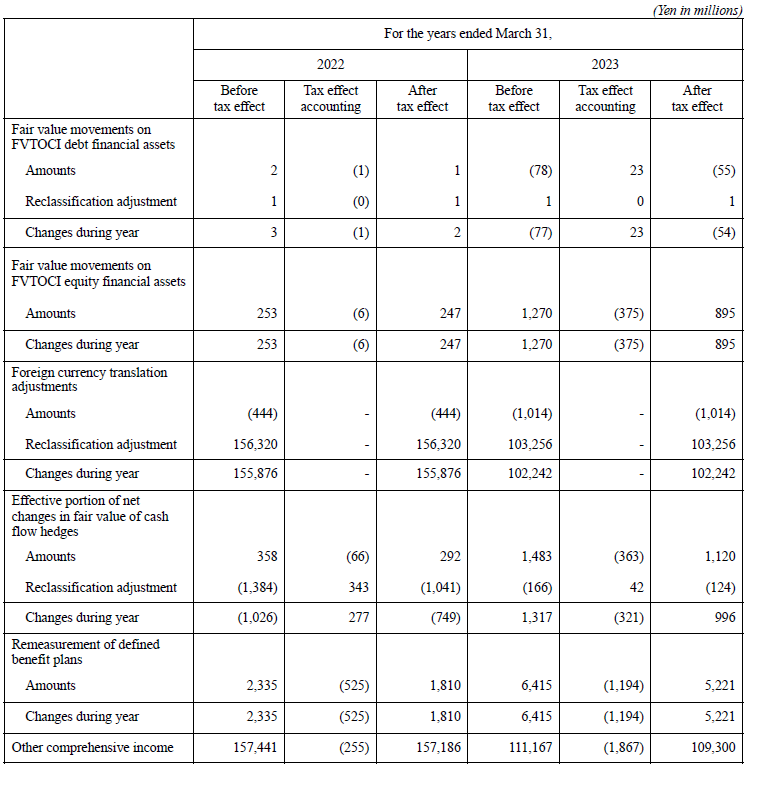

24. Other components of equity and other comprehensive income

The changes in other components of equity (net of tax) are as follows:

[Note: differences between the two tables represent NCI share]

The amounts of other comprehensive income including non-controlling interests, reclassification adjustment and tax effect accounting are as follows: