ROS AGRO PLC – Financial statements – 31 December 2023

Industry: agriculture

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEAR ENDED 31 DECEMBER 2023

(IN THOUSANDS OF RUSSIAN ROUBLES, UNLESS NOTED OTHERWISE)

2.2 Critical Accounting Estimates and Judgements in Applying Accounting Policies (extract)

Fair value of livestock and agricultural produce

The fair value less estimated point-of-sale costs of livestock at the end of each reporting period is determined using the physiological characteristics of the animals, management expectations concerning the potential productivity and market prices of animals with similar characteristics. The fair value of the Group’s bearer livestock is determined by using valuation techniques, as there were no observable market prices near the reporting date for pigs of the same physical conditions, such as weight and age. The fair value of the bearer livestock was determined based on the expected quantity of remaining farrows for pigs and the market prices of the young animals. The fair value of mature animals is determined based on the expected cash flow from the sale of the animals at the end of the production usage. The cash flow was calculated based on the actual prices of sales of culled animals from the Group’s entities to independent processing enterprises taking place near the reporting date, and the expected weight of the animals. Future cash flows were discounted to the reporting date at a current market-determined pre-tax rate. In the fair value calculation of the immature animals of bearer livestock management considered the expected culling rate.

Key inputs used in the fair value measurement of bearer livestock of the Group were as follows:

Should the key assumptions used in determination of fair value of bearer livestock have been 10% higher/lower with all other variables held constant, the fair value of the bearer livestock as at the reporting dates would be higher or lower by the following amounts:

The fair value of consumable livestock (pigs) is determined based on the market prices multiplied by the livestock weight at the end of each reporting period, adjusted for the expected culling rates. The average market price of consumable pigs being the key input used in the fair value measurement was 108.3 Russian Roubles per kilogram, excluding VAT, as at 31 December 2023 (31 December 2022: 98.5 Russian Roubles per kilogram, excluding VAT).

Should the market prices used in determination of fair value of consumable livestock have been 10% higher/lower with all other variables held constant, the fair value of the consumable livestock as at 31 December 2023 would be higher/lower by RR 565,856 (31 December 2022: RR 610,160).

The fair value less estimated point-of-sale costs for agricultural produce at the time of harvesting was calculated based on quantities of crops harvested and the prices on deals that took place in the region of location on or about the moment of harvesting and was adjusted for estimated point-of-sale costs at the time of harvesting.

The average market prices (Russian Roubles/tonne, excluding VAT) used for fair value measurement of harvested crops were as follows:

Should the market prices used in determination of fair value of harvested crops have been 10% higher/lower with all other variables held constant, the fair value of the crops harvested in 2023 would be higher/lower by RR 4,103,162 (2022: RR 2,911,137).

The fair value less estimated point-of-sale costs for unharvested crops are calculated based on expected yield, degree of readiness for each crop and the forward market prices.

The average forward market prices (Russian Roubles/tonne, excluding VAT) used for fair value measurement of unharvested crops were as follows:

Should the forward market prices used in determination of fair value of unharvested crops have been 10% higher/lower with all other variables held constant, the fair value of the unharvested crops as at 31 December 2023 would be higher/lower by RR 105,667 (2022: RR 87,868).

2. Summary of significant accounting policies (extract)

2.7 Biological assets and agricultural produce

Biological assets of the Group consist of unharvested crops (grain crops, sugar beets and other plant crops) and pigs livestock.

Livestock is measured at their fair value less estimated point-of-sale costs. Fair value at initial recognition is assumed to be approximated by the purchase price incurred. Point-of-sale costs include all costs that would be necessary to sell the assets. All the gains or losses arising from initial recognition of biological assets and from changes in fair-value-less-cost-to-sell of biological assets less the amounts of these gains or losses related to the realised biological assets are included in a separate line “Net gain/ (loss) on revaluation of biological assets and agricultural produce” above the gross profit line.

At the year-end unharvested crops are measured at fair value less estimated point-of-sale costs. A gain or loss from the changes in the fair value less estimated point-of-sale costs of unharvested crops less the amount of such gain or loss related to the realisation of agricultural products is included as a separate line “Net gain/ (loss) on revaluation of biological assets and agricultural produce” above the gross profit line.

Upon harvest, grain crops, sugar beets and other plant crops are included into inventory for further processing or for sale and are initially measured at their fair value less estimated point-of-sale costs at the time of harvesting. A gain or loss arising on initial recognition of agricultural produce at fair value less estimated point-of-sale costs of unharvested crops less the amount of such gain or loss related to the realisation of agricultural products is recognised in profit or loss in the period in which it arises.

Bearer livestock is classified as non-current assets; consumable livestock and unharvested crops are classified as current assets in the consolidated statement of financial position.

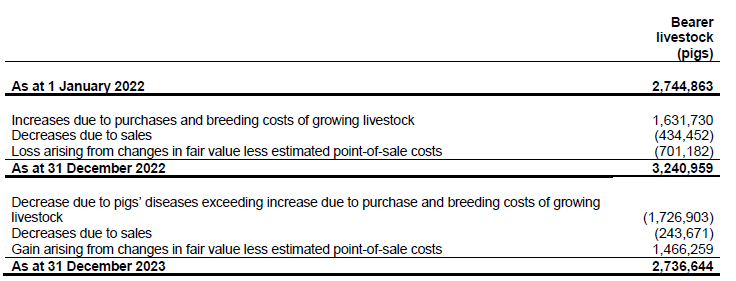

10. Biological assets

The fair value of biological assets belongs to level 3 measurements in the fair value hierarchy. Pricing model is used as a valuation technique for biological assets fair value measurement. There were no changes in the valuation technique during the years ended 31 December 2023 and 2022. The reconciliation of changes in biological assets between the beginning and the end of the year can be presented as follows:

Short-term biological assets

Long-term biological assets

In 2023 the aggregate gain on initial recognition of agricultural produce and from the change in fair value less estimated point-of-sale costs of biological assets amounted to RR 15,783,478 (2022: RR 3,191,157).

Included in the above amounts there are losses related to realised biological assets and agricultural produce amounting to RR 12,084,785 (2022: loss RR 11,733,592).

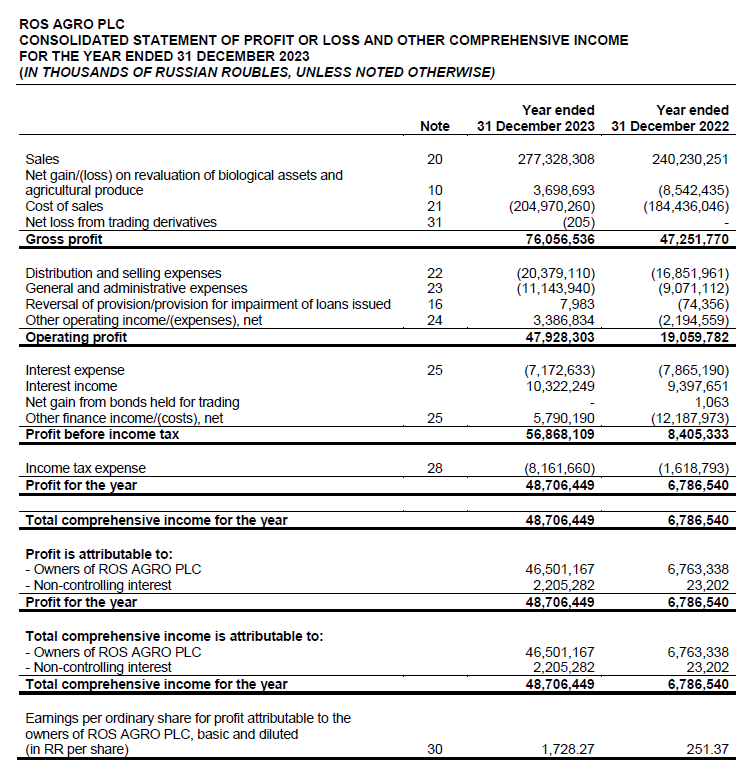

The amount of net gain/ (loss) on revaluation of biological assets and agricultural produce was recognized in the consolidated statement of profit or loss and other comprehensive income in 2023 in the amount of RR 3,698,693 (2022: loss RR 8,542,435), which includes the aggregate gain on initial recognition of agricultural produce in the amount RR 15,783,478 (2022: RR 3,191,157) less losses related to realised biological assets and agricultural produce in the amount of RR 12,084,785 (2022: loss RR 11,733,592).

Livestock population were as follows:

In 2023 total area of arable land amounted to 597 thousand ha (2022: 567 thousand ha).

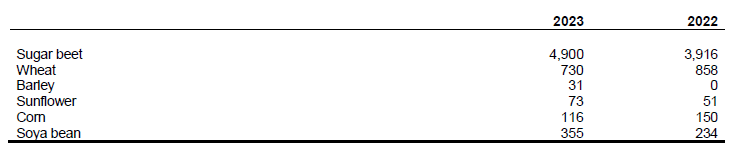

The main crops of the Group’s agricultural production and output were as follows (in thousands of tonnes):

Key inputs in the fair value measurement of the livestock and the agricultural crops harvested together with sensitivity to reasonably possible changes in those inputs are disclosed in Note 2.2.

As at 31 December 2023 biological assets with a carrying value of RR 2,137,344 (2022: RR 421,903) were pledged as collateral for the Group’s borrowings (Note 16).

The Group is exposed to financial risks arising from changes in meat and crops prices. The Group does not anticipate that crops and meat prices will decline significantly in the foreseeable future except some seasonal fluctuations and, therefore, has not entered into derivative or other contracts to manage the risk of a decline in respective prices. The Group reviews its outlook for meat and crops prices regularly in considering the need for active financial risk management.

19. Government grants

During 2022-2023 the Group received government grants from the Tambov and Belgorod regional governments and the Federal government in form of partial compensation of the investments into acquisition of equipment for agricultural business and sugar processing and the investments into reconstruction and modernisation of the pig-breeding farms and the slaughter house. The receipts of these grants in 2023 amounted to RR 576,649 (2022: RR 317,097). These grants are deferred and amortised on a straight-line basis over the expected lives of the related assets.

In 2022-2023 the Group obtained government grants for reimbursement of interest expenses on bank loans received for construction of the pig-breeding farms in the Far East and Tambov. The government grants related to interest expenses capitalised into the carrying value of assets, were similarly deferred and amortised on a straight-line basis over the expected lives of the related assets. The deferred government grants, related to capitalised interest expense, amounted to RR 1,680,110 (2022: RR 2,184,110).

The movements in deferred government grants in the consolidated statement of financial position were as follows:

Other bank loan interests, which had been refunded by the state, were credited to the consolidated statement of profit or loss and other comprehensive income and netted with the interest expense (Note 25).

Other government grants received are included in Note 24.

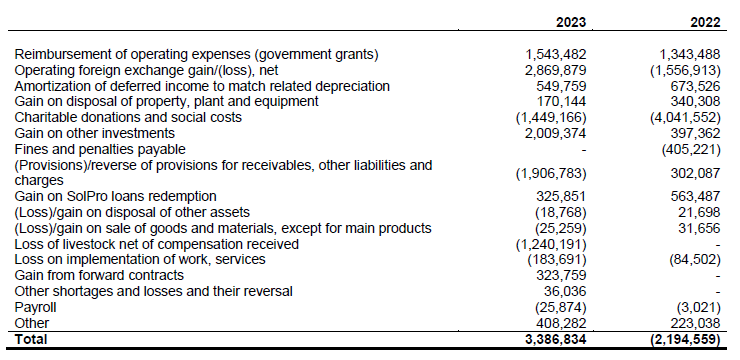

24. Other operating income/(expenses), net

Gain on other investments in 2023 is comprised of dividends received from LLC GK Agro-Belogorie in the amount of RR 2,009,374 (2022: RR 397,362).

32. Financial risk management (extract)

Market risk (extract)

Sales price risk

Changes in white sugar prices are closely related to changes in world raw sugar prices. The storage facilities of own sugar plants permit to build up stocks of white sugar to defer sales to more favourable price periods.

The Group is exposed to financial risks arising from changes in meat and crops prices (Note 10).