International Consolidated Airlines Group, S.A. – Annual report – 31 December 2025

Industry: airline

34 Employee benefit obligations (extract)

c Fair value of scheme assets

i Investment strategies

For both APS and NAPS, the Trustee has ultimate responsibility for decision-making on investment matters, including the asset-liability matching strategy. The latter is a form of investing designed to match the movement in pension plan assets with the movement in the projected benefit obligation over time. The Trustees’ investment committee adopts an annual business plan which sets out investment objectives and work required to support achievement of these objectives. The committee also deals with the monitoring of performance and activities, including work on developing the strategic benchmark to improve the risk return profile of the scheme where possible, as well as having a trigger-based dynamic governance process to be able to take advantage of opportunities as they arise. The investment committee reviews the existing investment restrictions, performance benchmarks and targets, as well as continuing to develop the de-risking and liability hedging portfolio.

Both schemes use derivative instruments for investment purposes and to manage exposures to financial risks, such as interest rate, foreign exchange, longevity and liquidity risks arising in the normal course of business. Exposure to interest rate risk is managed through the use of inflation-linked swap contracts. Foreign exchange forward contracts are entered into to mitigate the risk of currency fluctuations. Longevity risk is managed through the use of buy-in insurance contracts, asset swaps and longevity swaps.

Along with existing contracts with Rothesay Life (as detailed in note 34c(iii)) and following the completion of a further longevity swap in 2024, APS is 100% protected against all longevity risk and fully protected in relation to all pensions that were already being paid as at 31 March 2018. APS is nearly 90% protected against interest rates and inflation (on a Retail Price Index (RPI) basis). NAPS is 95% protected against interest rates and inflation (on a Consumer Price Index (CPI) basis).

The assets held by APS and NAPS are split between ‘return-seeking assets’ and ‘liability-matching assets’ depending on the maturity of each scheme. At 31 December 2025, the actual asset allocation for NAPS was 17% (2024: 20%) in return seeking assets and 83% (2024: 80%) in liability matching investments. For NAPS, the Trustee agreed an updated investment framework with British Airways as part of the Scheme’s 31 March 2021 actuarial valuation agreement. The Trustee aims towards an overall asset allocation with an agreed modest expected return relative to liabilities and sufficient liquidity to manage investment risk appropriately on an ongoing basis. The actual asset allocation for APS at 31 December 2025 was 1% (2024: 1%) in return seeking assets and 99% (2024: 99%) in liability matching investments. NAPS uses Liability Driven Investments (LDIs) to effectively hedge volatility in the scheme liabilities. This is achieved through direct bond holdings as opposed to the use of derivatives and, as such, leverage is low. Accordingly, as at 31 December 2025, NAPS has not been required to raise additional cash or liquidate existing assets in order to fund derivative positions.

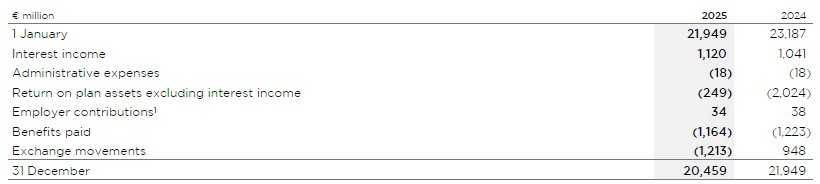

ii Movement in scheme assets

A reconciliation of the opening and closing balances of the fair value of scheme assets is set out below:

1 There were no employer contributions to APS or NAPS in 2025 (2024: €1 million contribution to APS).

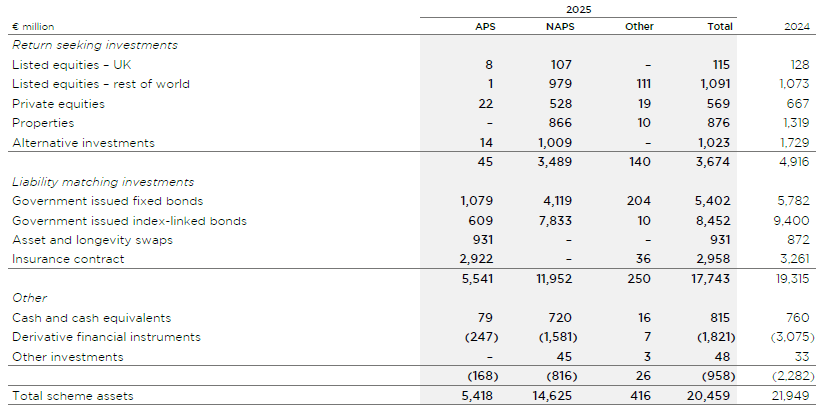

iii Composition of scheme assets

Scheme assets held by the Group at 31 December comprise:

The fair values of the Group’s scheme assets, which are not derived from quoted prices on active markets, are determined depending on the nature of the inputs used in determining the fair values (see note 30b for further details) and using the following methods and assumptions:

- Private equities are valued at fair value based on the most recent transaction price or third-party net asset, revenue or earnings-based valuations that generally result in the use of significant unobservable inputs. The dates of these valuations typically precede the balance sheet date and have been adjusted for any cash movements between the date of the valuation and the balance sheet date. Typically, the valuation approach and inputs for these investments are not updated through to the balance sheet date unless there are indications of significant market movements.

- Properties are valued based on an analysis of recent market transactions supported by market knowledge derived from third-party professional valuers that generally result in the use of significant unobservable inputs.

- Alternative investments fair values, which predominantly include holdings in investment and infrastructure funds, are determined based on the most recent available valuations applying the Net Asset Value methodology and issued by fund administrators or investment managers and adjusted for any cash movements having occurred from the date of the valuation to the balance sheet date. Typically, the valuation approach and inputs for these investments are not updated through to the balance sheet date unless there are indications of significant market movements.

- Other investments predominantly include: interest receivable on bonds; dividends from listed and private equities that have been declared but not received at the balance sheet date; receivables from the sale of assets for which the proceeds have not been collected at the balance sheet date; and payables for the purchase of assets which have not been settled at the balance sheet date.

- Derivative financial instruments are entered into predominantly to mitigate interest rate and inflation rate risks. These derivative financial instruments are stated at their fair value using pricing models and relevant market data as at the balance sheet date.

- Asset and longevity swaps – APS has a contract with Rothesay Life, entered into in 2010 and extended in 2013, which covers 25% (2024: 25%) of the pensioner liabilities for an agreed list of members. Under the contract, to reduce the risk of long-term longevity risk, Rothesay Life makes benefit payments monthly in respect of the agreed list of members in return for the contractual return receivable on a portfolio of assets (made up of quoted government debt) held by the scheme and the contractual payments made by APS to Rothesay Life on the longevity swaps. The Group holds the portfolio of assets at their fair value, with the government debt held at their quoted market price and the swaps accounted for at their estimated discounted future cash flows.

During 2011, APS entered into a longevity swap with Rothesay Life, which covers an additional 21% (2024: 21%) of the pensioner liabilities for the same agreed list of members as the 2010 contract. Under the longevity swap, to reduce the risk of long-term longevity risk, APS makes a fixed payment to Rothesay Life each month reflecting the prevailing mortality assumptions at the inception of the contract, and Rothesay Life makes a monthly payment to APS reflecting the actual monthly benefit payments to members. The cash flows are settled net each month. If pensioners live longer than expected at inception of the longevity swap, Rothesay Life will make payments to the scheme to offset the additional cost of paying pensioners and if pensioners do not live as long as expected, then the scheme will make payments to Rothesay Life. The Group holds the longevity swap at fair value, determined at the estimated discounted future cash flows.

During 2024, APS entered into a longevity swap with Zurich Assurance Ltd to transfer longevity risk in relation to an additional 7% (2024: 7%) of the scheme’s liabilities. Under the longevity swap, to remove the risk of long-term longevity risk, APS makes monthly fixed payments to Zurich Assurance Ltd reflecting the prevailing mortality assumptions at the inception of the contract, and Zurich Assurance Ltd makes a monthly payment to APS reflecting the actual monthly benefit payments to members. If pensioners live longer than expected at inception of the longevity swap, Zurich Assurance Ltd will make payments to the scheme to offset the additional cost of paying pensioners and if pensioners do not live as long as expected, then the scheme will make payments to Zurich Assurance Ltd. The Group holds the longevity swap at fair value, determined at the estimated discounted future cash flows.

- Insurance contract – during 2018, the Trustee of APS secured a buy-in contract with Legal & General. The buy-in contract covers all members in receipt of pensions from APS at 31 March 2018, excluding dependent children, receiving a pension at that date and members in receipt of equivalent pension only benefits, who were alive on 1 October 2018. Benefits coming into payment for retirements after 31 March 2018 are not covered. The contract covers benefits payable from 1 October 2018 onwards. The policy covers approximately 60% of all benefits APS expects to pay out in future.