Nippon Telegraph and Telephone Corporation – Annual report – 31 March 2019

Industry: telecoms

2. Basis of Preparation (extract)

(1) Matters Regarding Compliance with and First-Time Adoption of IFRS

NTT Group meets the requirements of a “Specified Company complying with Designated International Accounting Standards” pursuant to Article 1-2 of the “Order on the Terminology, Forms, and Preparation Methods of Consolidated Financial Statements” (Ordinance of the Ministry of Finance No. 28 of 1976) (the “Order on Consolidated Financial Statements”). Consequently, in accordance with Article 93 of the Order on Consolidated Financial Statements, the Group has prepared the consolidated financial statements pursuant to International Financial Reporting Standards (“IFRS”). The consolidated financial statements were approved by the President and Chief Executive Officer Jun Sawada and Senior Executive Vice President and Chief Financial Officer Akira Shimada on June 26, 2019.

NTT Group has applied IFRS from the current fiscal year ended March 31, 2019 (from April 1, 2018 to March 31, 2019), with the date of transition to IFRS being April 1, 2017. In connection with the transition to IFRS, the Group has applied IFRS 1 “First-time Adoption of International Financial Reporting Standards.” Please see “Note 37. First-Time Adoption of IFRS” for details regarding the impact of the transition to IFRS on the Group’s financial position, results of operation, and cash flows. NTT Group’s accounting policies conform to IFRS as in effect as of March 31, 2019, with the exception of IFRS provisions that have not been early adopted and exemptions allowed under IFRS 1.

37. First-time Adoption of International Financial Reporting Standards (“IFRS”)

(1) Transition to Financial Reporting in Accordance with IFRS

NTT Group prepared the consolidated financial statements for the fiscal year ended March 31, 2019 as its first IFRS financial statements.

According to IFRS 1, an entity applying IFRS for the first time must apply it retrospectively. However, retrospective application is exceptionally prohibited for certain standards under IFRS 1, for which IFRS is applied prospectively from the date of transition to IFRS. Additionally, certain exemptions under IFRS 1 may be voluntarily applied to a part of the standards required to be applied under IFRS. The effect of applying these provisions has been recognized at the IFRS transition date in retained earnings or “Other components of equity.”

The major voluntary exemptions stipulated in IFRS 1 and applied by NTT Group are described below.

(ⅰ) Business combinations

NTT Group has not applied IFRS 3 retrospectively to business combinations that arose before April 1, 2002. Goodwill resulting from business combinations that arose before April 1, 2002 has been recognized at the carrying amount based on U.S. GAAP. For goodwill generated in business combinations that occurred before the date of transition to IFRS, impairment testing was implemented as of the date of transition to IFRS, regardless of whether there was any indication of impairment.

(ⅱ) Deemed cost

For certain items of property, plant and equipment and investment property, NTT Group uses the fair value as of the date of transition to IFRS as deemed cost, which is a surrogate for cost at that date.

(ⅲ) Operating revenues

NTT Group has retrospectively applied IFRS 15 using the practical expedient set out in (d) under paragraph C5 of IFRS 15. In accordance with the provisions of the standard, information related to the date of transition to IFRS and the fiscal year ended March 31, 2018 is omitted for the amounts of consideration for goods or services to be provided from the next fiscal year and the explanation of when these amounts are expected to be recognized as revenue.

(ⅳ) Exemptions from restatement of comparative information in the application of IFRS 9

At the date of transition to IFRS and for the fiscal year ended March 31, 2018, items included within the scope of application of IFRS 9 have been restated in accordance with IFRS 9. These are recognized and measured in accordance with the previous accounting standards (U.S. GAAP).

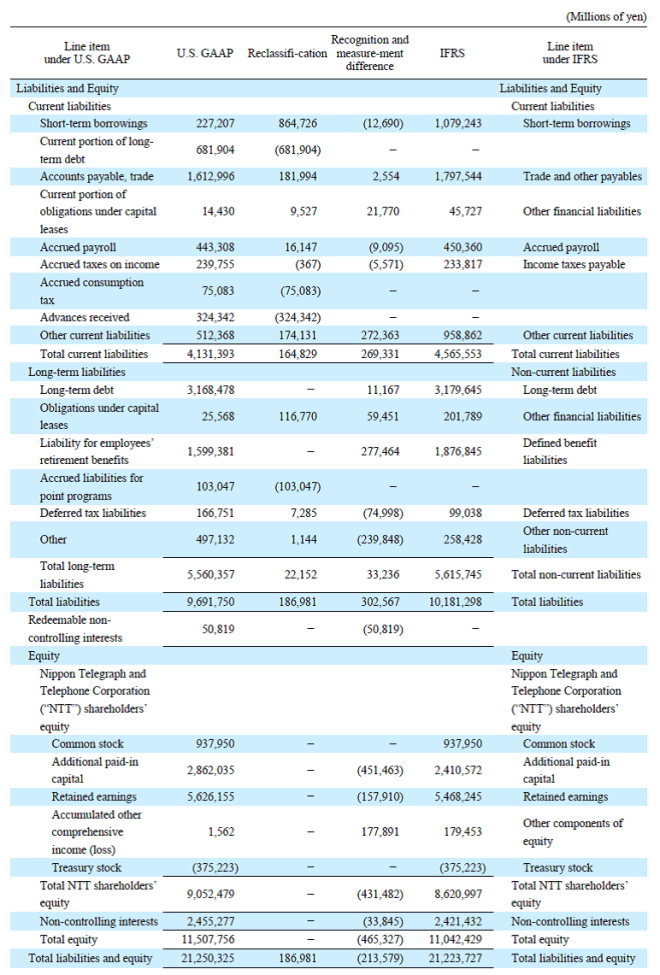

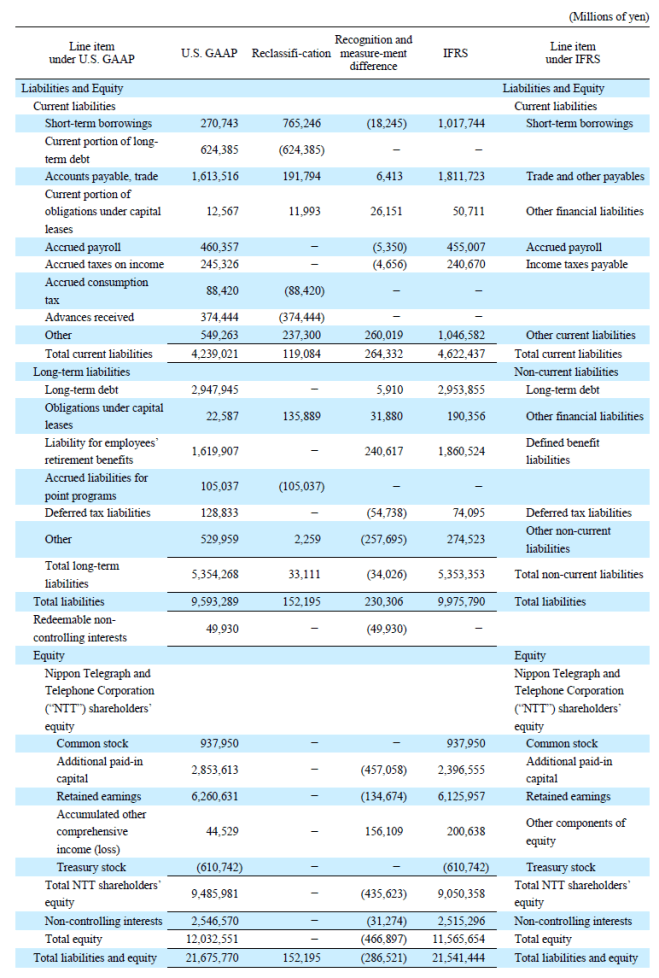

(2) Reconciliations from U.S. GAAP to IFRS

Upon transition to IFRS, NTT Group has adjusted the amounts in the consolidated financial statements that were prepared based on U.S. GAAP. The impact of transition from U.S. GAAP to IFRS on the Group’s financial position, results of operations, and cash flows is explained in the following reconciliation tables and the notes to these tables.

In the reconciliation tables, “Reclassification” shows those items that have no impact on equity and comprehensive income, and “Recognition and measurement difference” shows those items that have an impact on equity and comprehensive income.

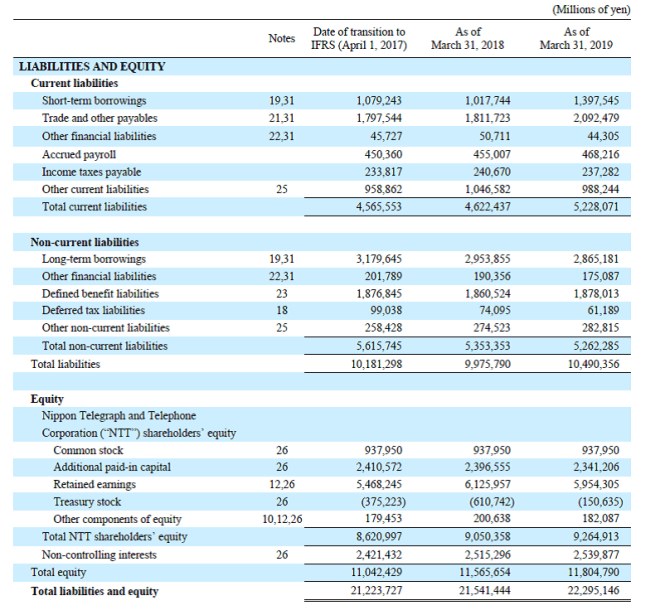

Reconciliation of equity at the date of transition to IFRS (April 1, 2017)

Consolidated statement of financial position

Reconciliation of equity as of March 31, 2018

Consolidated statement of financial position

Reconciliation of comprehensive income for the fiscal year ended March 31, 2018 (April 1, 2017 to March 31, 2018)

Consolidated statement of profit or loss

Consolidated statement of comprehensive income

(3) Notes on Adjustments to Equity and Comprehensive Income

(ⅰ) Impairment on non-financial assets

As the methods of implementing impairment tests for goodwill differ between U.S. GAAP and IFRS, a difference emerges in the amounts recognized as impairment losses. The main difference is the implementation unit of impairment tests.

Under U.S. GAAP, impairment tests for goodwill are required to be performed for each reporting unit (business segment or the constituent unit one level lower than business segments), whereas under IFRS impairment tests are required to be conducted for each cash-generating unit or group of cash-generating units. When transitioning to IFRS, NTT Group divided certain reporting units into several cash-generating units.

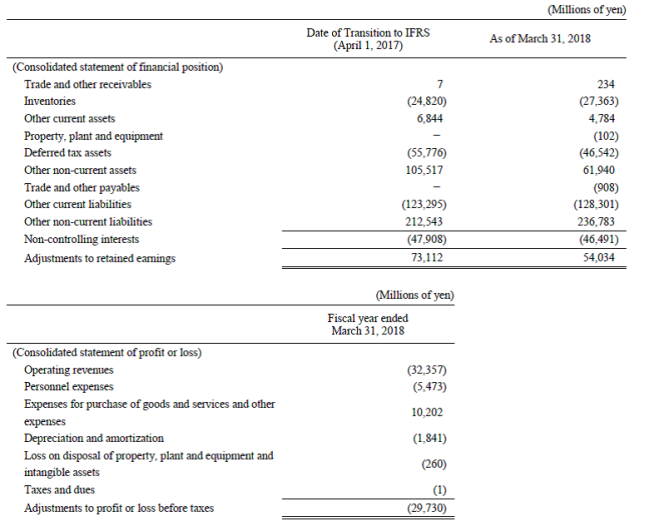

For goodwill, an impairment test was implemented as of the date of transition to IFRS, regardless of whether there was any indication of impairment. As a result, impairment losses were recognized for cash-generating units of System Integration-MEA and Internet Solutions of Dimension Data belonging mainly to the Long distance and international communications business segment. All impairment losses were ¥26,231 million and allocated to goodwill. The recoverable amounts of these cash-generating units are fair value less costs of disposal, which are measured by the discount cash flow method and the guideline public company method using unobservable inputs. The assumptions (inputs) used to measure fair value defined in “Note 3. Significant Accounting Policies (5) Fair Value” are classified as Level 3.

The impact of this change is as follows.

Impairment losses, recoverable amounts, and main assumptions used to estimate the recoverable amounts

(ⅱ) Capitalization of development expenses

Of the research and development expenditures that were recorded as expenses under U.S. GAAP, part of the development expenses meet the capitalization requirements under IFRS. These are recognized as assets in the consolidated statement of financial position and amortized using the straight-line method over the estimated useful lives.

The impact of this change is as follows.

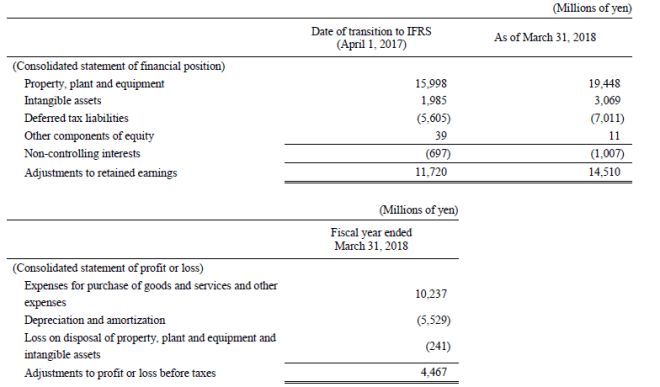

(ⅲ) Deemed cost

In applying IFRS, NTT Group has applied the exemptions stipulated in IFRS 1, and used the fair value of certain property, plant and equipment and investment property as of the date of transition to IFRS as their deemed cost.

At the date of transition to IFRS, the previous carrying amount and the fair value of “property, plant and equipment” and “investment property” using the deemed cost stood at ¥525,178 million and ¥413,281 million, respectively.

As a result of the above, at the date of transition to IFRS, “property, plant and equipment” and “investment property” decreased by ¥66,353 million and ¥45,544 million, respectively. The net difference of this adjustment, after deducting the ¥34,789 million adjustment for deferred taxes, is included in “retained earnings” for ¥55,450 million and “non-controlling interests” for ¥21,658 million.

(ⅳ) Revenues

With regard to costs incurred to provide communications services in the Mobile communications business, Regional communications business, Long distance and international communications business, and sales commissions and other charges were previously capitalized and amortized over the estimated average period of the subscription term under U.S. GAAP, up to the amount of income from non-recurring upfront fees such as installation fees and activation fees. However, under IFRS, because the full amount of these costs will be capitalized regardless of the upper limit of non-recurring upfront fees, part of the sales commissions and other charges that were previously accounted for as expenses will be additionally recognized as assets. In addition, an allowance was recognized for points earned by customers depending on their service usage under U.S. GAAP. However, under IFRS, part of the transaction consideration is recognized as contract liabilities when the points are granted, and revenue is recognized when the points are used.

In the Mobile communications business, income from non-recurring upfront fees, such as activation fees, is deferred. These were recognized as revenues by type of service over the average expected period of subscription under U.S. GAAP. Under IFRS, these will be recognized over the period of providing the “Monthly Support” service.

As for contracts for which it is difficult to make a reasonable estimate on the progress of the construction work, revenue is recognized upon completion of the contract services under U.S. GAAP. On the other hand, under IFRS, revenue is recognized within the range of the costs incurred.

The impact of these changes is as follows.

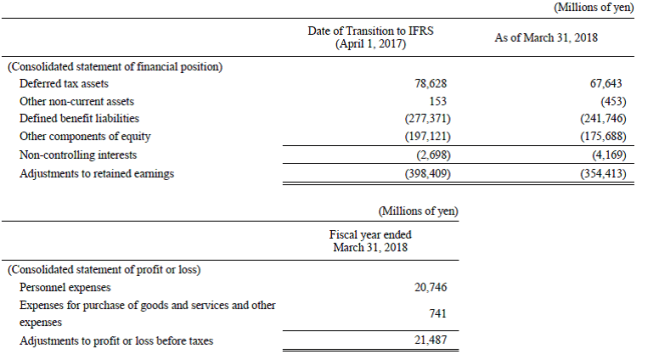

(ⅴ) Employee benefits

Under U.S. GAAP, service cost, interest cost, and expected return on plan assets associated with post-retirement benefits under the defined benefit plans were recognized in profit or loss. Of the actuarial gains or losses and prior service cost arising from the defined benefit plans, those that were not recognized as components of retirement benefit expenses for the current period are recognized as “Other components of equity” and subsequently recognized in profit or loss over a certain future period.

On the other hand, under IFRS, current service cost and past service cost under the defined benefit plans are recognized in profit or loss, while interest cost is recognized in profit or loss at an amount calculated by multiplying the net defined benefit liabilities and assets by discount rates. Remeasurements of the net defined benefit liabilities and assets, such as actuarial gains or losses, are recognized in other comprehensive income, which, when incurred, is transferred directly from “other components of equity” to retained earnings, without being recognized in profit or loss.

NTT Special Accounting Fund for the NTT CDBP is a public welfare pension plan and is considered a multi-employer plan. Therefore, contributions to the fund are recognized as expenses under U.S. GAAP. On the other hand, under IFRS, although the scheme is a public welfare pension scheme, it is considered a defined benefit plan. Accordingly, the defined benefit obligations are recognized at present value in the consolidated statement of financial position as “defined benefit liabilities.”

The impact of these changes is as follows.

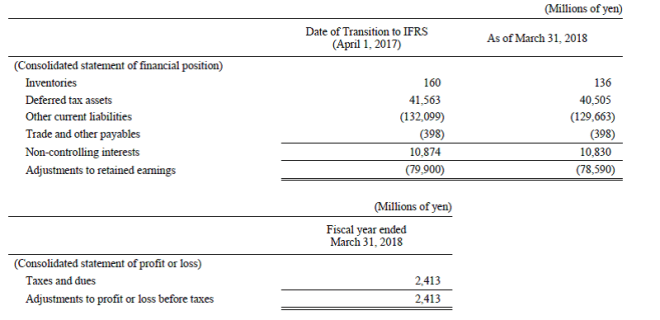

(ⅵ) Levies

Under U.S. GAAP, levies payable such as real estate taxes are were expensed over the relevant accounting periods. Under IFRS, however, these are recognized as an expense in its entirety at the time when payment obligation arises.

The impact of this changes are as follows.

(ⅶ) Business combinations

Under U.S. GAAP, with regard to the acquisition of non-controlling interests in subsidiaries that occurred before March 31, 2009, the cost was allocated to identifiable assets acquired and liabilities assumed, which were measured based on an estimated fair value, with the excess of the cost over the net assets acquired recognized as “goodwill.” With regard to individual investments acquired in stages, the accounting method described above is applied, and the cumulative amount of the costs is then reflected. Under IFRS, changes in the parent’s ownership interest in a subsidiary that do not result in a loss of the parent’s control over the subsidiary are accounted for as capital transactions. Individual investments acquired in stages are remeasured at a fair value on the acquisition date when the parent acquires control over the subsidiary.

In addition, under U.S. GAAP, the non-controlling interest in the acquired company is measured at a fair value at the time of business combination. On the other hand, under IFRS, the non-controlling interest in the acquired company at the time of business combination can be measured, for each business combination transaction, at fair value or by proportional share in the acquired company’s identifiable net assets.

The impact of these changes is as follows.

(ⅷ) Income taxes

Under U.S. GAAP, with regard to taxable temporary differences pertaining to investments in domestic subsidiaries, the tax law provides a means by which the reported amount of the investment can be recovered free of tax. Except for the cases where the Company expects to ultimately use the means, deferred tax liabilities are recognized. On the other hand, under IFRS, when it is probable that the temporary differences will not be reversed in a foreseeable future, deferred tax liabilities for taxable temporary differences pertaining to investments in subsidiaries are not recognized.

In addition, under U.S. GAAP, deferred tax liabilities recognized for taxable temporary differences pertaining to investments in affiliates are measured based on the amount of future reversal of the taxable temporary differences resulting from the sale of investments. On the other hand, under IFRS, the deferred tax liabilities recognized for future taxable temporary differences pertaining to investments in affiliates are measured based on the most probable amount of future reversal, such as the distribution of dividends.

The impact of these changes is as follows. The impact on consolidated statements of profit or loss is immaterial and omitted.

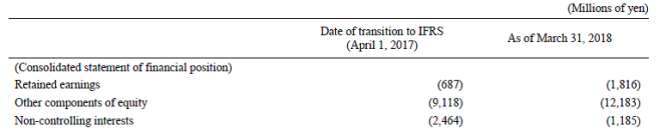

(ⅸ) Put options granted to non-controlling interests

With regard to short put options on subsidiary shares granted to the holders of certain non-controlling interests, redemption of the non-controlling interests is not solely in the control of NTT Group. Under U.S. GAAP, the estimated redemption amount was recorded as “Redeemable non-controlling interests” and presented in between liabilities and equity in the consolidated balance sheets. Changes in the estimated redemption amount were reflected to “retained earnings.”

On the other hand, under IFRS, the present value of the redemption amount of these options is, in principle, initially recognized as “other financial liabilities,” and an equivalent amount is deducted from an additional paid-in capital. These are subsequently measured at an amortized cost using the effective interest rate method, with the subsequent changes recognized as additional paid-in capital.

The impact of this change is as follows.

The main adjustments to equity and comprehensive income other than (ⅰ) to (ⅸ) above are as follows.

Under U.S. GAAP, when the fiscal year-end date of a subsidiary or an investment accounted for using the equity method differs from that of the parent company, material events or transactions occurring during the period of the different year-end dates are disclosed in the notes or adjusted in the consolidated financial statements.

Under IFRS, when the fiscal year-end date of a subsidiary or an associate and joint venture differs from that of the parent company, the fiscal year-end date is unified, or additional financial statements are prepared as of the parent company’s fiscal year-end date, unless impractical. If unifying the fiscal year-end dates or preparing additional financial statements is impractical, an adjustment is made for the material events or transactions occurring during the period of the different year-end dates.

The impact of this change is as follows.

(4) Note on Changes in Presentation of Consolidated Statement of Financial Position and Consolidated Statement of Profit or Loss

(ⅰ) Presentation of deferred tax assets and deferred tax liabilities

Under U.S. GAAP, “deferred tax assets” and “deferred tax liabilities” at the date of transition to IFRS (April 1, 2017) are presented as current assets and current liabilities, and non-current assets and non-current liabilities. Under IFRS, all deferred tax assets and deferred tax liabilities are presented as non-current assets and non-current liabilities. At the end of the fiscal year ended March 31, 2018, there was no difference in this presentation requirement between U.S. GAAP and IFRS.

(ⅱ) Classification of financial assets and financial liabilities

Under IFRS, “other financial assets” and “other financial liabilities” are presented separately, based on the requirements of presentation.

(ⅲ) Offsetting of financial assets and financial liabilities

Under U.S. GAAP, financial assets are offset against financial liabilities for presentation provided that certain requirements are met, even if the right to offset is conditional. On the other hand, under IFRS, financial assets are not offset against financial liabilities, except when an unconditional and legally enforceable right to offset exists at the end of the reporting period, and the Group aims to either settle on a net basis or realize the asset and settle the liability simultaneously.

(ⅳ) Presentation of operating expenses

Under U.S. GAAP, operating expenses are presented using the function of expense method, whereby expenses are classified as cost of sales, selling expenses, and other categories of expenses based on their function. Under IFRS, expenses are presented using the nature of expense method, whereby expenses are classified as “personnel expenses,” “expenses for purchase of goods and services and other expenses,” “depreciation and amortization,” and other categories of expenses based on their nature.

(5) Adjustments to Consolidated Statement of Cash Flows

The impact of the change from U.S. GAAP to IFRS in the consolidated statement of cash flows is as follows.

The key adjustments are the following two points:

(ⅰ) Under U.S. GAAP, cash flows related to loans and the collection of loans are recorded under cash flows from investing activities. Under IFRS, however, cash flows related to loans and collection of loans that are related to principal operating activities are recorded under cash flows from operating activities. The impact of this change is as follows.

(ⅱ) Under IFRS, in connection with the change in the consolidated statement of financial position described in (4) (ⅲ) above, Short-term borrowings, and cash and cash equivalents, for which offsetting presentation is not permitted are presented. The impact of this change is as follows.