Nikon Corporation – Annual report – 31 March 2025

Industry: manufacturing

3. Material Accounting Policy Information (extract)

(4) Financial Instruments (extract)

1) Non-derivative Financial Assets (extract)

(iii) Impairment of financial assets measured at amortized cost

Allowance for doubtful accounts in respect of financial assets measured at amortized cost is recognized for expected credit losses.

At the end of each reporting period, the Group evaluates whether there has been a significant increase in credit risk of a financial asset since initial recognition. Specifically, if the credit risk of a financial asset has not significantly increased since initial recognition, an allowance for doubtful account is measured at an amount equal to the 12-month expected credit losses. However, if the credit risk has significantly increased since initial recognition, it is measured at an amount equal to the expected credit losses over the remaining term of the financial asset. An allowance for doubtful account for trade receivables without any significant financing components is measured at an amount equal to the lifetime expected credit losses since initial recognition.

Whether the credit risk has significantly increased or not depends on changes in default risk. The following factors are considered to determine if there has been a change in default risk:

- Financial condition of debtors

- Actual credit losses occurred in prior years

- Overdue information in prior years

Provision or reversal of allowance for doubtful accounts is recognized in profit or loss as “Selling, general and administrative expenses” in the consolidated statement of profit or loss.

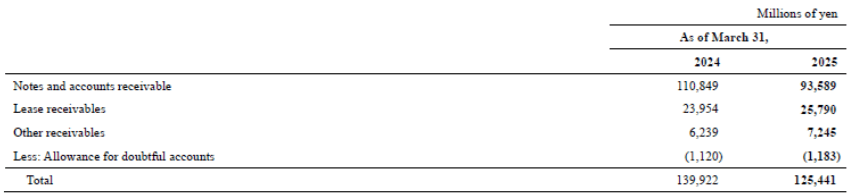

9. Trade and Other Receivables

The breakdown of trade and other receivables is as follows:

Note: Trade and other receivables are classified as financial assets measured at amortized cost.

As for allowance for doubtful accounts, please see (5) Credit Risk Management in Note 35. Financial Instruments.

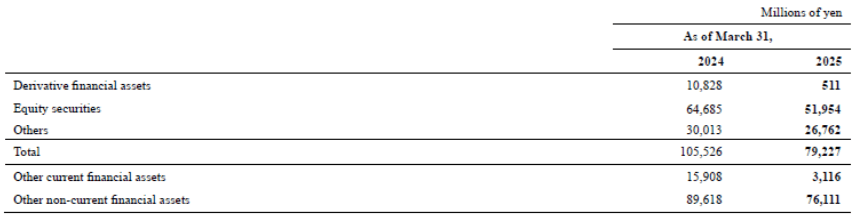

11. Other Financial Assets (extract)

(1) Breakdown

The breakdown of other financial assets is as follows:

As for the classification of financial assets, please see (2) Classification of Financial Instruments in Note 35. Financial Instruments.

Derivative financial assets other than those applying hedging accounting are classified as financial assets measured at fair value through profit or loss. Equity securities are mainly classified as financial assets measured at fair value through other comprehensive income.

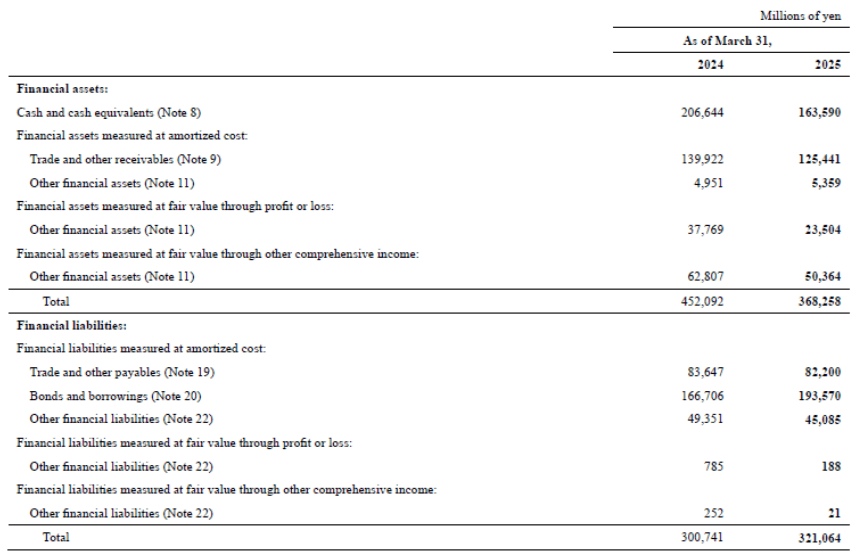

35. Financial Instruments (extract)

(2) Classification of Financial Instruments

Financial instruments are classified as follows:

(5) Credit Risk Management

The Group is exposed to credit risk (i.e., the risk that a counterparty will default on its contractual obligations of a financial asset held by the Group, resulting in a financial loss to the Group) arising from trade and other receivables, including notes receivable, accounts receivable, lease receivables, and other receivables.

Trade receivables, including notes and accounts receivable and lease receivables, are exposed to customer credit risk. With respect to this risk, the Group manages the due dates and account balances of each customer in accordance with the Group’s policies concerning settlement conditions, and it also obtains information about doubtful accounts that are mainly caused by deterioration in the financial conditions of customers at an early stage, in addition to accepting advances and utilizing transaction credit insurance according to the nature of transaction contents, trade size, and the creditworthiness of customers so as to mitigate credit risk.

Other receivables are also exposed to the credit risk of counterparties, but they are generally settled in a short period.

- Derivatives are exposed to credit risk arising from default by counterparties. With respect to the execution and management of derivative transactions, the Group operates the transactions according to internal policies for trade authorization and enters into derivative transactions only with highly rated financial institutions to mitigate credit risk.

The carrying amount of the financial assets after deducting impairment losses as presented in the consolidated financial statements represents the Group’s maximum exposure to credit risk without considering the valuation of the related collateral obtained.

(i) Credit Risk Exposure with Respect to Trade and Other Receivables

The Group’s credit risk exposure with respect to trade and other receivables is as follows:

Regarding trade and other receivables, allowance for doubtful accounts is recognized and measured based on future expected credit losses, taking into account the recoverability and a significant increase in credit risk. The Group assesses and determines whether credit risk has significantly increased based on changes in the debtor’s default risk, which is based on the debtor’s financial condition and historical records of actual credit loss and past due. Allowance for doubtful accounts associated with trade receivables is always measured at lifetime expected credit losses. Further, lifetime expected credit losses may be estimated individually or collectively. Although lifetime expected credit losses are measured collectively, if one or more of the following events adversely affect the estimated future cash flows of trade receivables, an expected credit loss of the trade receivables is measured individually as an impairment of credit of trade receivables:

- Significant financial difficulties of debtors

- Contractual breach including default or delinquencies

- The increase in the possibility of bankruptcy or other financial restructuring of debtors

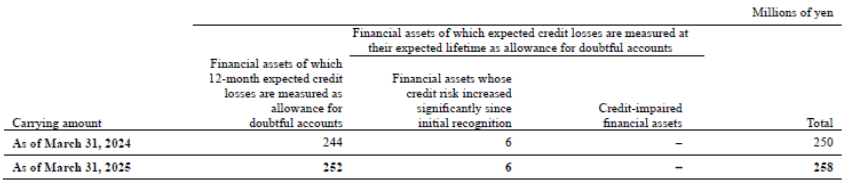

Trade and other receivables

The financial assets above mainly include notes and accounts receivable and lease receivables.

Other receivables are financial assets of which allowance for doubtful accounts are measured based on 12-month expected credit losses. The balances of other receivables as of March 31, 2024 and 2025 were ¥3,180 million and ¥3,855 million, respectively.

Other financial assets

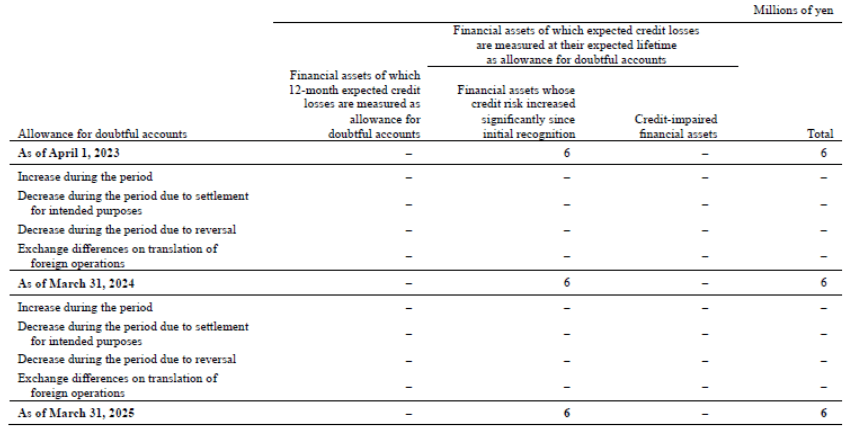

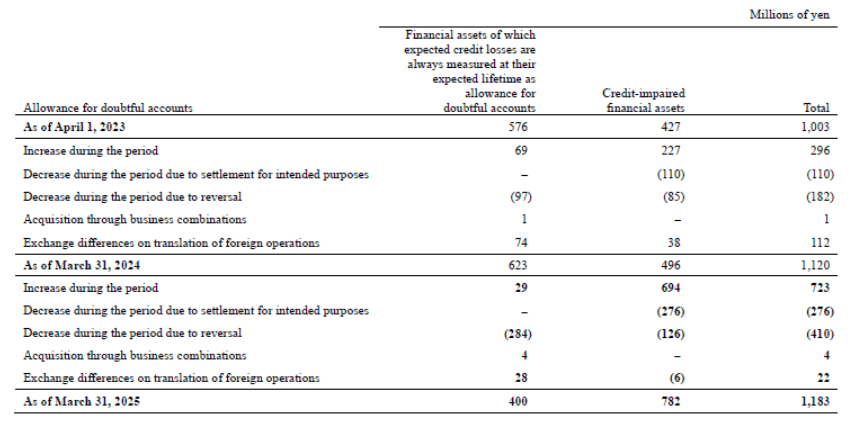

(ii) Analysis of Allowance for Doubtful Accounts

The Group accounts for the impairment of financial assets through allowance for doubtful accounts rather than writing off the carrying amount of the assets. Changes in the allowance for doubtful accounts are as follows:

Trade and other receivables

The allowance for doubtful accounts above is mainly related to notes and accounts receivable and lease receivables.

There was no allowance for doubtful accounts of other receivables as of March 31, 2024 and 2025.

Other financial assets