SimCorp A/S – Annual report – 31 December 2021

Industry: computer software

2.1 Revenue

Revenue types

Revenue is mainly derived from license fees from new clients, license fees from additional sales to existing clients, software updates and support fees, professional services, and hosting and other fees.

License fees can be derived from subscription or from perpetual license agreements. Subscription agreements give the right to use the software for a determined period of time, which can be extended at the end of the initial term. Standard perpetual software licenses provide clients with the right to use the software whilst the software updates and support contract remains in force. License fees also include revenue from Client Driven Development agreements and standard platform offerings.

Software updates and support fees relate to contracts made on perpetual and subscription-based license terms. Software updates and support fees include both initial license and additional license-based software updates and support fees. Performance obligations include: unspecified future upgrades, maintenance and helpline support.

Professional services agreements can include multiple performance obligations. The performance obligations are: implementation services, validation and testing services, SimCorp Dimension on-boarding and operating services. SCDaaS operating services occur when, in addition to hosting, SimCorp undertakes the operation of the client’s system in a cloud-based environment.

The hosting offering provides the client with the infrastructure required to operate SimCorp Dimension. Other fees include, for instance, training and education as well as third party products and software as service fees.

Accounting policies, judgments and estimates

Contract Identification

Contracts can include several components, in this situation, the total contract sum is allocated to the separate performance obligations for the purpose of revenue recognition.

Separate contracts with the same client are treated as one contract if entered into at or near the same time and economically interrelated. Contracts closed more than 6 months apart are not considered to be entered at the same time.

In determining whether the various contracts are interrelated judgment is required. Considerations include: whether the contracts were negotiated as a package with a single commercial objective, whether the amount of consideration on one contract is dependent on the performance of another contract, or if some or all offerings in the contract are a single performance obligation.

Additional agreements with existing clients can be a new contract or a modification to existing contracts. Judgments making this determination consider: the presence of a connection between the new agreement and pre-existing contracts, whether subscription fees, license fees, software updates and support fees or services under the new agreement are highly interrelated with the subscription fees, license fees and software updates and support fees or services sold under prior agreements, and how the subscription fees, license fees and software updates and support fees or services under the new agreement are priced. Conversion of perpetual license agreement to a subscription based license agreement is accounted for as a termination of the perpetual license agreement and a new subscription license agreement

Performance obligation identification

Contracts often include several components. License fees from new clients, license fees from additional sales to existing clients, software updates and support fees, professional services, hosting, training, Datacare, Coric, Digital Portal, IAaaS, other services, and third-party products constitute the main performance obligations. The fees allocated to the different performance obligations are recognized separately.

The only performance obligation related to license agreements has been identified as the right to use the software. The right to use software license is considered a separate performance obligation when it satisfies the following conditions: can be delivered separately from other services, can be installed by a third party, can be used without upgrades, and is functional without upgrades or technical support.

Judgment is required in determining whether a component is considered a separate performance obligation, in particular, professional services and implementation activities. Consideration is given as to whether the services significantly integrate, customize or modify the software or hosting offering. In general, implementation services and activities go beyond setup and qualify as a separate performance obligation.

Options to acquire additional components such as renewals or additional volumes require judgment in determining whether such options provide a material right to the client which the client would not receive without entering into that contract. In this judgment it is considered whether the options entitle the customer to a discount that exceeds the discount granted for the respective subscriptions fees, license fees, software updates and support fees sold with the option.

Transaction price

Estimate is applied in determining the amount to which SimCorp expects to be entitled in exchange for transferring licenses, and software updates and support to a customer.

The consideration attributable to license fees in subscription-based agreements are discounted to net present value when the value of the financing element is deemed significant. If the period between licenses transfer, software updates and support and payment from the clients is a year or less no financing component is recognized.

A hierarchy has been established to identify the standalone selling prices used to allocate the transaction price of a customer contract to the performance obligations in the contract.

Where standalone selling prices for a performance obligation are observable and reasonably consistent across customers, estimates are derived from SimCorp’s pricing history. Using this approach, professional services stand-alone value is determined based on the hourly billing rate for the relevant market unit. Hosting services are assumed to be quoted to the client at their stand-alone value if it is equal to or above hosting costs.

Where sales prices are not directly observable or are highly variable across customers, estimation techniques are applied, such as a cost-plus-margin approach. This approach is often applied to third party products.

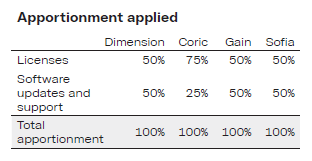

If not renewable, with highly variable pricing, and no substantial direct costs to estimate based on a cost-plus margin approach, allocation is achieved by applying a residual approach. We use this technique in particular for license and software updates and support.

Once the standalone price for other components is estimated, an apportionment is applied to allocate the price between license and software updates and support after deducting other performance obligations from the total consideration as follows:

Revenue recognition

Revenue recognition requires an agreement with the client which creates enforceable rights and obligations between the parties, has commercial substance, and identifies payment terms. In addition, it must be probable that the consideration determined in the contract will be collected.

Revenue is recognized when the client has obtained control of the license or service and has the ability to use and obtain substantially all the benefits from the license or service.

SimCorp has therefore assessed that the client obtains control of the license when all the following criteria are met: a binding contract is entered into; the license is delivered; and the client has the right to use it. License revenue is therefore generally recognized at that point-in-time.

When the contract contains functionality gaps or requires client acceptance of functionality, the revenue recognition will be deferred until the time of delivery or acceptance. The consideration attributable to license fee in subscription-based agreements is discounted to net present value when the value of the financing element is deemed significant.

Revenue from software updates and support agreements is recognized on a straight-line basis over the contract period.

Client-driven development entails direct cooperation between SimCorp’s development team and the client for a client-defined software. Such agreements are individually evaluated to determine if revenue is recognized at a point in time or over time.

Professional services fees are recognized based on work performed for time and material contracts. Fixed fee agreements are recognized based on percentage of completion unless client acceptance is required.

The percentage-of-completion method requires estimation of total revenue and the stage of completion. The assumptions, estimates, and uncertainties inherent in determining the stage of completion affect the timing and amounts of revenue recognized.

Changes in estimates of progress towards completion and of contract revenue and costs are accounted for as cumulative catch-up adjustments to the reported revenue for the applicable contract.

Software as a Service (SaaS), such as on-boarding and operating services, hosting fees, Datacare, Coric Digital Portal, Regulatory Reporting Platform (RRP), and Investment Accounting Services (IAS), are revenue recognized over the term of the service.

Where SimCorp stands ready to provide the service (such as access to e-learning and hosting operating services) revenue is recognized based on time elapsed – ratably over the period applicable. Judgment is applied in determining which method to use.

All the judgments and estimates mentioned above can significantly impact the timing and amount of revenue to be recognized.

The geographical distribution of revenue is based on the country in which the client is invoiced. Significant countries are defined as countries representing 5.0% or more of the Group’s revenue. None of the reported licenses – initial sales is derived from perpetual sales (2020: EUR 0.0).

From the reported licenses – additional sales EUR 23.9m is derived from perpetual sales (2020: EUR 18.8m). The Group has no client contributing revenue of more than 4.0% (2020: 5.5%) of total revenue.

2.3 Future performance obligations

The amount of a customer contract’s transaction price that is allocated to the remaining performance obligations represents contracted revenue that has not yet been recognized. Including amounts recognized as contract liabilities and amounts that are contracted but not yet delivered.

The transaction price allocated to performance obligations that are unsatisfied or partially unsatisfied as of December 31, 2021 is EUR 554.8m (2020: EUR 405.6m). This amount mostly comprises obligations to provide software updates, agreements which require client acceptance of functionality, and support or hosting subscriptions and support, as the respective contracts typically have durations of multiple years.

Management expects that EUR 141.3m in 2021 (2020: EUR 113.3m) of the amount allocated to the future performance obligations as of December 31, 2021 will be recognized during 2022. EUR 342.3m (2020: EUR 228.6m) is expected to be recognized as revenue within 2 to 5 years. The remaining part is expected to be recognized as revenue after 5 years. The Group applies the practical expedient in paragraph 121 of IFRS 15 and does not disclose information about remaining performance obligations that have original expected durations of one year or less.

Accounting estimates and judgments

This estimation is judgmental, as it needs to consider estimates of possible future contract modifications and the timing of satisfaction of performance obligations. The amount of transaction price allocated to the remaining performance obligations, and changes in this amount over time, are impacted by, among others, currency fluctuations and possible contract modifications.

Under the percentage-of-completion method used for fixed fee services agreements, recognition of profit is dependent upon the accuracy of a variety of estimates. Such estimates are based on various judgments with respect to multiple factors and are difficult to accurately determine until the project is significantly underway. Due to uncertainties inherent in the estimation process, it is possible that the actual timing of completion may vary from estimates.

2.4 Contract balances

Contract balances consist of client-related assets and liabilities.

Contract assets

Contract assets relate to the Group’s rights to consideration for software licensed to clients under subscription agreements with future payments, when that right is conditional on SimCorp’s future performance.

If the timing of payments specified in the contract provides the client with a significant financing benefit, the transaction price is adjusted to reflect this financing component.

Contract assets increased by EUR 45.1m with subscription-based licenses adding EUR 84.8m (2020: EUR 67.3m) and finance income recognized EUR 2.0m (2020: EUR 2.3m). Foreign exchange as well as adjustments also had a positive impact partly off-set by deduction of expected credit loss provision with overall positive impact of EUR 8.6m (2020: EUR -7.3m). The overall balance was reduced by invoiced subscription-based license fees of EUR 50.3m (2020: EUR 37.9m).

Contract liabilities

When a client pays consideration in advance, or an amount of consideration is due contractually before transferring of the license or service, then the amount received in advance is presented as a liability. Contract liabilities represent mainly prepayments from clients for unsatisfied or partially satisfied performance obligations in relation to licenses, software updates and support, and services. Software updates and support and hosting billing generally occurs at periodic intervals (e.g. quarterly or yearly) prior to revenue recognition, resulting in liabilities.

The majority of license agreements are recognized as revenue in the year of sale. However, contracts with functionality gaps or acceptance criteria may have revenue recognition deferred, resulting in a contract liability when payment has occurred.

Contracts in progress relating to fixed fee professional services are measured at the estimated sales value of the proportion of the contract completed at the statement of financial position date.

Periodic fixed fees for subscription services, software updates and support services, and other multiperiod agreements are typically invoiced yearly or quarterly in advance. Such fee prepayments account for the majority of our contract liability balance. Fees based on actual transaction volumes for SCDaaS subscriptions and fees charged for non-periodical services are invoiced as the services are delivered. While payment terms and conditions vary by contract type and region, our terms typically require payment within 30 to 60 days.

Accounting policies, judgments and estimates

Amounts invoiced on account in excess of work completed are included in prepayments under current liabilities.

Contract assets from contracts with customers are measured at amortized cost less expected credit losses. Contract assets are within the scope of impairment requirements in IFRS 9.

For contract assets the simplified approach is used, and the expected loss provision is measured at the estimate of the lifetime expected credit losses.

Expected loss rates between 0.03% – 14.13% are applied (2020: 0.04% – 13.36%), based on average default rates by region as published by Standard & Poor. For additional information refer to note 6.2 Risk.

Judgment is required in determining whether a right to consideration is conditional and thus qualifies as contract assets. Estimates are made as to whether and to what extent subsequent concessions or payments may be granted to customers and whether the customer is expected to pay the contractual fees. In this judgment, trading history is considered both with the respective customer and more broadly.

Incremental Costs of Obtaining Customer Contracts

The Group expenses the incremental costs of obtaining a customer contract as incurred. The incremental costs of obtaining a customer contract primarily consist of sales commissions earned by the sales force. Commissions are typically related to the license fee which is recognized upfront upon delivery, consequently, we expense sales commissions concurrently with revenue recognition.

Costs to Fulfill Customer Contracts

The Group does not capitalize costs incurred to fulfil customer contracts. Direct costs for custom development and standard platform are expensed as incurred.