Rio Tinto plc – Annual report – 31 December 2025

Industry: mining

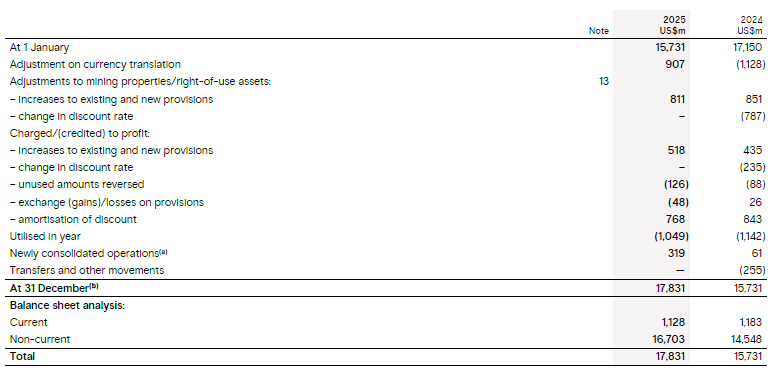

14 Close-down, restoration and environmental provisions

Recognition and measurement

The Group has provisions for close-down and restoration costs, which include the dismantling and demolition of infrastructure, the removal of residual materials, and the remediation of disturbed areas for mines and certain refineries and smelters. The obligation may arise during development or during the production phase of a facility. These provisions are based on all regulatory requirements and any other commitments made to stakeholders. The provision excludes the impact of future disturbance that is planned to occur during the life of mine, so that it represents only existing disturbance as at the balance sheet date.

Closure provisions are not made for those operations that have no known restrictions on their lives as the closure dates cannot be reliably estimated; instead a contingent liability is disclosed. Refer to note 37 for details. This applies primarily to certain Canadian smelters that have indefinite-lived water rights from local governments permitting electricity generation from hydropower stations and are not tied to a specific orebody.

Close-down and restoration costs are a normal consequence of mining or production, and the majority of close-down and restoration expenditure is incurred in the years following closure of the mine, refinery or smelter. Although the ultimate cost to be incurred is uncertain, the Group’s businesses estimate their costs using current restoration standards, techniques and expected climate conditions. The costs are estimated on the basis of a closure plan, and are reviewed at each reporting period during the life of the operation to reflect known developments. The estimates are also subject to formal review, with appropriate external support, at regular intervals.

The timing of closure and the rehabilitation plans for the site can be uncertain and dependent upon future capital allocation decisions, which involve estimation of future economic circumstances and business cases. In such circumstances, the closure provision is estimated using probability weighting of the different remediation and closure scenarios.

The initial close-down and restoration provision is capitalised within “Property, plant and equipment”. Subsequent movements in the close-down and restoration provisions for ongoing operations are treated as an adjustment to cost within “Property, plant and equipment”. This includes those resulting from new disturbances related to expansions or other activities qualifying for capitalisation; updated cost estimates; changes to the estimated lives of operations; changes to the timing of closure activities; and revisions to discount rates.

Changes in closure provisions relating to closed and fully impaired operations are charged/(credited) to “Net operating costs” in the income statement.

Where rehabilitation is conducted systematically over the life of the operation, rather than at the time of closure, provision is made for the estimated outstanding continuous rehabilitation work at each balance sheet date and the cost is charged to the income statement.

The closure provision is represented by forecast future underlying cash flows expressed in real terms at the balance sheet date. These are discounted for the time value of money based on a long-term view of low-risk market yields which includes a review of historic trends plus risks and opportunities for which future cash flows have not been adjusted, namely potential improvements in closure practices between the reporting date and the point at which rehabilitation spend takes place. The real-terms discount rate used is 2.5% (2024: 2.5%) which is applied to all locations since we expect to meet closure cash flows principally from US dollar revenues and financing, with activities coordinated by the Group’s central closure team.

To roll forward those real-terms cash flows between periods, we identify local rates of inflation based on Producer Price Inflation (PPI) indices and, together with the real-terms discount rate, unwind the discount through the line “Amortisation of discount on provisions”, shown within “Finance items” in the income statement. This nominal rate for cost escalation in the current financial year is estimated at the start of each half-year and applied systematically for 6 months. At the end of each half year we update the underlying cash flows for the latest estimate of experienced inflation, if it differs materially from our forecast, for the current financial year and record this as “changes to existing provisions”. For operating sites this adjustment usually results in a corresponding adjustment to property, plant and equipment, and for closed and fully impaired sites the adjustment is charged or credited to the income statement.

In some cases, our subsidiaries make a contribution to trust funds in order to meet or reimburse future environmental and decommissioning costs. Amounts due for reimbursement from trust funds are not offset against the corresponding closure provision unless payments into the fund have the effect of passing the closure obligation to the trust.

Environmental costs result from environmental damage that was not a necessary consequence of operations, and may include remediation, compensation and penalties. Provision is made for the estimated present value of such costs at the balance sheet date. These costs are charged to “Net operating costs”, except for the unwinding of the discount which is shown within “Amortisation of discount on provisions”.

Remediation procedures may commence soon after the time the disturbance, remediation process and estimated remediation costs become known, but can continue for many years depending on the nature of the disturbance and the remediation techniques used.

(a) In 2025, this relates to our acquisition of Arcadium Lithium plc. Refer to note 5 for details. In 2024, this relates to our acquisition of an additional 20.64% interest in NZAS.

(b) Close-down, restoration and environmental provisions at 31 December 2025 have not been adjusted for closure-related receivables amounting to US$394 million (2024: US$350 million) due from the ERA trust fund and other financial assets held for the purposes of meeting closure obligations. These are included within “Receivables and other assets” on the balance sheet.

Key judgement Close-down, restoration and environmental obligations

We use our judgement and experience to determine the potential scope of closure rehabilitation work required to meet the Group’s legal, statutory and constructive obligations, and any other commitments made to stakeholders, and the options and techniques available to meet those obligations in order to estimate the associated costs and the likely timing of those costs. Significant judgement is also required to then determine both the costs associated with that work and the other assumptions used to calculate the provision. External experts support the cost estimation process where appropriate, but there remains significant estimation uncertainty.

The key judgement in applying this accounting policy is determining when an estimate is sufficiently reliable to make or adjust a closure provision. Adjustments are made to provisions when the range of possible outcomes becomes sufficiently narrow to permit reliable estimation. Depending on the materiality of the change, adjustments may require review and endorsement by the Group’s Closure Steering Committee before the provision is updated.

Cost provisions are updated throughout the life of the operation with conceptual study estimates reviewed every 5 years. Within 10 years from the expected closure date, closure cost estimates must comply with the Group’s Capital Project Framework. This means, for example, that where an Order of Magnitude (OoM) study is required for closure, it must be of the same standard as an OoM study for a new mine, smelter or refinery.

In some cases, the closure study may indicate that monitoring and, potentially, remediation will be required indefinitely – for example, groundwater treatment. In these cases, the underlying cash flows for the provision may be restricted to a period for which the costs can be reliably estimated, which on average is around 30 years. Where an alternative commercial arrangement to meet our obligations can be predicted with confidence, this period may be shorter.

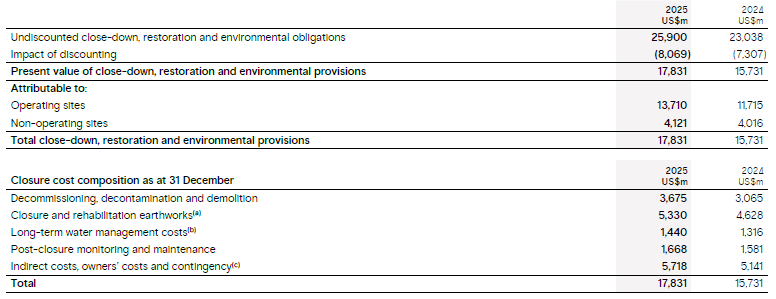

Analysis of close-down, restoration and environmental provisions

(a) A key component of earthworks rehabilitation involves re-landscaping the area disturbed by mining activities utilising largely diesel-powered heavy mobile equipment. In developing low-carbon solutions for our mobile fleet, this may include electrification of the vehicles during the mine life. The forecast cash flows for the heavy mobile equipment in the closure cost estimate are based on existing fuel sources. The cost incurred during closure could reduce if these activities are powered by renewable energy.

(b) Long-term water management relates to the post-closure treatment of water due to acid rock drainage and other environmental commitments and is an area of research and development focus for our Closure team. The cost of this water processing can continue for many years after the bulk earthworks and demolition activities have completed and are therefore exposed to long-term climate change. This could materially affect rates of precipitation and therefore change the volume of water requiring processing. It is not currently possible to forecast accurately the impact this could have on the closure provision as some of our locations could experience drier conditions whereas others could experience greater rainfall. A further consideration relates to the alternative commercial use for the processed water, which could support ultimate transfer of these costs to a third party.

(c) Indirect costs, owners’ costs and contingency include adjustments to the underlying cash flows to align the closure provision with a central-case estimate. This excludes allowances for quantitative estimation uncertainties, which are allocated to the underlying cost driver and presented within the respective cost categories above.

The geographic composition of the closure provision shows that our closure obligations are largely in countries with established levels of regulation in respect of mine and site closure.

Projected cash flows (undiscounted) for close-down, restoration and environmental provisions

Remaining lives of operations and infrastructure range from 1 to over 50 years with an average for all sites, weighted by undiscounted present closure obligation, of around 15 years. Although the ultimate cost to be incurred is uncertain, the Group’s businesses estimate their respective costs based on current restoration standards, techniques and expected climate conditions.

Key accounting estimate Close-down, restoration and environmental obligations

The most significant assumptions and estimates used in calculating the provision are:

- Closure timeframes. The weighted average remaining lives of operations is shown above. Some expenditure may be incurred before closure while the operation as a whole is in production.

- The length of any post-closure monitoring period. This will depend on the specific site requirements and the availability of alternative commercial arrangements; some expenditure can continue into perpetuity. The Rio Tinto Kennecott closure and environmental remediation provision includes an allowance for ongoing monitoring and remediation costs, including groundwater treatment, of approximately US$0.7 billion.

- The probability weighting of possible closure scenarios. The most significant impact of probability weighting is at the Pilbara operations (Iron Ore) relating to infrastructure, and incorporates the expectation that some infrastructure will be retained by the relevant State authorities post closure. The assignment of probabilities to this scenario reduces the closure provision by US$0.5 billion.

- Appropriate sources on which to base the calculation of the discount rate. The discount rate, by nature, is subjective and therefore sensitivities are shown below for how the provision balance would change if discounted at alternative discount rates.

There is significant estimation uncertainty in the calculation of the provision and cost estimates can vary in response to many factors including:

- changes to the relevant legal or local/national government requirements and any other commitments made to stakeholders

- review of remediation and relinquishment options

- additional remediation requirements identified during the rehabilitation

- the emergence of new restoration techniques

- precipitation rates and climate change

- change in foreign exchange rates

- change in the expected closure date

- change in the discount rate.

Experience gained at other mine or production sites may also change expected methods or costs of closure, although elements of the restoration and rehabilitation can be unique to each site. Generally, there is relatively limited restoration and rehabilitation activity and historical precedent elsewhere in the Group, or in the industry as a whole, against which to benchmark cost estimates.

The expected timing of expenditure can also change for other reasons, for example because of changes to expectations relating to Ore Reserves and Mineral Resources, production rates, renewal of operating licences or economic conditions.

Changes in closure cost estimates at the Group’s ongoing operations could result in a material adjustment to assets and liabilities in the next 12 months and would also impact the depreciation and the unwinding of discount in future years.

Changes to closure cost estimates for closed operations, and changes to environmental cost estimates at any operation, could cause a material adjustment to the income statement and closure liability. We do not consider that there is significant risk of a change in estimates for these liabilities causing a material adjustment to the income statement in the next 12 months. Any new environmental incidents may require a material provision but cannot be predicted.

Project-specific risks are embedded within the cash flows which are based on a central case estimate of closure activities assuming that the obligation is fulfilled by the Group. These cash flows are then discounted, as mentioned above, using a consistent discount rate applied to all locations.

Impact of climate change on our business Close-down, restoration and environmental costs

The underlying costs for closure have been estimated with varying degrees of precision based on a function of the age of the underlying asset and proximity to closure. For assets within 10 years of closure, closure plans and cost estimates are supported by detailed studies which are refined as the closure date approaches. These closure studies consider climate change and plan for resilience to expected climate conditions with a particular focus on precipitation rates. For new developments, consideration of climate change and ultimate closure conditions are an important part of the approval process. For longer-lived assets, closure provisions are typically based on conceptual level studies that are refreshed at least every 5 years; these are evolving to incorporate greater consideration of forecast climate conditions at closure.

Sensitivity analysis

Close-down, restoration and environmental provisions are based on risk-adjusted cash flows expressed in real terms. On 30 June 2024, we revised the closure discount rate from 2.0% to 2.5%, applied prospectively from that date. We reassessed the closure discount rate in the current year and continue to consider the real rate of 2.5% is the most appropriate rate to use.

The impact of discounting on the provision is illustrated below: