Play Communications S.A. – Annual report – 31 December 2019

Industry: telecoms

Consolidated financial statements prepared in accordance with IFRS as adopted by the European Union (extracts)

As at and for the year ended December 31, 2019

(Expressed in PLN, all amounts in tables given in thousands unless stated otherwise)

41. Summary of significant accounting policies (extract)

41.3 Revenue

Revenue is measured based on consideration specified in a contract with a customer and excludes amounts collected on behalf of third parties. The Group recognizes revenue when it transfers control over a good or service to a customer. Revenue is presented net of value added tax (VAT), rebates and discounts and after eliminating intragroup sales.

The Group’s revenues are earned mainly from the following telecommunications services and goods:

− voice and SMS telecommunications;

− data transfer;

− television and video on demand;

− value added services;

− interconnection;

− international roaming;

− sales of handsets and other equipment.

Revenues from voice, SMS telecommunications and data transfer include charges for telecommunications traffic originated in the Play network or roaming network, including revenues from prepaid products.

Goods and services may be sold separately or in bundled packages. For bundled packages, including e.g. mobile devices, monthly fees and activation fees from contract subscribers, the Group accounts for revenue from individual goods and services separately if they are distinct – i.e. if a good or service can be distinguished from other components of the bundled package and if a customer can benefit from it separately. The consideration for the bundled packages comprises cash flows from the customers expected to be received in relation to goods and services delivered over the Adjusted Contract Term (see Note 41.10). The consideration (transaction price) is allocated between separate performance obligations in a bundle based on their relative stand-alone selling prices. The Group identifies the following performance obligations: delivery of mobile devices, provision of telecommunications services and provision of service of device leasing. The stand-alone selling prices for mobile devices are estimated based on cost of sale plus margin. Please see Note 2.4.1. Stand-alone selling prices for

telecommunications services and lease services are set based on prices for non-bundled offers with the same range of services.

Services purchased by a customer beyond the contract are treated as a separate contract and recognition of revenue from such services is based on the actual airtime or data usage or is made upon the expiration of the Group’s obligation to provide the services.

Mobile services are billed on a monthly basis and payments are due shortly after the bill date.

Telecommunications revenue from the sale of prepaid products in single–element contracts (i.e. with one performance obligation for telecommunications services) is recognized at the face value of a prepaid top-up sold, net of VAT. The difference between the face value of a prepaid offerings and the value for which the offerings are sold by the Group to its distributors, constitutes commission earned by the distributors, who act as agents. The Group acts as a principal in such agreements. The costs of prepaid commissions are recognized as other service costs when the distribution service is provided, i.e. when the prepaid product is delivered to the end customer. The revenue from the sale of prepaid products is deferred until the end customer commences using the product and presented in the statement of financial position as deferred income in case the prepaid product is held by a distributor or as contract liability in case the prepaid product had been transferred to the end customer but not yet used. The revenue from the sale of prepaid products is recognized in the profit or loss as telecommunications services are provided, based on the actual airtime or data usage at an agreed tariff, or upon expiration of the obligation to provide the service.

Revenues from the value-added services are recognized in the amount of full consideration if the Group acts as principal in the relation with the customer or in the amount of the commission earned if the Group acts as agent.

Interconnection revenues are derived from calls and other traffic that originate in other operators’ networks but use Play network. The Group receives interconnection fees based on agreements entered into with other telecommunications operators. These revenues are recognized in the period in which the services were rendered.

International roaming revenues are derived from calls and other traffic generated by foreign operators’ customers in Play network. The Group receives international roaming fees based on agreements entered into with other telecommunications operators. These revenues are recognized in the profit or loss in the period in which the services were rendered.

Revenue from sale of handsets, other equipment and other goods is recognized when a promised good is transferred to the customer (typically upon delivery). The amount of revenue recognized for mobile devices is adjusted for expected returns, which are estimated based on the historical data. For mobile devices sold separately (i.e. without the telecommunications contract), a customer usually pays full price at the point of sale.

For mobile devices sold in bundled contracts, customers are offered two schemes of payments – full payment at the commencement of the contract (in such contracts the handset price is significantly reduced and the cost of device is recovered through monthly fees for telecommunication services) or instalment sales with monthly instalments paid over the period of the contract plus initial fee paid upon delivery of a handset.

Revenues from content services (e.g. music and video streaming, applications and other value added services) rendered to our subscribers are recognized after netting off costs paid by us to third party content providers (when the Group acts as an agent in the transaction) or in the gross amount billed to a subscriber (when the Group acts as a principal).

41.4 Interest income

Interest income is recognized on a time-proportion basis using the effective interest method.

41.10 Contract costs

Contract costs eligible for capitalization as incremental costs of obtaining a contract comprise commission on sale relating to postpaid contracts and “mix” contracts (contracts for a specified number and value of top-ups) with acquired or retained subscribers. Contract costs are capitalized in the month of service activation if the Group expects to recover those costs. Contract costs comprise sales commissions to dealers and to own salesforce which can be directly attributed to an acquired or retained contract. Contract costs constitute non-current assets as the economic benefits from these assets are expected to be received in the period longer than twelve months.

In all other cases, including acquisition of prepaid telecommunications customers, subscriber acquisition and retention costs are expensed when incurred.

Capitalized commission fees relating to postpaid contracts are amortized on a systematic basis that is consistent with the transfer to the customer of the services when the related revenues are recognized. Contract costs relating to contracts signed with acquired or retained subscribers are amortized:

– for postpaid contracts – over the Adjusted Contract Term, which is the period after which the Group expects to offer a subsequent retention contract to a customer, which is usually a few months before the contractual term lapses,

– for “mix” contracts – over the term during which a customer is expected to fulfil their obligation in relation to all top-ups required under a contract.

When the customer enters into a retention contract before the term of the previous one expires (which means that the original contracts costs have not been fully amortized), the new asset is recognized in the month the new contract is signed. The new asset is amortized over the term representing the sum of the period remaining to the end of the previous contract and the retention contract term. Amortization period of the contract cost relating to previous contract is then shortened to be in line with the actual contract term.

Contract costs capitalized are impaired if the customer is disconnected or if the asset’s carrying amount exceeds projected discounted cash flows relating to the contract. An impairment loss is recognized in profit or loss to the extent of the carrying amount of an contract costs asset over the remaining amount of consideration that the Group expects to receive in exchange for the goods or services to which the asset relates less the costs that relate directly to providing those goods or services and that have not been recognized as expenses.

41.12 Inventories

Inventories are stated at the lower of cost and net realizable value. Net realizable value is the estimated selling price in the ordinary course of business less the applicable variable selling expenses. For inventories intended to be sold in promotional offers calculation of net realizable value takes into account future margin expected from telecommunications services, with which the item of inventories is offered.

Inventories include handsets and other equipment transferred to dealers who act as agents. They are expensed to costs of goods sold on the date of activation of telecommunications services in relation to which the equipment was sold to the end customer or on the date when the equipment was sold to the end customer without a telecommunications service contract. The Group estimates the prevalent period between the date of transfer of the equipment to dealer and the date of service activation based on historical data. If no service agreement relating to the mobile device is activated during the period estimated as described above, it is assumed, that the mobile device was sold to the end customer without related service agreement and revenue from sale of goods and corresponding cost of sale are recognized in statement of comprehensive income.

41.14 Contract assets

A contract asset is the Group’s right to consideration in exchange for goods or services that the Group has transferred to a customer when that right is conditional on something other than the passage of time (for example, delivery of other elements of the contracts). The Group recognizes contract assets mainly from the contracts in which goods delivered at a point in time are bundled with services delivered over time. The Group considers contract assets as current assets as they are expected to be realized in the normal operating cycle.

The loss allowance for contract assets is measured and recognized under IFRS 9 at the initial recognition of contract assets. The Group uses professional judgement to calculate probability–weighted estimate of credit losses over the expected life of contract assets.

41.24 Deferred income

Deferred income on sales of contract services comprises amounts relating to services that will be delivered in the future, which are billed to a customer in advance but not yet due. Deferred income on sales of prepaid products comprises the value of prepaid products delivered to a distributor but not yet transferred to the end customer.

41.25 Contract liabilities

Contract liabilities comprise the Group’s obligation to transfer goods or services to a customer for which the Group has received consideration from the end customer or the amount is due.

2.4 Critical accounting estimates and judgments (extracts)

2.4.1 Recognition of revenue

The application of IFRS 15 requires the Group to make judgements that affect the determination of the amount and timing of revenue from contracts with customers (please see also Note 4). These include:

– determining the timing of satisfaction of performance obligations,

– determining the transaction price allocated to them,

– determining the standalone selling prices.

The stand-alone selling prices for mobile devices are estimated as cost of sale plus margin. Stand-alone selling prices for telecommunications services are set based on prices for non-bundled offers with the same range of services. The transaction price is calculated as total consideration receivable from the customer over the Adjusted Contract Term, which is the period after which the Group expects to offer a subsequent retention contract to a customer, which is usually a few months before the contractual term lapses.

Significant financing component

The Group used the practical expedient described in paragraph 63 of IFRS 15 and did not adjust the promised amount of consideration for the effects of a significant financing component because it has assessed that for most of the contracts the period between when the Group transfers the equipment to the customer and when the customer pays for the equipment is one year or less.

Material right considerations

The Group has not identified any material rights in the contracts with customers which would need to be treated as separate performance obligations. In particular, the Group does not consider an activation fee to provide a material right to a customer to extend the contract without paying an additional activation fee. Also, the Group has assessed that for additional services offered to existing customers at a discounted price, the value of the revenue which would need to be deferred until satisfaction of the performance obligation associated with the potential material right, would be insignificant and therefore such potential material rights are not treated as separate performance obligations.

Agent vs. principal considerations in relation to cooperation with dealers

The Company cooperates with a network of dealers who sell contract services (including these bundled with handsets) and prepaid services. The Group has assessed that the dealers act as agents (and therefore do not control the goods or services before they are provided to the end-customer) in this process, for the following reasons:

a) the Group bears primary responsibility for fulfilling the promise to provide the specified good and service – the Group is responsible for delivering telecommunications services to the end-customer and organizes the process of repairs of the equipment within the guarantee period,

b) prices of services and equipment delivered to customers are determined by the Group and not by the dealer;

c) dealers are remunerated in the form of commissions;

d) credit risk related to consideration for service and in case of instalment sales model also credit risk related to consideration for equipment is borne by the Group.

2.4.3 Estimation of provision for impairment of financial assets

The Group considers a financial asset in default when internal or external information indicates that the Group is unlikely to receive the outstanding contractual amounts in full before taking into account any credit enhancements held by the Group. The expected credit loss is calculated as expected gross carrying amount of the financial asset at default date multiplied by expected credit loss rate.

When measuring expected credit loss provision for billing receivables the Group uses collectability ratio from previous periods including information on recoverability through the process of sales of outstanding invoices as well as forward looking information.

For other trade receivables the Group performs assessment for each individual debtor taking into account the probability of default or delinquency in payments and the probability that debtor will enter into financial difficulties or bankruptcy. The Group uses all reasonable and supportable information regarding debtors available at the assessment date, including the information about securities, e.g. guarantees, deposits and insurance.

When calculating the loss allowance for contract assets the Group considers a financial asset in default when the Group is unlikely to receive the cash flows from customers which would be used to settle the outstanding contract assets balance, e.g. when the customer is disconnected as a result of breach of the contract. The Group uses professional judgement to calculate probability–weighted estimate of credit losses over the expected life of contract assets.

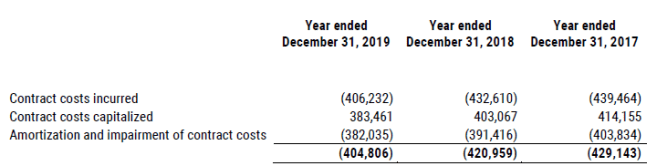

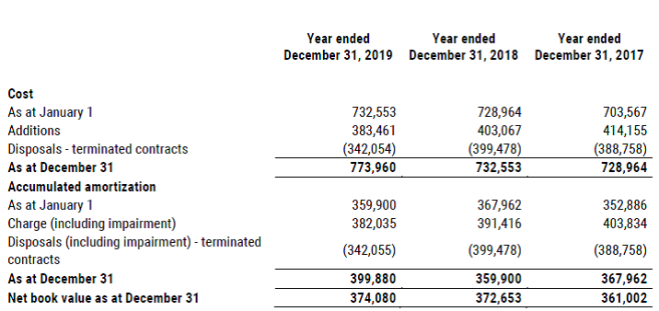

6. Contract costs, net

The contract costs presented above are costs to obtain contracts with customers (sales commissions).

9. Other operating income and other operating costs

Gain / loss on receivables management

The lines “Gain on receivables management” and “Loss on receivables management” represent the net amount resulting from: cost resulting from movement of the provision for impairment of receivables of 62,008 thousand in the year ended December 31, 2019 (72,914 thousand in the year ended December 31, 2018 and 53,634 thousand for the year ended December 31, 2017), net result on sales of overdue receivables to collecting agencies as well as income from early contract termination.

Loss on receivables management during the year ended December 31, 2019 resulted from an unfavorable change in market conditions for receivables sales and decrease of recovery ratio in comparison to the year ended December 31, 2018.

During the year ended December 31, 2018 the Group reversed the one-off write-off cost of interconnection receivables from the years 2011-2013 in the amount of PLN 12,735 thousand due to change of the court ruling from 2016 (due to initial unfavorable court ruling the Group recognized cost during the year ended December 31, 2016).

Gain on the receivables management recognized in the year ended December 31, 2017 resulted from the decrease in provision for impairment of trade receivables due to decreased volume of installments sales as well as improved collectability of receivables achieved among others thanks to accelerated sales of receivables to collection agencies at favorable prices.

The line “Impairment of trade receivables” represents the amount charged to profit and loss according to IFRS 9.

When calculating the impairment provision the Group takes into account the price it expects to be able to recover in future from sales of receivables.

For movements of the provision for impairment of trade and other receivables please see also Note 21.

Impairment of contract assets

Impairment of contract assets recognized in the year ended December 31, 2019 and year ended December 31, 2018 related mainly to subsidy contracts for which amount of contract assets and its write-off is significantly higher than for installment contracts. The impairment recognized in the current period and in the year ended December 31, 2018 increased in comparison to the year ended December 31, 2017 as impairment recognized in 2017 related primarily to installment sales contracts with lower amount of contract assets.

For movements of the provision for impairment of contract assets please see also Note 22.

17. Contract costs

The contract costs presented above are costs to obtain contracts with customers (sales commissions).

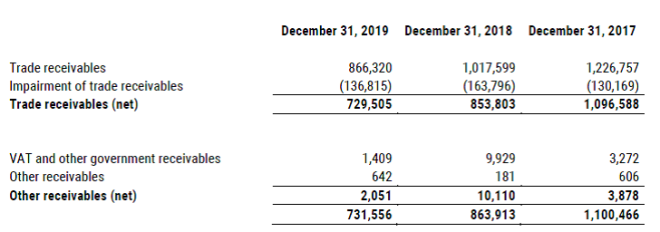

21. Trade and other receivables

Total amount of trade receivables are receivables from contracts with customers.

Trade receivables include installment receivables relating to sales of handsets and mobile computing devices. The balance of trade receivables decreased following the significant reduction in the volume of installment sales after October 2016.

The Group classifies trade receivables within business model “hold to collect contractual cash flows” and measures them at amortized costs. As part of its receivables management the Group sells past due receivables to third party collection agencies; the receivables are then derecognized. Such sales are aimed at mitigating potential credit losses due to deterioration of credit-standing of the debtors.

As of December 31, 2019 trade receivables of PLN 136,815 thousand (December 31, 2018: PLN 163,796 thousand and December 31, 2017: PLN 130,169 thousand) were impaired. The individually impaired receivables are mainly receivables from subscribers who have violated the provisions of the agreements or who have withdrawn from agreements.

As of December 31, 2019 trade receivables of PLN 174,500 thousand (December 31, 2018: PLN 214,580 thousand and December 31, 2017: PLN 195,945 thousand) were past due but not impaired. These relate mainly to individual customers for whom there is no history of default.

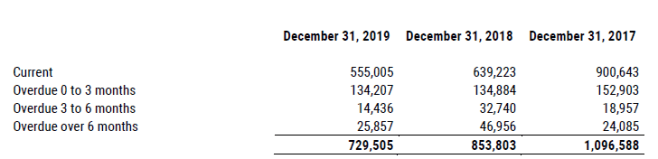

The ageing analysis of trade receivables (net) that were not impaired is as follows:

The value of overdue receivables in the year ended December 31, 2019 decreased in comparison to previous years mainly due to significant sales transaction to collection agencies during 2019.

The value of receivables overdue over 3 months increased in the year ended December 31, 2018 in comparison to prior and subsequent year due to the fact that in 2018 the Group reduced the volume of sales of receivables to collection agencies because of unfavorable market prices for sales of receivables.

The maximum exposure to credit risk at the end of the reporting period is the carrying amount of each class of receivables mentioned above.

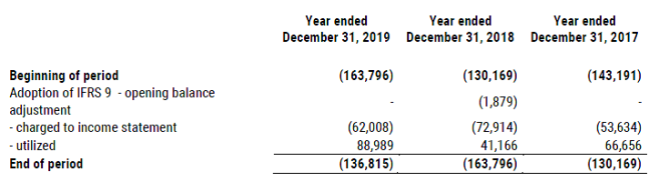

Movements of the provision for impairment of trade receivables are as follows:

Utilization of provision during the year ended December 31, 2019 increased in comparison to previous years due to significant transactions of sales of impaired receivables to collection agencies. For explanation of changes in the amounts charged or credited to income statement please see Note 9.

Amounts charged to the allowance account are generally written down when there is no expectation of recovering additional cash.

Credit risk exposure resulting from the Group’s trade receivables as at December 31, 2019 and December 31, 2018 was as follows:

22. Contract assets

The value of impairment of contract assets presented above represents the expected credit loss recognized in accordance with IFRS 9 at the initial recognition of the contract asset. Please see also Note 2.4.3.

Expected credit loss rate for contract assets as at 31 December 2019 and 2018 amounted to 5.3% and 5.1%, respectively.

In the year ended December 31, 2017 the expected credit loss was not estimated. The actually impaired contract assets were written off in the period when the actual credit loss occurred. The charge to income statement was equal to the value of the contract assets relating to contracts actually disconnected. In the year ended December 31, 2018 and in the current year the value of the contract assets relating to contracts actually disconnected is presented in line “utilization” below, whereas the line “charged to income statement” represents the changes in estimated credit losses which the Group expects to incur in future.

Movements of the provision for impairment of contract assets are as follows:

For explanation of changes in the impairment charged to income statement – please see Note 9.

Movements in the contract assets balance for the years ended: 31 December 2019, 2018 and 2017 were as follows:

Additions correspond to adjustments to sales of goods under IFRS 15 when services and devices are sold in bundled packages to customers.

In current and in comparative periods there were no significant changes in the time frame for a right to consideration to become unconditional or in the time frame for a performance obligation to be satisfied.

In current and in comparative periods there were no cumulative catch-up adjustments to revenue that affect the corresponding contract asset or contract liability, including adjustments arising from a change in an estimate of the transaction price or a contract modification.

30. Contract liabilities

Contract liabilities comprise the Group’s obligation to transfer goods or services to a customer for which the Group has received consideration from the end customer or the amount is due.

As at December 31, 2019 contract liabilities comprise Group’s obligation to transfer services from unused contract and prepaid balances.

The table below represents amounts recognized as service revenue during the reporting periods for which the customers had paid in advance and which had been presented as contract liabilities before the beginning of the reporting period.

32. Deferred income

Deferred income on sales of prepaid services comprises the value of prepaid products delivered to a distributor but not yet transferred to the end customer. Prepaid products transferred to end customer and not used are presented as contract liabilities (see also Note 30) while amounts of prepaid products used by end customers are recognized as revenue in the statement of comprehensive income.

Deferred income on sales of contract services comprises amounts relating to services that will be delivered in the future which are billed to a customer in advance but not yet due, whereas amounts billed in advance and due are presented as contract liabilities. Deferred income balances for contract services depend on whether due date for services is after or before the reporting date and may vary significantly between reporting dates.

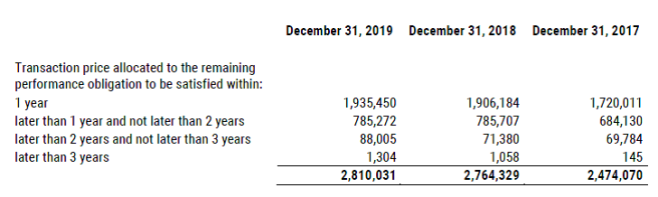

4. Operating revenue

Total operating revenue corresponds to the revenue from contracts with customers.

Other usage revenue consists mainly of revenues from MVNOs to whom the Group provides telecommunications services and revenues generated from services rendered to subscribers of foreign mobile operators that have entered into international roaming agreements with the Group.

Usage revenues generated by 3S Group acquired during the year ended December 31, 2019 are presented in “other usage revenue” line.

In the reporting periods there was no revenue recognized from performance obligations satisfied or partially satisfied in previous periods.

The following table includes revenue expected to be recognized in the future related to performance obligations that are unsatisfied (or partially unsatisfied) at the reporting date.