NEXT plc – Annual report – 31 January 2026

Industry: retail

GROUP ACCOUNTING POLICIES (extract)

Customer and Other Receivables

Customer receivables are outstanding customer balances less an allowance for impairment. Customer receivables are recognised when the Group becomes party to the contract which happens when the goods are dispatched. They are derecognised when the rights to receive the cash flows have expired, e.g. due to the settlement of the outstanding amount or where the Group has transferred substantially all the risks and rewards associated with that contract. Other trade receivables are stated at invoice value less an allowance for impairment. Customer and other receivables are subsequently measured at amortised cost as the business model is to collect contractual cash flows and the debt meets the SPPI criterion.

Impairment

In accordance with the accounting policy for impairment – financial assets, the Group recognises an allowance for ECLs for customer and other receivables. IFRS 9 requires an impairment provision to be recognised on origination of a customer advance, based on its ECL. The Group has taken the simplification available under IFRS 9 paragraph 5.5.15 which allows the loss amount in relation to a trade receivable to be measured at initial recognition and throughout its life at an amount equal to lifetime ECL. This simplification is permitted where there is either no significant financing component (such as customer receivables where the customer is expected to repay the balance in full prior to interest accruing), or where there is a significant financing component (such as where the customer expects to repay only the minimum amount each month), but the directors make an accounting policy choice to adopt the simplification. Adoption of this approach means that Significant Increase in Credit Risk (SICR) and Date of Initial Recognition (DOIR) concepts are not applicable to the Group’s ECL calculations.

Lifetime ECLs are the ECLs that result from all possible default events over the expected life of a financial instrument.

ECL is the product of the probability of default (PD), exposure at default (EAD) and loss given default (LGD), discounted at the original EIR. The assessment of credit risk and the estimation of ECL are required to be unbiased, probability-weighted and should incorporate all available information relevant to the assessment, including information about past events, current conditions and reasonable and supportable forecasts of economic conditions at the reporting date. The forward looking aspect of IFRS 9 requires considerable judgement as to how changes in economic factors might affect ECLs. The ECL model applies four macroeconomic scenarios including a base case which is viewed by management to be the most likely outturn, together with an upside, downside and extreme scenario. A 45% weighting is applied to the base case and 5% to the upside scenario, 35% to the downside scenario and 15% to the extreme scenario.

IFRS 9 “Financial instruments” paragraph 5.5.20 ordinarily requires an entity to not only consider a loan, but also the undrawn commitment and the ECL in respect of the undrawn commitment, where its ability to cancel or demand repayment of the facility does not limit its exposure to the credit risk of the undrawn element. However, the guidance in IFRS 9 on commitments relates only to commitments to provide a loan (that is, a commitment to provide financial assets, such as cash) and excludes from its scope rights and obligations from the delivery of goods as a result of a contract with a customer within the scope of IFRS 15 “Revenue from contracts with customers” (that is, a sales commitment). Thus, the sales commitment (unlike a loan commitment) is not a financial instrument, and therefore the impairment requirements in IFRS 9 do not apply until delivery has occurred and a receivable has been recognised.

Impairment charges in respect of customer receivables are recognised in the Income Statement within “Impairment losses on customer and other receivables”.

Delinquency is taken as being in arrears and credit impaired is taken as being the loan has defaulted, which is considered to be the point at which the debt is passed to an internal or external Debt Collection Agency (DCA) and a default registered to a Credit Reference Agency (CRA), or any debt 90 days past due. Delinquency and default are relevant for the estimation of ECL, which segments the book by customer indebtedness, banded into 4 risk bands by arrears stage (see Note 30).

Financial assets are written off when there is no reasonable expectation of recovery, such as when a customer fails to engage in a repayment plan with the Group. If recoveries are subsequently made after receivables have been written off, they are recognised in the Income Statement.

The key inputs into the ECL calculation are:

PD: “Probability of Default” is an estimate of the likelihood of default over the expected lifetime of the debt. NEXT has assessed the expected lifetime of customer receivables and other trade receivables, based on historical payment practices. The debt is segmented by arrears stage, Experian’s Consumer Indebtedness Index (a measure of customers’ affordability) and expected time of default.

EAD: “Exposure at Default” is an estimate of the exposure at that future default date, taking into account expected changes in the exposure after the reporting date, i.e. repayments of principal and interest, whether scheduled by the contract or otherwise and accrued interest from missed payments. This is stratified by arrears stage, Experian’s Consumer Indebtedness Index and expected time of default.

LGD: “Loss Given Default” is an estimate of the loss arising in the case where a default occurs at a given time. It is based on the difference between the contractual cash flows due and those that NEXT would expect to receive, discounted at the original EIR. It is usually expressed as a percentage of the EAD. NEXT includes all cash collected over five years from the point of default.

The Group uses probability weighted economic scenarios that are integrated into the model, in order to evaluate a range of possible outcomes as is required by IFRS 9. An analysis of historical performance suggests that the expected performance of the book is most closely aligned to the forecast change in unemployment rate. However, management considers that the inputs and models used for the ECLs may not always capture all characteristics of the market at the Balance Sheet date. To reflect this qualitative adjustments or overlays are made, based on external data, historical performance and future expected performance.

Major Sources of Estimation Uncertainty and Judgement (extract)

Expected credit losses on Online customer receivables (estimation)

The allowance for ECL (Note 14) is calculated on a customer-by-customer basis, using a combination of internally and externally sourced information, including expected future default levels (derived from historical defaults, overlaid by arrears and indebtedness profiles, and third party macro-economic forecasts) and future predicted cash collection levels (derived from past trends and future projections).

Prior to default, the greatest sensitivity relates to the ability of customers to afford their payments (impacting the Probability of Default (PD) and, to a lesser extent, the Exposure at Default (EAD)). Once a customer receivable has defaulted, there is limited sensitivity in expected recoveries due to the lack of significant variability in cash collection levels post default.

Of the total ECL (Note 14), £66.2m (2025: £71.1m) relates to defaulted debt (without significant uncertainty) and £99.1m (2025: £110.2m) is for non defaulted debt, where significant estimation uncertainty exists. The remainder of this section relates to non defaulted debt.

Macroeconomic Uplift

The first main area of major estimation uncertainty in calculating the ECL is the impact of a change in unemployment. Management use an independent forecast of unemployment, provided by Experian, and weights the effect of the expected (base case), upside, downside and extreme scenarios in the proportions 45/5/35/15. The expected scenario assumes a central unemployment rate peaking at 5.1% during 2026. This weighted view adds £11.0m (2025: £11.3m) to the underlying model ECL. A sensitivity assessment on the unemployment scenarios has been performed by management and the impact of a significant but plausible change would not be material.

The second main area of major estimation uncertainty in calculating the ECL is the impact of macroeconomic factors that are not included in the “macroeconomic uplift” calculation, due to it being solely based on changes in unemployment rate. Management have reviewed independent forecasts of key labour market and consumer economy indicators which have the potential to negatively affect customer payment behaviour. These forecasts, project continued weakness in real wage growth and job vacancies, along with ongoing inflationary pressures. In order to reflect the underlying risk in the loan book, the following adjustment has been incorporated into the provision:

- Recognition of the ongoing risk of an increased ECL for customers who have shown recent indicators of distress and considered to be at higher risk of default

With consumer prices in the UK still elevated following an extended period of high inflation, disposable income is likely to remain constricted for consumers with lower levels of financial resilience. In addition, real terms wage growth, along with job vacancy data have remained weakened in recent statistics and updated independent forecasts. Management believe this may adversely impact the recoverability of customer receivables, specifically customers who are modelled to have a low income, high mortgage repayment or are renting. A further overlay to increase the provision coverage of these customers has been applied, which forms £24.5m (2025: £38.8m) of the total ECL.

- Sensitivity to the Probability of Default

Following application of the above overlays, management believes that there is adequate provision for ECL based on a stressed, but realistic level of payments. The primary area of estimation uncertainty which could have a material impact to the provision is the probability of default. If the probability of default were to double, this would increase the provision by £38.8m.

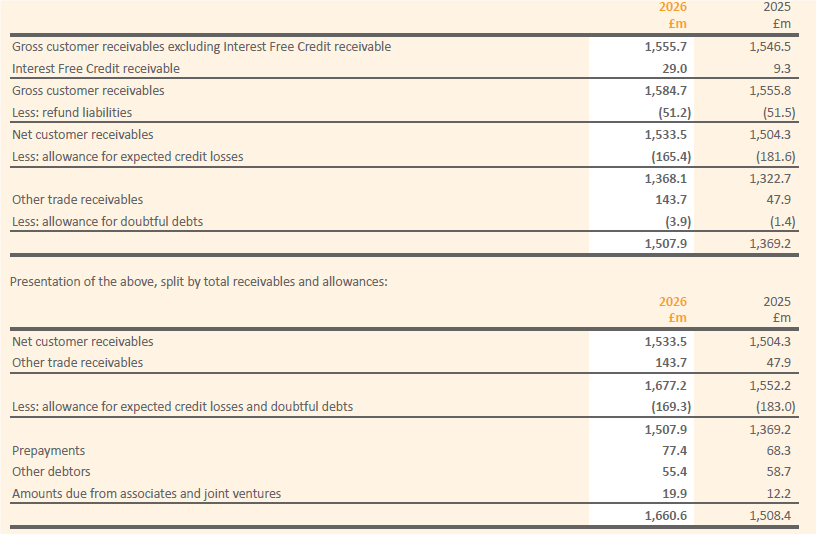

14. Customer and Other Receivables

The following table shows the components of net receivables:

No interest is charged on online credit account customer receivables if the statement balance is paid in full and to terms; otherwise balances bear interest at a variable annual percentage rate of 24.9% (2025: 24.9%) at the year-end date, except for £129.9m (2025: £95.6m) of balances on the “pay in 3” product which bears interest at 29.9% (2025: 29.9%) at the year end date.

The Group applies the simplified approach to providing for expected credit losses prescribed by IFRS 9, which permits the use of the lifetime expected loss provision for all trade receivables. To measure the expected credit losses, other trade receivables have been allocated to the Risk band 1 (defined in Note 30), representing management’s view of the risk and the days past due. The expected credit losses incorporate forward looking information.

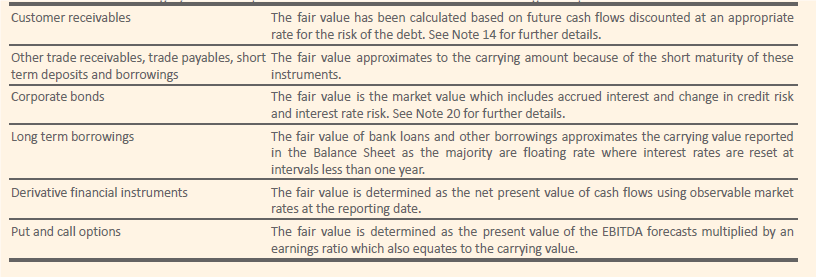

The fair value of customer receivables and other trade receivables is approximately £1,490m (2025: £1,340m). This has been calculated based on future cash flows discounted at an appropriate rate for the risk of the debt. The fair value is within Level 3 of the fair value hierarchy (refer to the Fair Value Hierarchy table in Note 29).

Expected irrecoverable amounts on balances with indicators of impairment are provided for based on past default experience, adjusted for expected behaviour. Receivables which are impaired, other than by age or default, are separately identified and provided for as necessary.

The ECL allowance against other debtors and amounts due from associates and joint ventures is immaterial in the current and prior year. The maximum exposure to credit risk at the reporting date is the carrying value of each class of asset.

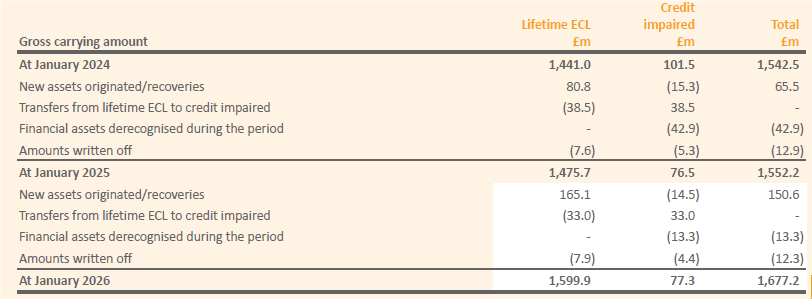

An analysis of changes in the gross carrying amount in relation to customer receivables and other trade receivables is as follows:

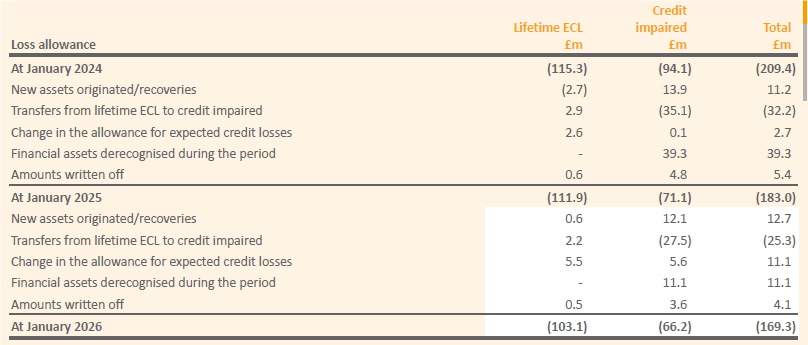

An analysis of the changes in the impairment allowance for customer receivables and other trade receivables is as follows:

Change in the allowance for expected losses includes an ECL release of £20.0m in the current year (2025: £10.0m).

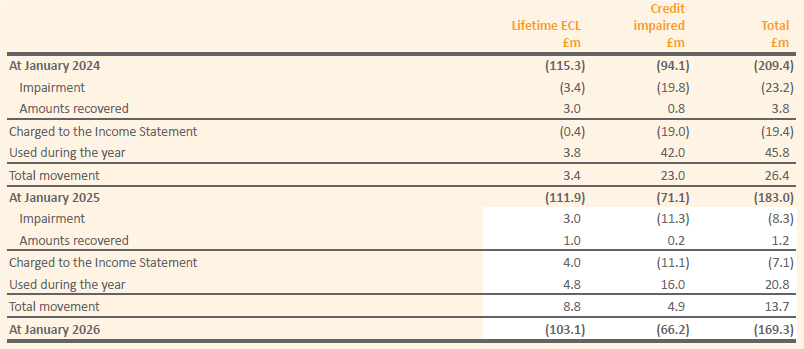

The amount charged to the Income Statement of £7.1m (2025: £19.4m) differs to the bad debt charge of £1.6m (2025: £17.5m) in the Chief Executive’s Review on page 42 due to the inclusion of other trade receivables within this note not included within the Chief Executive review.

Information on the Group’s credit risk in relation to customer receivables is provided in Note 30.

29. Financial Instruments: Fair Values (extract) The fair values of each category of the Group’s financial instruments are based on the following assumptions:

30. Financial Instruments: Financial Risk Management and Hedging Activities (extract)

Credit risk

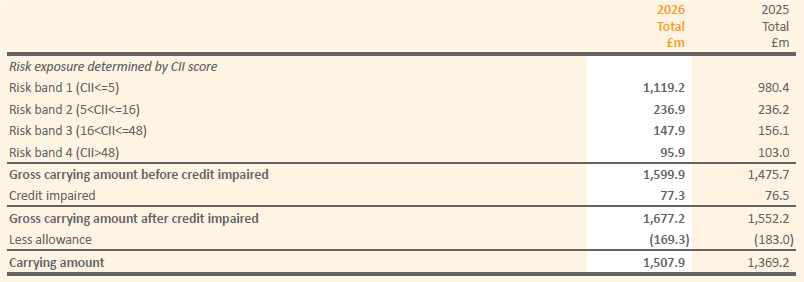

Credit risk is the risk of financial loss to the Group if a customer or counterparty to a financial instrument fails to meet its contractual obligations and arises primarily from the Group’s Online customer receivables. The carrying amount of financial assets represents the maximum residual credit exposure, which was £1,481.5m at the reporting date (2025: £1,369.2m). These are detailed in Note 14.

The Group’s credit risk in relation to customer receivables is influenced mainly by the individual characteristics of each customer. The Board has established a credit policy under which each new credit customer is analysed individually for creditworthiness and subject to credit verification procedures. Receivable balances are monitored on an ongoing basis and provision is made for estimated irrecoverable amounts using forward looking estimates. The concentration of credit risk is limited due to the Online customer base being large and diverse. As at January 2026, there were 3.18m active customers (2025: 3.00m) with an average balance of £482 (2025: £512). The Group’s outstanding receivables balances and impairment losses are detailed in Note 14. The performance of our credit risk policies and the risk of the debtor book are monitored weekly by management. Any trends and deviations from expectations are investigated. Senior management review is carried out monthly.

Customer receivables with a value of £6.7m (2025: £8.3m) were on a Reduced Payment Indicator (RPI) plan. An allowance for Expected Credit Losses (ECLs) of £4.2m (2025: £5.9m) has been made against these balances. Customers are typically on RPI plans for a period of 12 months during which no interest is charged and repayment rates are reduced. On completion of the RPI plan the customer would be returned to normal scoring, which considers multivariate factors, including indebtedness and repayment history, in the assessment of their expected risk levels. Any modification gain or loss recognised is immaterial to the financial statements.

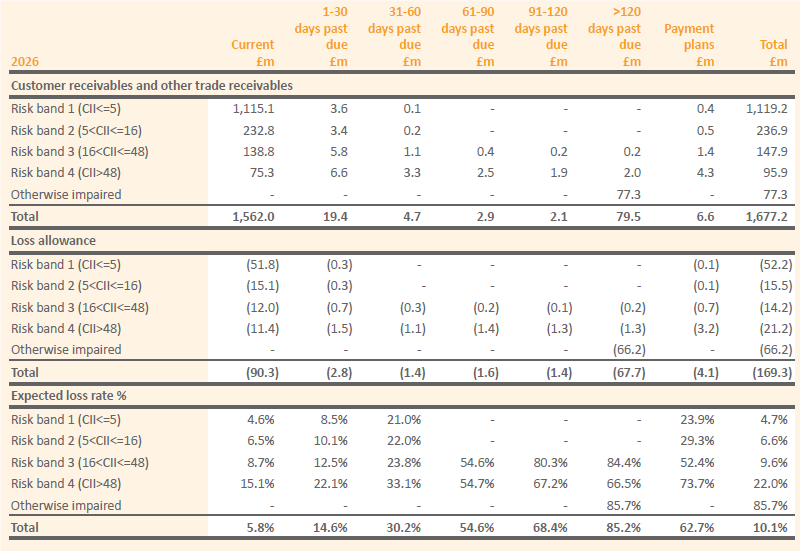

The Group uses Experian Delphi for Customer Management which provides a suite of characteristics and scores to monitor the credit behaviour of new and existing customers. The principal score for making risk decisions around credit limit changes, and monitoring the risk of associated sales, is the Account and Arrears Management (“AAM”) score. The principal measure to assess a customer’s ability to afford repayments, and our allowance for expected credit losses under IFRS 9, is the Consumer Indebtedness Index (“CII”). The CII is a score within the range of 0 to 99. A lower CII score is representative of a lower level of risk associated with the debt (i.e. a lower CII score indicates the customer has a greater ability to afford repayments).

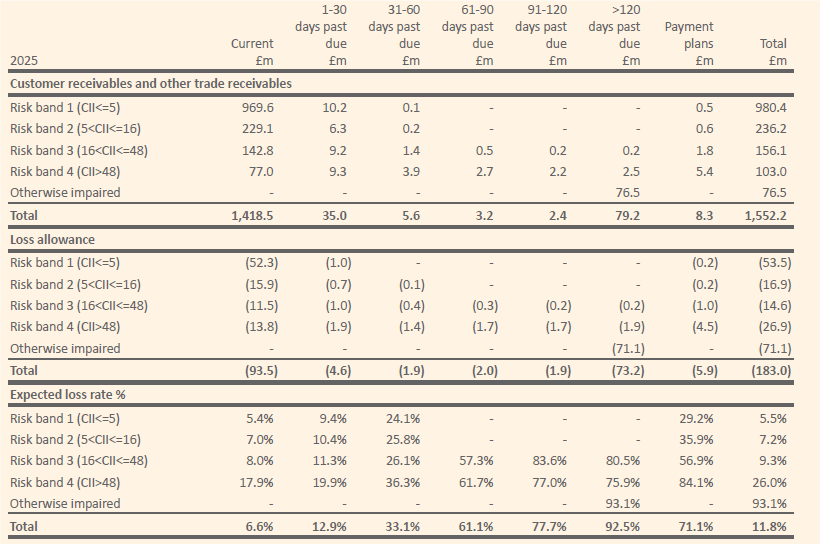

The following table contains an analysis of customer and other receivables segmented by CII score at the end of the reporting period. For the purpose of this analysis, trade receivables are recognised in Risk band 1.

Analysis of customer receivables and other trade receivables, stratified by credit grade, is provided in the tables below. Since 2024, CII scores have been based on GEN11.

Credit risk on other financial assets

Investments of cash surpluses and derivative contracts are made through banks and companies which must fulfil credit rating and investment criteria approved by the Board. Risk is further mitigated by diversification and limiting counterparty exposure. The Group does not consider there to be any impairment loss in respect of these balances (2025: £nil). The maximum exposure to credit risk at the reporting date is the carrying value of each class of asset as the debt is not collateralised.