Nippon Sheet Glass Company Limited – Annual report – 31 March 2026

Industry: manufacturing

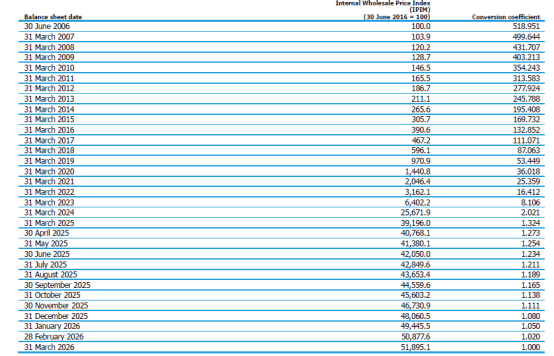

40. Hyperinflationary accounting adjustments

As from the second quarter of FY2019, the wholesale price index in Argentina indicated that cumulative 3-year inflation had exceeded 100 percent. Consequently the Group has concluded that its subsidiaries in Argentina, each of which has the Argentine Peso as a functional currency, are currently operating in a hyperinflationary environment. The Group has therefore applied accounting adjustments to the underlying financial results and position of its subsidiaries in Argentina as required by IAS 29 ‘Financial Reporting in Hyperinflationary Economies’.

As required by IAS 29, the Group’s consolidated financial statements will include the results and financial position of its Argentinian subsidiaries, restated in terms of the measuring unit current at the period end date.

For the restatement of results and financial positions of its Argentinian subsidiaries, the Group will apply the conversion coefficient derived from the Internal Wholesales Price Index (IPIM) published by Instituto Nacional de Estadística y Censos de la República Argentina (INDEC). IPIM and corresponding conversion coefficients from June 2006 are presented below.

The Group’s subsidiaries in Argentina have restated their non-monetary items held at historical cost, namely property, plant and equipment, by applying the conversion coefficient based on when the items were initially recognized. Monetary items and non-monetary items held at current cost will not be restated, as they are considered to be expressed in terms of the measuring unit current at the period end date. The effect of inflation on the net monetary position of the Group’s Argentinian subsidiaries is presented in the finance income or finance expenses section of the income statement.

The Argentinian subsidiaries’ income statement and cash flow statement will also be restated, applying the conversion coefficient for the current financial year as shown in the above table.

For the purpose of consolidation, the results and financial position of the Group’s Argentinian subsidiaries are translated using the closing exchange rates at the period end date. Comparative financial statements are not restated based on IAS 21 ‘The Effects of Changes in Foreign Exchange Rates’ para 42(b).

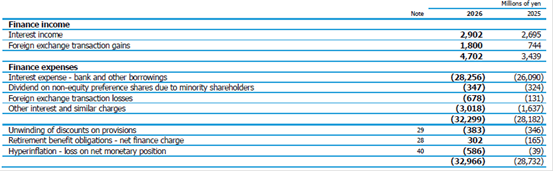

9. Finance income and expenses