Rolls-Royce Holdings plc – Annual report – 31 December 2025

Industry: manufacturing

1 Accounting policies (extract)

Revenue recognition and contract assets and liabilities

Revenue recognised comprises sales to the Group’s customers after discounts and amounts payable to customers. Revenue excludes value added taxes. The transaction price of a contract is typically clearly stated within the contract, although the absolute amount may be dependent on escalation indices and long-term contracts that require the key estimates highlighted below to be made. Refund liabilities, where sales are made with a right of return, are not typical in the Group’s contracts. Where they do exist, and consideration has been received, a portion based on an assessment of the expected refund liability is recognised within other payables. The Group has elected to use the practical expedient not to adjust revenue for the effect of financing components where the expectation is that the period between the transfer of goods and services to customers and the receipt of payment is less than a year. Consideration is received in the form of deposits and payments for completion of milestones or performance obligations. LTSA cash receipts are typically received based on EFHs.

Sales of standard OE, spare parts and time and material (T&M) overhaul services are generally recognised on transfer of control to the customer. This is generally on delivery to the customer, unless the specific contractual terms indicate a different point. The Directors consider whether there is a need to constrain the amount of revenue to be recognised on delivery based on the contractual position and any relevant facts, however, this is not typically required.

Sales of OE and services that are specifically designed for the contract (most significantly in the Defence business) are recognised by reference to the progress towards completion of the performance obligation, using the cost method described in the key judgements, provided the outcome of contracts can be assessed with reasonable certainty.

The Group generates a significant portion of its revenue on aftermarket arrangements arising from the installed OE fleet. As a consequence, in particular in the Civil Aerospace large engine business, the Group will often agree contractual prices for OE deliveries that take into account the anticipated aftermarket arrangements. Sometimes this may result in losses being incurred on OE. As described in the key judgements, these contracts are not combined. The consideration in the OE contract is therefore allocated to OE performance obligations and the consideration in the aftermarket contract to aftermarket performance obligations.

Key areas of the accounting policy are:

- Future variable revenue from long-term contracts is constrained to take account of the risk of non-recovery of resulting contract balances from reduced utilisation e.g. EFHs, based on historical forecasting experience and the risk of aircraft being parked by the customer.

- A significant amount of revenue and cost related to long-term contract accounting is denominated in currencies other than that of the relevant Group undertaking, most significantly USD transactions in sterling and euro denominated undertakings. These are translated at estimated long-term exchange rates.

- The assessment of stage of completion is generally measured for each contract. However, in certain cases, such as for CorporateCare agreements, where there are many contracts covering aftermarket services each for a small number of engines, the Group accounts for a portfolio of contracts together, as the effect on the Consolidated Financial Statements would not differ materially from applying the standard to the individual contracts in the portfolio. When accounting for a portfolio of LTSAs, the Group uses estimates and assumptions that reflect the size and composition of the portfolio.

- A contract asset/liability is recognised where payment is received in arrears/advance of the revenue recognised in meeting performance obligations.

- Contract modifications of LTSAs can be accounted for as separate contracts, termination of the existing contract and the creation of a new contract, or as part of the existing contract. The treatment is dependent on whether the change in scope is because of the addition of promised goods or services that are distinct and whether the price increases by an amount that reflects their standalone selling prices.

- Where material, wastage costs (see key judgements on page 126) are recorded as an expense and excluded from the measure of progress of LTSA contracts.

- The Group recognises a liability for their obligation to repurchase parts it has sold to the maintenance, repair and overhaul bases who overhaul the Group’s customers’ engines.

If the expected costs to fulfil a contract exceed the expected revenue, a contract loss provision is recognised for the excess costs.

The Group pays participation fees to airframe manufacturers, its customers for OE, on certain programmes. Amounts paid are initially treated as contract assets and subsequently charged as a reduction to the OE revenue when the engines are transferred to the customer.

The Group has elected to use the practical expedient to expense as incurred any incremental costs of obtaining or fulfilling a contract if the amortisation period of an asset created would have been one year or less. Where costs to obtain a contract are recognised in the balance sheet, they are amortised over the performance of the related contract (eight to 15 years).

Key judgement – Whether Civil Aerospace OE and aftermarket contracts should be combined

In the Civil Aerospace business, OE contracts for the sale of engines to be installed on new aircraft are with the airframers, while the contracts to provide spare engines and aftermarket goods and services are with the aircraft operators, although there may be interdependencies between them. IFRS 15 Revenue from Contracts with Customers includes guidance on the combination of contracts, in particular that contracts with unrelated parties should not be combined. Notwithstanding the interdependencies, the Directors consider that the engine contract should be considered separately from the aftermarket contract. In making this judgement, they also took account of industry practice.

Key judgement – How performance on long-term aftermarket contracts should be measured

The Group generates a significant proportion of its revenue from aftermarket arrangements. These aftermarket contracts, such as TotalCare and CorporateCare agreements in the Civil Aerospace business, cover a range of services and generally have contractual terms covering more than one year. Under these contracts, the Group’s primary obligation is to maintain customers’ engines in an operational condition. This is achieved by undertaking various activities, such as maintenance, repair and overhaul, and engine monitoring over the period of the contract. Revenue on these contracts is recognised over the period of the contract and the basis for measuring progress is a matter of judgement. The Directors consider that the stage of completion of the contract is best measured by using the actual costs incurred to date compared to the estimated costs to complete the performance obligations, as this reflects the extent of completion of the activities to be performed.

Key judgement – Whether long-term aftermarket contracts contain a significant financing component

Long-term aftermarket contracts typically cover a period of eight to 15 years. Their pricing is the subject of negotiation with individual customers under competitive circumstances. It is the Directors’ judgement that the consideration received approximates to the cash selling price and any timing difference between consideration being received and the supply of goods and services is typical of the industry and arises for reasons other than to provide financing. The customers typically pay on an ‘as used’ basis (e.g. USD/EFH) which reflects the wear and tear of the engine as it flies and aligns to the customer’s own revenue streams. An adjustment to the transaction price is therefore not required.

Key judgement – Whether any costs should be treated as wastage

In rare circumstances, the Group may incur costs of wasted material, labour or other resources to fulfil a contract where the level of cost was not reflected in the contract price. The identification of such costs is a matter of judgement and would only be expected to arise where there has been a series of abnormal events which give rise to a significant level of cost of a nature that the Group would not expect to incur and hence is not reflected in the contract price. Examples include technical issues that: require resolution to meet regulatory requirements; have a wide-ranging impact across a product type; and cause significant operational disruption to customers. Similarly, in these rare circumstances, significant disruption costs to support customers resulting from the actual performance of a delivered good or service may be treated as a wastage cost. Provision is made for any costs identified as wastage when the obligation to incur them arises – see note 23.

Key judgement – Whether the Civil Aerospace LTSA contracts are warranty style contracts entered into in connection with OE sales and therefore can be accounted for under IFRS 15 Revenue from Contracts with Customers

The Group has considered whether these arrangements are insurance contracts as defined in IFRS 17 Insurance Contracts. While they may transfer an element of insurance risk, they relate to warranty and service type agreements that are entered into in connection with the Group’s sales of its goods or services and therefore continue to be accounted for under the existing revenue and provisions standards. The Directors have judged that such arrangements entered into after the original equipment sale remain sufficiently related to the sale of the Group’s goods and services to allow the contracts to continue to be measured under IFRS 15 Revenue from Contracts with Customers and IAS 37 Provisions, Contingent Liabilities and Contingent Assets.

Key judgement – Whether sales of spare engines to joint ventures are at fair value

The Civil Aerospace business maintains a pool of spare engines to support its customers. Some of these engines are sold to, and held by, joint venture companies. The assessment of whether the sales price reflects fair value is a key judgement. The Group considers that based upon the terms and conditions of the sales, and by comparison to the sales price of spare engines to other third parties, the sales made to joint ventures reflect the fair value of the goods sold. See note 28 for the value of sales to joint ventures during the year.

Key judgement – When revenue should be recognised in relation to spare engine sales

Revenue is recognised at the point in time when a customer obtains control of a spare engine. The customer could be a related party, an external operator or a spare engine service provider. Depending on the contractual arrangements, judgement is required on when the Group relinquishes control of spare engines and, therefore, when the revenue is recognised. The point of control passing has been concluded to correspond to the point of legal sale, even for instances where the customer is contracted to provide some future spare engine capacity to the Group to support its installed engine base. In such cases, the customer has responsibility for generating revenue from the engines and exposure to periods of non-utilisation; exposure to risk of damage or loss, risk from residual value movements, and will determine if and when profits will be made from disposal. The spare engine capacity that will be made available to the Group in the future does not consist of identified assets and the provider retains a substantive right to substitute the asset through the Group’s period of use. It is, therefore, appropriate to recognise revenue from the sale of the spare engines at the point that title transfers. During 2025, of the total 52 (2024: 57) large spare engine sales delivered, 5 (2024: 20) engines were sold to customers where contractual arrangement allows for some future spare engine capacity to be used by the Group. These sales contributed £94m (2024: £399m) to revenue for the year.

Key estimate – Estimates of future revenue, including customer pricing, and costs of long-term contractual arrangements, including the impact of climate change

The Group has long-term contracts that fall into different accounting periods and which can extend over significant periods (generally up to 25 years), the most significant of these are LTSAs in the Civil Aerospace business, with contracts typically covering a period of eight to 15 years. The estimated revenue and costs are inherently imprecise and significant estimates are required to assess: EFHs, time on wing and other operating parameters; the pattern of future maintenance activity and the costs to be incurred; lifecycle cost improvements over the term of the contracts; and escalation of revenue and costs (that includes the impact of inflation). Many of the revenues and costs are denominated in currencies other than that of the relevant group undertaking, these are translated at an estimated long-term exchange rate, based on historical trends and economic forecasts.

The impact of climate change on EFHs and costs is also considered when making these estimates. Industry and customer data on expected levels of utilisation is included in the forecasts used. Across the length of the current Civil Aerospace LTSA contracts, allowance has been made for around a 1% (2024:1%) projected cost increase resulting from carbon pricing and commodity price changes.

During the year, changes to the estimate in relation to the Civil Aerospace long term contracts resulted in favourable catch-up adjustments to revenue of £253m (2024: favourable catch-up adjustments of £311m).

The sensitivities below demonstrate how changes in assumptions (including as a result of climate change) could impact the level of revenue recognised were assumptions to change. The Directors believe that the estimates used to prepare the Consolidated Financial Statements take account of the inherent uncertainties, constraining the expected level of revenue as appropriate. Based upon the stage of completion of all LTSA contracts within Civil Aerospace as at 31 December 2025, the following reasonably possible changes in estimates would result in catch-up adjustments being recognised in the period in which the estimates change (at underlying rates):

- A change in forecast EFHs of 1% over the remaining term of the contracts would impact LTSA income and to a lesser extent costs, resulting in an in-year impact of around £20m. This would be expected to be seen as a catch-up change in revenue or, to the extent it impacts onerous contracts, within cost of sales.

- A 2% increase or decrease in our pricing to customers over the life of the contracts would lead to a revenue catch-up adjustment in the next 12 months of around £400m.

- A 2% increase or decrease in shop visit costs over the life of the contracts would lead to a revenue catch-up adjustment in the next 12 months of around £120m.

Risk and revenue sharing arrangements (RRSAs)

Cash entry fees received are initially deferred on the balance sheet as deferred receipts from RRSA workshare partners within trade payables and other liabilities. The cash entry fee is a transaction with a supplier and is recognised as a reduction in cost of sales incurred. Individual programme amounts are allocated pro rata to the estimated number of units to be produced. Amortisation commences as each unit is delivered and then recognised on a 15-year straight-line basis.

The payments to suppliers of their shares of the programme cash flows for their production components are charged to cost of sales when OE sales are recognised or as LTSA costs are incurred. These prepayments are initially recognised within trade receivables and other assets.

The Group also has arrangements with third parties who invest in a programme and receive a return based on its performance, but do not undertake development work or supply parts. Such arrangements (financial RRSAs) are financial instruments as defined by IAS 32 Financial Instruments: Presentation and are accounted for using the amortised cost method.

Key judgement – Determination of the nature of entry fees received

RRSAs with key suppliers (workshare partners) are a feature of the civil aviation industry. Under these contractual arrangements, the key commercial objectives are that: (i) during the development phase the workshare partner shares in the risks of developing an engine by performing its own development work, providing development parts, and paying a non-refundable cash entry fee; and (ii) during the production phase the workshare partner supplies components in return for a share of the programme cash flows as a ‘life of type’ supplier (i.e. as long as the engine remains in service).

The non-refundable cash entry fee is considered to be one element of a long-term supply agreement. These receipts are deferred on the balance sheet and recognised against the cost of sales over the estimated number of units to be delivered on a similar basis to the amortisation of development costs – see page 129.

Government grants

Government grants received are varied in nature and are recognised in the income statement so as to match them with the related expenses that they are intended to compensate. Where grants are received in advance of the related expenses, they are initially recognised as liabilities within trade payables and other liabilities and released to match the related expenditure. Non-monetary grants are recognised at fair value.

Interest

Interest receivable/payable is credited/charged to the income statement using the effective interest method. Where borrowing costs are attributable to the acquisition, construction or production of a qualifying asset, such costs are capitalised as part of the specific asset.

2 Segmental analysis (extract)

Disaggregation of revenue from contracts with customers

Analysis by type and basis of recognition

Analysis by geographical destination

The Group’s revenue by destination of the ultimate operator is as follows:

Order backlog

Contracted consideration, translated at the estimated long-term exchange rates, that is expected to be recognised as revenue when performance obligations are satisfied in the future (referred to as order backlog) is as follows:

The parties to these contracts have approved the contract and customers do not have a unilateral enforceable right to terminate the contract without compensation. The Group excludes Civil Aerospace OE orders (for deliveries beyond the next seven to 12 months) that customers have placed where they retain a right to cancel. The Group’s expectation based on historical experience is that these orders will be fulfilled. Civil Aerospace order backlog has increased by £4.7bn, this is due to new aftermarket contracts and contract extensions. Other drivers include commercial optimisation and revenue escalation with major customers. The Civil order backlog will be recognised over the contract term. The £1.3bn increase within Power Systems is mainly driven by orders for power generation (from the growth in data centres) and governmental, which will be mainly recognised over the next three years.

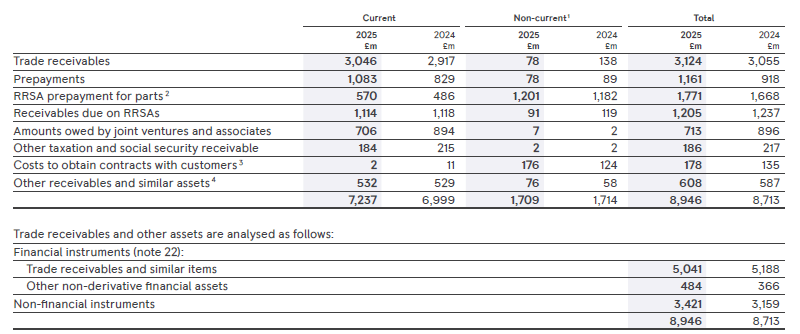

16 Trade receivables and other assets

1 Trade receivables and other assets have been presented on the face of the balance sheet in line with the operating cycle of the business. Further disclosure is included in the table above and relates to amounts not expected to be received in the next 12 months, in line with specific customer payment arrangements, including customers on payment plans

2 These amounts reflect the contractual share of EFH flows and original equipment deposits from customers paid to RRSA partners in return for the supply of parts in future periods under long-term supply contracts. During the year £597m (2024: £262m) has been charged to cost of sales in relation to parts supplied and used in the year

3 These are amortised over the term of the related contract in line with engine deliveries, resulting in amortisation of £10m (2024: £8m) in the year. There were no impairment losses

4 Other receivables includes unbilled recoveries relating to completed overhaul activity where the right to consideration is unconditional

The Group has adopted the simplified approach to provide for expected credit losses (ECLs), measuring the loss allowance at a probability weighted amount incorporated by using credit ratings which are publicly available, or through internal risk assessments derived using the customer’s latest available financial information.

The ECLs for trade receivables and other financial assets has decreased by £7m to £232m (2024: decreased by £3m to £239m).

The assumptions and inputs used for the estimation of the ECLs are disclosed in the table below:

1 During the year, there has been a change to the classification used for investment gradings. In 2024, the ratings were reported using credit ratings C and above, credit ratings C and below and without credit rating. In 2025, the ratings have been reported using credit rating BBB- and above, credit rating below BBB- and without credit rating

The movements of the Group ECLs provision are as follows:

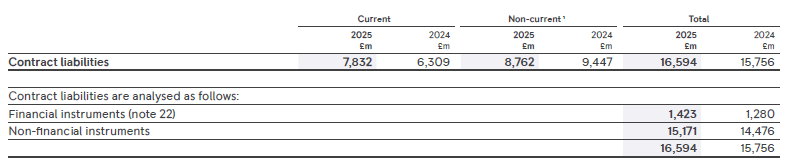

17 Contract assets and liabilities

1 Contract assets have been presented on the face of the balance sheet in line with the operating cycle of the business. Further disclosure of contract assets is provided in the table above, which shows within current the element of consideration that will become unconditional in the next year

2 Contract assets are classified as non-financial instruments

The balance includes £973m (2024: £955m) Civil Aerospace LTSA assets and £477m (2024: £381m) Defence LTSA assets.

The increase in the Civil Aerospace balance is driven by revenue recognised (when performance obligations have been completed during the year) being greater than the amount invoiced on those contracts that have a contract asset balance. Revenue recognised relating to performance obligations satisfied in previous years was £36m which reduced the contract asset (2024: reduction of £42m) in Civil Aerospace.

No impairment losses in relation to these contract assets (2024: none) have arisen during the year.

Participation fee contract assets have decreased by £12m (2024: increased by £102m) primarily due to amortisation of £(20)m (2024: £(23)m) and the Civil Aerospace programme asset impairment reversal of £nil (2024: £132m), offset by foreign exchange on consolidation of £8m (2024: £(7)m).

The absolute value of ECLs for contract assets has increased by £1m to £12m (2024: increased by £5m to £11m).

1 Contract liabilities have been presented on the face of the balance sheet in line with the operating cycle of the business. Contract liabilities are further split according to when the related performance obligation is expected to be satisfied and, therefore, when revenue is estimated to be recognised in the income statement

During the year, £5,562m (2024: £5,048m) of the opening contract liability was recognised as revenue.

Contract liabilities have increased by £838m. The movement in the Group balance is primarily as a result of an increase in Civil Aerospace of £576m. This is mainly a result of growth in LTSA liabilities of £231m (2025: £11,370m, 2024: £11,139m) driven almost wholly by large engines, with customer invoicing in 2025 (based on EFH) being in advance of revenue recognised (based on costs incurred completing performance obligations). The contract liability movement includes a decrease of £289m (2024: decrease of £354m) as a result of revenue being recognised in relation to performance obligations satisfied in previous years. Contract liability increases in Defence of £180m and Power Systems of £90m is from the receipt of deposits in advance of performance obligations being completed.