Anglo–Eastern Plantations Plc – Annual report – 31 December 2016

Industry: agriculture

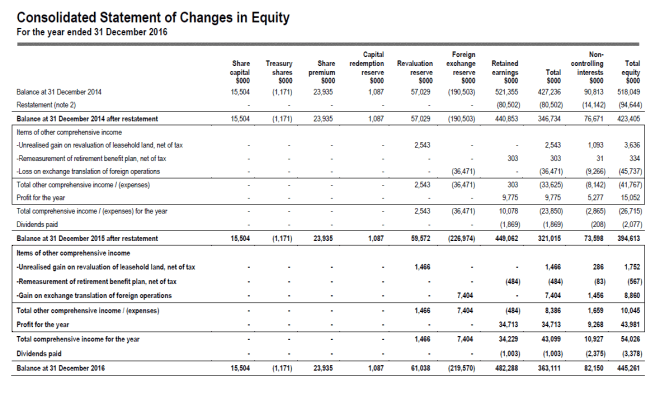

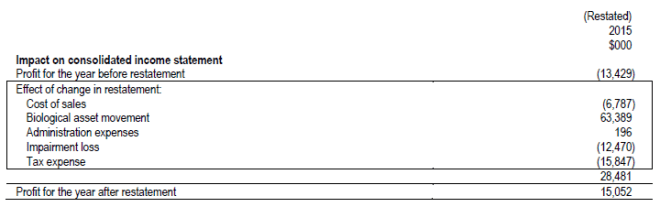

2 Prior year restatement

The amendments to IAS 16 and the amendments to IAS 41, which came into effect on 1 January 2016, require Biological Assets that meet the definition of bearer plants to be accounted for as Property, Plant and Equipment in accordance with IAS 16, adopting either a cost model or a revaluation model. This required retrospective application.

As the Biological Assets of the Group fall within the definition of bearer plants, with effect from 1 January 2016 the immature plants are stated at accumulated cost until maturity, subject to impairment reviews, and the mature plantations are stated at historical cost less accumulated depreciation. The unharvested FFB, which is agricultural produce under the revised IAS 41, are recognised as Biological Assets and are stated at fair value less cost to sell at the point of harvest, with changes recognised in profit and loss. This has resulted in the accounts for the year ended 31 December 2015 being restated.

The effects of the restatements are summarised as follows:

The effect of the prior year adjustments had a negative impact on the earnings per share before BA of 43.50cts and a positive impact on the earnings per share after BA of 62.24cts for the year to 31 December 2015.

The prior year restatement has changed from that reported in the interim financial statements as the figures have now been subject to audit.