Ferguson plc – Annual report – 31 July 2019

Industry: distribution

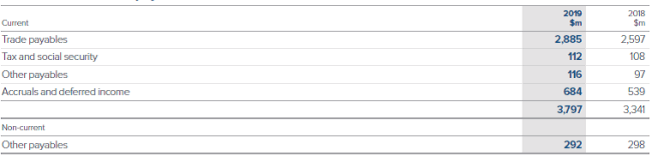

20 – Trade and other payables

Trade payables are stated net of $44 million (2018: $32 million) due from suppliers with respect to supplier rebates where an agreement exists that allows these to be net settled.

Accruals and deferred income includes $159 million (2018: $nil) payable in relation to the irrevocable and non-discretionary share buy back programme announced in July 2019.

25 – Share capital (extract)

ii) Treasury shares

The shares purchased under the Group’s buy back programmes have been retained in issue as Treasury shares and represent a deduction from equity attributable to shareholders of the Company.

On 9 May 2019, prior to the Scheme of Arrangement, all Treasury shares held by Old Ferguson were cancelled.

On 10 June 2019, the Group announced a $500 million share buy back programme. As at 31 July 2019, ordinary shares had been purchased for a consideration of $150 million and a further purchase of $159 million was irrevocably committed to.

A summary of the movements in Treasury shares in the year is detailed in the following table:

Consideration received in respect of shares transferred to participants in certain long-term incentive plans and all-employee plans amounted to $3 million (2018: $24 million).

Directors’ Report – other disclosures (extract)

Authority to purchase shares (extract)

At the 2018 AGM of Old Ferguson, authority was given to the Directors to purchase the Company’s ordinary shares. This authority was adopted by shareholders of the Company on 25 April 2019 and the Directors were given authority to purchase up to 23,185,045 of the Company’s ordinary shares of 10 pence each (with such purchases being subject to minimum and maximum price conditions). This authority to purchase the Company’s shares will expire at the 2019 AGM.

On 10 June 2019, the Company announced a $500 million share repurchase programme (the “2019 Buy Back Programme”). The purpose of the 2019 Buy Back Programme was to reduce the issued capital of Ferguson plc. As at 31 July 2019, 2,090,371 ordinary shares of 10 pence each had been purchased for a consideration of $150 million representing 0.90 per cent of the issued share capital of the Company as at 31 July 2019. All shares purchased were held in Treasury. On 31 July 2019 the Company entered into an irrevocable and non-discretionary arrangement with its broker Barclays Capital Securities Limited (“Barclays”), to continue with the 2019 Buy Back Programme after the year end, which concluded on 24 September 2019. During this period, Barclays acted as principal and made trading decisions concerning the timing of the purchases of the Company’s shares independently of the Company. Additional details concerning the 2019 Buy Back Programme can be found in note 25 to the consolidated financial statements. Details of shares that were acquired by the Company in previous financial years that were held or disposed of during the financial year ended 31 July 2019 are provided in note 25 to the consolidated financial statements on pages 144 and 145.