Givaudan SA – Annual report – 31 December 2016

Industry: manufacturing

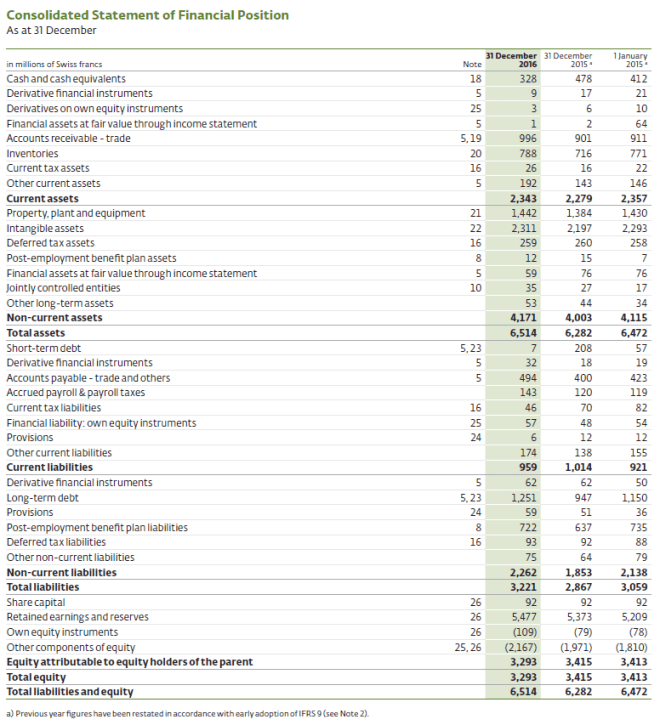

Notes to the consolidated financial statements (extract)

2.1.1 Changes in Accounting Policies and Disclosures (extract)

IFRS 9 Financial Instruments addresses the classification, measurement and derecognition of financial assets and financial liabilities and introduces new rules for hedge accounting. As at 1 January 2016, the Group has early adopted IFRS 9 as issued in July 2014. As a result of the adoption of IFRS 9, the Group classifies all financial assets as financial assets at fair value through the income statement except for trade receivables which are classified at amortised cost.

The adoption of IFRS 9 helps to align the accounting of financial assets with the objectives to collect contractual cash flows as they come due and to sell financial assets.

Financial assets at fair value through the income statement

Financial assets that are used to fund the settlements of long-term incentive plans recognised in the liabilities fulfil the objectives of collecting contractual cash flows and selling financial assets. Investments accounted for as available-for-sale financial assets in accordance with IAS 39 change their measurement category to “at fair value through the income statement” which is more consistent, in the Group’s opinion, with the Group’s strategic investments objectives.

Derivative financial assets accounted for at fair value through the income statement in accordance with IAS 39 remain in the same measurement category unless they are designated as effective hedging instruments.

Financial assets at amortised cost

Trade receivables reach the objective of collecting contractual cash flows over their life. Trade receivables accounted for as “loans and receivables” financial assets in accordance with IAS 39 change their measurement category to “at amortised cost”.

The new hedging rules align hedge accounting more closely with the Group’s risk management practices. The hedging strategy of the Group is not changed.

The new impairment model is an expected credit loss (ECL) model which may result in the earlier recognition of credit losses than the incurred loss impairment model used in IAS 39. The Group applies a simplified approach for trade receivables, for which the tracking of changes in credit risk is not required but instead the base lifetime expected credit loss at all times is applied. The current practice for measuring the trade receivables does not change.

For financial liabilities, there is no change in their classification and measurement except for liabilities designated at fair value through the income statement for which the amount of change in the fair value that is attributable to changes in own credit risk is presented in other comprehensive income. The Group has currently only financial liabilities at amortised cost and therefore there is no impact in their classification.

The following tables summarise the impact of the above changes on the Group’s financial position, on the statement of comprehensive income, and on earnings per share.