Balfour Beatty plc – Annual report – 31 December 2025

Industry: construction; support services

2 Principal accounting policies (extract)

2.4 Revenue recognition

The Group recognises revenue when it transfers control over a product or service to its customer. Revenue is measured based on the consideration specified in a contract with a customer and excludes amounts collected on behalf of third parties. Where consideration is not specified within the contract and is therefore subject to variability, the Group estimates the amount of consideration to be received from its customer. The consideration recognised is the amount which is highly probable not to result in a significant reversal in future periods.

Where a modification to an existing contract occurs, the Group assesses the nature of the modification and whether it represents a separate performance obligation required to be satisfied by the Group or whether it is a modification to the existing performance obligation.

The Group does not expect to have any contracts where the period between the transfer of the promised goods or services to the customer and payment by the customer exceeds one year. As a consequence, the Group does not adjust its transaction price for the time value of money.

The Group’s activities are wide ranging, and as such, depending on the nature of the product or service delivered and the timing of when control is passed onto the customer, the Group will account for revenue over time and at a point in time. Where revenue is measured over time, the Group uses the input method to measure progress of delivery.

Revenue is recognised as follows:

- revenue from construction and services activities is recognised over time and the Group uses the input method to measure progress of delivery;

- revenue from manufacturing activities is recognised at a point in time when title has passed to the customer; and

- dividend income in the Parent Company is recognised when the equity holders’ right to receive payment is established.

2.5 Construction and services contracts

When the outcome of individual contracts can be estimated reliably, contract revenue is recognised by reference to the measure of progress at the reporting date using the input method. Costs are recognised as incurred and revenue is recognised on the basis of the proportion of total costs at the reporting date to the estimated total costs of the contract.

Estimates of the final out-turn on each contract may include cost contingencies to take account of the specific risks within each contract that have been identified during the early stages of the contract. The cost contingencies are reviewed on a regular basis throughout the contract life and are adjusted where appropriate. However, the nature of the risks on contracts are such that they often cannot be resolved until the end of the project and therefore may not reverse until the end of the project. The estimated final out-turns on contracts are continuously reviewed and, in certain limited cases, recoveries from insurers are assessed, and adjustments made where necessary.

No margin is recognised until the outcome of the contract can be estimated with reasonable certainty. Provision is made for all known or expected losses on individual contracts once such losses are foreseen.

Revenue in respect of variations to contracts and incentive payments is recognised when there is an enforceable right to payment and it is highly probable it will be agreed by the customer. Variable consideration is assessed on a contract-by-contract basis according to the facts, circumstances and terms of each project and only recognised to the extent that it is highly probable not to significantly reverse in the future. Revenue in respect of claims is recognised only if it is highly probable not to reverse in future periods. Profit for the year includes the benefit of claims settled in the year to the extent not previously recognised on contracts completed in previous years.

2.7 Pre-contract bid costs and recoveries

Pre-contract costs are expensed as incurred until preferred bidder status is awarded at which point further costs are capitalised as there is a high probability that the Group would be able to recover these costs. Amounts subsequently recovered in respect of pre-contract costs that have been written off before preferred bidder status was awarded are recognised in full in the income statement when they are received in cash.

2.28 Judgements and key sources of estimation uncertainty (extracts)

a) Revenue and margin recognition (estimate)

The Group’s revenue recognition and margin recognition policies, which are set out in Notes 2.4 and 2.5, are central to how the Group values the work it has carried out in each financial year.

These policies require forecasts to be made of the outcomes of long-term construction services and support services contracts, which require estimates to be made of both cost and income recognition on each contract. On the cost side, estimates of forecasts are made on the final out-turn of each contract in addition to potential costs to be incurred for any maintenance and defects liabilities. On the income side, estimates are made on variations to consideration which typically include variations due to changes in scope of work, recoveries of claim income from customers, and potential liquidated damages that may be levied by customers. On cost reimbursable contracts there are also estimates required on the level of disallowable costs which requires an assessment of whether costs are recoverable under the terms of the contract and therefore should be recognised as income. Estimates are reviewed regularly throughout the contract life based on latest available information and adjustments are made where necessary. The Group continues to regularly assess these estimates.

As at 31 December 2025, the Group’s contract assets, contract liabilities and contract provisions amounted to £238m, £1,063m and £514m respectively as set out in Notes 24 and 27. The Group has considered the nature of the estimates involved in deriving these balances and concluded that it is possible, on the basis of existing knowledge, that outcomes within the next financial year may be different from the Group’s assumptions applied as at 31 December 2025 and could require a material adjustment to the carrying amounts of these assets and liabilities in the next financial year. However, due to the level of uncertainty, combination of cost and income variables and timing across a large portfolio of contracts (in excess of 1,000) at different stages of their contract life, it is impracticable to provide a quantitative analysis of the aggregated estimates that are applied at a portfolio level.

Within this portfolio, there are a limited number of long-term contracts where the Group has incorporated significant estimates over contractual entitlements relating to recoveries of claim income from customers, suppliers and liquidated damages levied by the customer. This is in the Construction Services segment. These recoveries have been recognised at the amount that is considered highly probable not to significantly reverse. However, there are a host of factors affecting potential outcomes in respect of these entitlements which could result in a range of reasonably possible outcomes on these contracts in the following financial year, ranging from a gain of £82m to a loss of £44m. The Directors have assessed the range of reasonably possible outcomes on these limited number of contracts based on facts and circumstances that were present and known at the balance sheet date. As with any contract applying long-term contract accounting, these contracts are also affected by a variety of uncertainties that depend on future events, and so often need to be revised as contracts progress.

d) Contract provisions (estimate)

Contract provisions are liabilities of uncertain timing or amount and therefore in making a reliable estimate of the quantum and timing of liabilities estimates are applied and re-evaluated at each reporting date. The range of potential outcomes on contract provisions as a result of uncertain future events could result in a materially positive or negative swing to profitability and cash flow.

The Group has considered the nature of these estimates and concluded that it is possible, on the basis of existing knowledge, that outcomes within the next financial year may be different from the Group’s assumptions applied as at 31 December 2025 and could require a material adjustment to the carrying amounts of assets and liabilities in the next financial year. As disclosed in Note 27, the majority of the Group’s provision balance relates to contract provisions, which include loss provisions, defect and warranty provisions, where estimates are made around forecast costs, timing and whether it is probable there will be an outflow of future economic benefit. Contract loss provisions may also include estimates around variable consideration as disclosed in Note 2.28(a). However, due to the level of uncertainty, combination of variables and timing across a large portfolio of complex contracts at different stages of their contract life, it is impracticable to provide a quantitative analysis of the aggregated estimates that are applied at a portfolio level.

To the extent that the sensitivities disclosed in Note 2.28(a) affect a loss-making contract, this will have an impact on the Group’s provisions in the next financial year.

The Group also continues to provide for a number of fire safety-related claims received by the Group as part of its defects provision. A provision is made when there is a probable obligation and outflow, and the Group can reliably estimate the cost relating to its obligation. If costs are considered possible or cannot be reliably estimated, then they are considered to be contingent liabilities (see Note 38). Provisions of this nature are inherently uncertain as the estimated costs are based on a number of key estimates and assumptions which include, but are not limited to, the extent of defects that may exist, the cost of rectifying these defects and the consideration of what was considered to comply with building safety regulations at the time these buildings were constructed. These estimates are also inherently uncertain due to the highly complex and bespoke nature of each building. The Directors have used various externally available information and internal assessments as a basis for the estimated remedial costs for the fire safety claims received to date. The actual costs will ultimately be subject to the progression of investigative works, remedial works carried out, settlements of ongoing claims, and the evolution of current legislation and regulation which will impact the scope of any remediation works required, and therefore it is impracticable to provide a quantitative analysis of the aggregated estimates across the Group for these fire safety-related claims. There are also potential avenues to recovering a portion of these costs from third parties, which have not been recognised by the Group at this stage.

Within the fire defect population, there are claims received under the retrospective Building Safety Act (BSA) legislation introduced in 2022 (refer to Note 10.2.2) for which the Group is carrying a defect provision amounting to £85m at 31 December 2025 (2024: £82m). If the forecast remediation costs relating to BSA claims received to date were 25% higher / lower than provided, the pre-tax non-underlying charge in the Group’s income statement would increase / decrease by £21m. However, if further BSA claims are notified, this could also increase the required provision, but the potential quantity and timing of this change cannot be readily determined without further claims being made against the Group and, subsequently, the necessary investigative work being conducted on these claims. The scope of buildings and remediation works to be considered may also change as legislation and regulations continue to evolve relating to BSA.

The Group continues to regularly assess these estimates.

4 Revenue

4.1 Nature of services provided

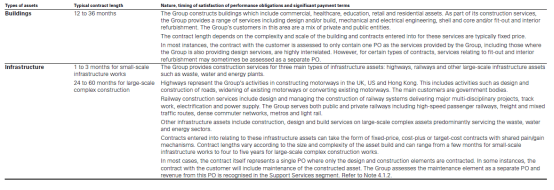

4.1.1 Construction Services

The Group’s Construction Services segment encompasses activities in relation to the physical construction of assets provided to public and private customers. Revenue generated in this segment is measured over time as control passes to the customer as the asset is constructed. Progress is measured by reference to the cost incurred on the contract to date compared to the contract’s end of job forecast (the input method). Payment terms are based on a schedule of value that is set out in the contract and fairly reflect the timing and performance of service delivery. Contracts with customers are typically accounted for as one performance obligation (PO).

4.1.2 Support Services

The Group’s work in this segment supports existing assets through maintaining, upgrading and managing services across utilities and infrastructure assets. Revenue generated in this segment is measured over time as control passes to the customer as and when services are provided. Progress is measured by reference to the cost incurred on the contract to date compared to the contract’s end of job forecast (the input method). Payments are structured as milestone payments set out in the respective contracts.

4.1.3 Infrastructure Investments

The Group invests directly in a variety of assets, predominantly consisting of infrastructure assets where there are opportunities to manage the asset upon completion of construction. The Group also invests in real estate-type assets, in particular private residential and student accommodation assets. Revenue generated in this segment is from the provision of construction, maintenance and management services and also from the recognition of rental income. The Group’s strategy is to hold these assets until optimal values are achieved through disposal of mature assets.

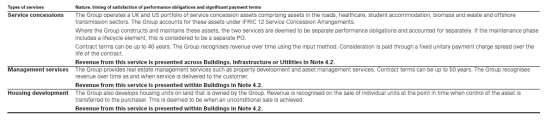

4.2 Disaggregation of revenue

The Group presents a disaggregation of its revenue according to the primary geographical markets in which the Group operates as well as the types of assets serviced by the Group. The nature of the various services provided by the Group is explained in Note 4.1. This disaggregation of revenue is also presented according to the Group’s reportable segments as described in Note 5.

For the year ended 31 December 2025

+ Includes rental income of £57m including share of joint ventures and associates or £32m excluding share of joint ventures and associates.

For the year ended 31 December 2024

+ Includes rental income of £48m including share of joint ventures and associates or £26m excluding share of joint ventures and associates.

4.3 Transaction price allocated to the remaining performance obligations (excluding joint ventures and associates)

The total transaction price allocated to the remaining performance obligations represents the contracted revenue to be earned by the Group for distinct goods and services which the Group has promised to deliver to its customers. These include promises which are partially satisfied at the period end or those which are unsatisfied but which the Group has committed to providing. In deriving this transaction price, any element of variable revenue is estimated at a value that is highly probable not to reverse in the future. The transaction price above does not include any estimated revenue to be earned on framework contracts for which a firm order or instruction has not been received from the customer.

24 Contract balances

The timing of revenue recognition, billings and cash collection results in trade receivables (billed amounts), contract assets (unbilled amounts) and customer advances and deposits (contract liabilities) on the Group’s balance sheet. For services in which revenue is earned over time, amounts are billed in accordance with contractual terms, either at periodic intervals or upon achievement of contractual milestones. The timing of revenue recognition is measured in accordance with the progress of delivery on a contract which could either be in advance or in arrears of billing, resulting in either a contract asset or a contract liability.

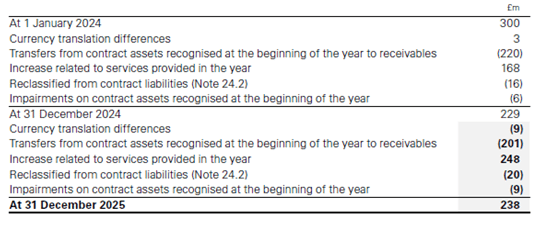

24.1 Contract assets

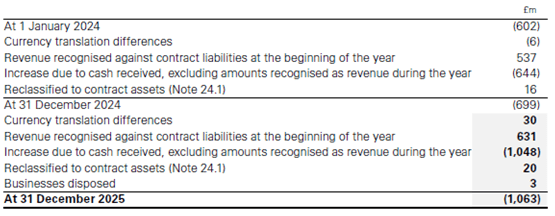

24.2 Contract liabilities

The amount of revenue recognised in the year from performance obligations satisfied (or partially satisfied) in previous periods amounted to £1m (2024: £2m).

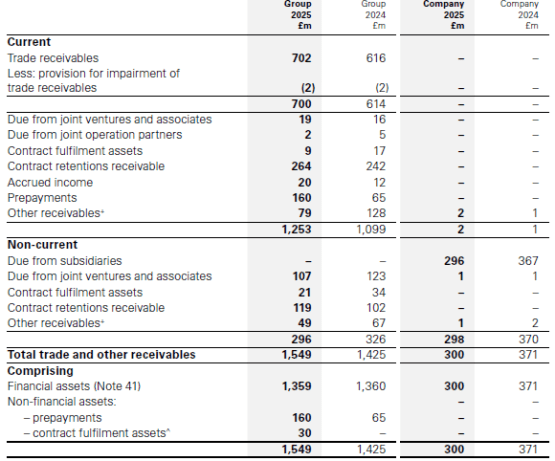

25 Trade and other receivables (extract)

+ Includes insurance recoveries recognised in relation to rectification works on a development in London (Note 10.2).

^ Contract fulfilment assets have been presented as a non-financial asset in 2025. This was previously presented as a financial asset in 2024 and has not been re-presented in the comparative period as the Directors do not consider this to be material.

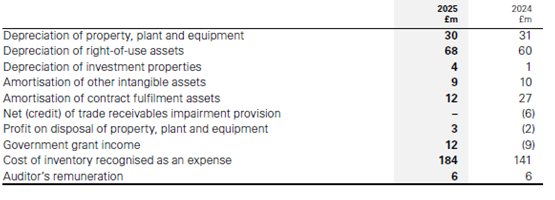

6 Profit/(loss) from operations (extract)

6.1 Profit/(loss) from operations is stated after charging/(crediting)