Samsung Electronics Co., Ltd. – Annual report – 31 December 2024

Industry: manufacturing

28. Financial Risk Management (extract)

(F) Fair value measurement (extract)

(2) Fair value hierarchy classifications of the financial instruments that are measured at or only disclosed their fair value as of December 31, 2024 and 2023 are as follows:

The levels of the fair value hierarchy and its application to financial assets and liabilities are described below.

- Level 1: Quoted prices (unadjusted) in active markets for identical assets or liabilities

- Level 2: Inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly

- Level 3: Inputs for the asset or liability that are not based on observable market data (that is, unobservable inputs)

The fair value of financial instruments traded in active markets is based on quoted market prices at the reporting date. A market is regarded as active if quoted prices are readily and regularly available from an exchange, dealer, broker, industry group, pricing service, or regulatory agency, and those prices represent actual and regularly occurring market transactions on an arm’s length basis. These instruments are included in Level 1. The instruments included in Level 1 are listed equity investments, most of which are classified as financial assets at fair value through other comprehensive income.

The fair value of financial instruments that are not traded in an active market is determined by using valuation techniques. These valuation techniques maximize the use of observable market data where available and rely as little as possible on entity-specific estimates. If all significant inputs required to measure the fair value of an instrument are observable, the instrument is included in Level 2.

If one or more of the significant inputs are not based on observable market data, the instrument is included in Level 3.

The Company performs the fair value measurements required for financial reporting purposes, including Level 3 fair values, and discusses valuation processes and results in line with the financial reporting timelines. The Company’s policy is to recognize transfers between levels at the end of the reporting period if corresponding events or changes in circumstances have occurred.

Specific valuation techniques used to value financial instruments include:

- Quoted market prices or dealer quotes for similar instruments

- The fair value of forward foreign exchange contracts is determined using forward exchange rates at the reporting date, with the resulting value discounted to present value

Other techniques, such as discounted cash flow analysis, binomial distribution model, etcetera, are used to determine fair value for the remaining financial instruments. For trade and other receivables that are classified as current assets, the book value approximates a reasonable estimate of fair value.

(3) Valuation technique and the inputs

The Company utilizes a present value technique to discount future cash flows using proper interest rates for corporate bonds, government and public bonds, and bank debentures that are classified as Level 2 in the fair value hierarchy.

The following table presents the valuation technique and the inputs used for major financial instruments classified as Level 3 as of December 31, 2024.

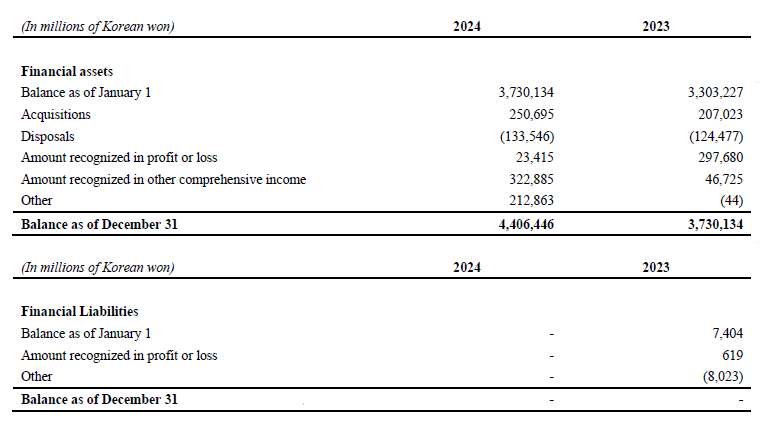

(4) Changes in Level 3 instruments for the years ended December 31, 2024 and 2023 are as follows:

(5) Sensitivity analysis for recurring fair value measurements categorized within Level 3

Sensitivity analysis of financial instruments is performed to measure favorable and unfavorable changes in the fair value of financial instruments which are affected by the unobservable parameters, using a statistical technique. When the fair value is affected by more than two input parameters, the amounts represent the most favorable or unfavorable.

The results of the sensitivity analysis for effect on income or loss before tax from changes in inputs for major financial instruments which are categorized within Level 3 and subject to sensitivity analysis are as follows:

(*1) For equity securities, changes in fair value are calculated by increasing or decreasing perpetual growth rate and weighted average cost of capital (-1.0%~1.0%), which are significant unobservable inputs.

(*2) Changes in fair value were calculated by increasing or decreasing underlying asset price (20%) and price volatility (10%), which are significant unobservable inputs.