Smurfit Kappa Group plc – Half year report – 30 June 2019

Industry: packaging

Notes to the Condensed Consolidated Interim Financial Statements (extract)

3. Changes in Significant Accounting Policies

IFRS 16, Leases, issued in January 2016 by the IASB replaces IAS 17, Leases, and related interpretations. IFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases for both the lessee and the lessor. For lessees, IFRS 16 eliminates the classification of leases as either operating leases or finance leases and introduces a single lessee accounting model with some exemptions for short-term and low-value leases. The lessee recognises a right-of-use asset representing its right to use the underlying asset and a lease liability representing its obligation to make lease payments.

The Group has adopted IFRS 16 using the modified retrospective approach, with the date of initial application of 1 January 2019. Under this method, the impact of the standard is calculated retrospectively, however, the cumulative effect arising from the new leasing rules is recognised in the opening balance sheet at the date of initial application. Accordingly, the comparative information presented for 2018 has not been restated.

The Group’s leasing activities and how these are accounted for

The Group leases a range of assets including property, plant and equipment and vehicles.

As a lessee, the Group previously classified leases as operating or finance leases based on its assessment of whether the lease transferred substantially all of the risks and rewards of ownership. Payments made under operating leases (net of any incentives received from the lessor) were charged to profit or loss on a straight-line basis over the period of the lease. Under IFRS 16, the Group applies a single recognition and measurement approach for all leases, except for short-term and low-value assets and recognises right-of-use assets and lease liabilities.

The Group presents right-of-use assets in ‘property, plant and equipment’, in the same line item as it presents underlying assets of the same nature that it owns. The carrying amounts of right-of-use assets are as below.

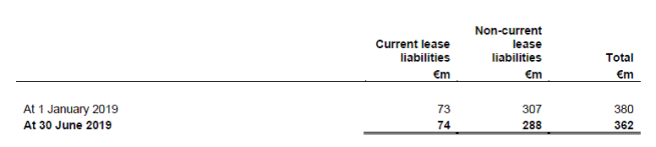

The Group presents lease liabilities in ‘borrowings’ in the balance sheet. The carrying amounts of lease liabilities are as below.

Significant accounting policies

Under IFRS 16, a contract is, or contains a lease if the contract conveys a right to control the use of an identified asset for a period of time in exchange for consideration. The Group recognises a right-of-use asset and a lease liability at the lease commencement date.

The right-of-use asset is initially measured at cost, and subsequently at cost less any accumulated depreciation and impairment losses and adjusted for certain remeasurements of the lease liability. The cost of right-of-use assets includes the amount of lease liabilities recognised, initial direct costs incurred, restoration costs and lease payments made at or before the commencement date less any lease incentives received. The right-of-use asset is depreciated on a straight-line basis over the shorter of its estimated useful life and the lease term. Where the lease contains a purchase option the asset is written off over the useful life of the asset when it is reasonably certain that the purchase option will be exercised. Right-of-use assets are subject to impairment testing.

The lease liability is initially measured at the present value of certain lease payments to be made over the lease term. The lease payments include fixed payments (including in-substance fixed payments) less any lease incentives receivable, variable lease payments that depend on an index or a rate, and amounts expected to be paid under residual value guarantees. The lease payments also include the exercise price of a purchase option reasonably certain to be exercised by the Group and payments of penalties for terminating a lease, if the lease term reflects the Group exercising the option to terminate. The variable lease payments that do not depend on an index or a rate are recognised as an expense in the period in which the event or condition that triggers the payment occurs. The Group has elected to avail of the practical expedient not to separate lease components from any associated non-lease components.

The lease payments are discounted using the lessee’s incremental borrowing rate as the interest rate implicit in the lease is generally not readily determinable.

After the commencement date, the lease liability is subsequently increased by the interest cost on the lease liability and decreased by the lease payments made. It is remeasured when there is a change in future lease payments arising from a change in an index or rate, a change in the estimate of the amount expected to be payable under a residual value guarantee, or as appropriate, changes in the assessment of whether a purchase or extension option is reasonably certain to be exercised or a termination option is reasonably certain not to be exercised.

The Group has elected to apply the recognition exemptions for short-term and low-value leases and recognises the lease payments associated with these leases as an expense in profit or loss on a straight-line basis over the lease term. Short-term leases are leases with a lease term of 12 months or less. Low-value assets comprise certain items of IT equipment and small items of office furniture.

Significant accounting judgements

The Group has applied judgement to determine the lease term for some lease contracts in which it is a lessee that include renewal options. The assessment of whether the Group is reasonably certain to exercise such options impacts the lease term, which significantly affects the amount of lease liabilities and right-of-use assets recognised.

Transition

On transition to IFRS 16, the Group has elected to apply the practical expedient to grandfather the assessment of which transactions are leases. It applied IFRS 16 only to contracts that were previously identified as leases. Contracts that were not identified as leases under IAS 17 and IFRIC 4 were not reassessed.

At transition, for leases classified as operating leases under IAS 17, lease liabilities were measured at the present value of the remaining lease payments, discounted at the lessee’s incremental borrowing rate as at 1 January 2019. Right-of-use assets were measured at either:

• their carrying amount as if IFRS 16 had been applied since the commencement date, discounted using the lessee’s incremental borrowing rate at the date of initial application – the Group applied this approach for certain property leases; or

• an amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments – the Group applied this approach to all other leases.

The Group applied the following practical expedients when applying IFRS 16 to leases previously classified as operating leases under IAS 17.

• Excluded initial direct costs from measuring the right-of-use asset at the date of initial application.

• Used hindsight when determining the lease term if the contract contains options to extend or terminate the lease.

• Relied on its assessment of whether leases are onerous under IAS 37 immediately before the date of initial application to meet the impairment requirement.

For leases previously classified as finance leases under IAS 17, the carrying amount of the right-of-use asset and the lease liability at 1 January 2019 were determined as the carrying amount of lease asset and lease liability under IAS 17 immediately before that date.

Impacts on financial statements

Impacts on transition

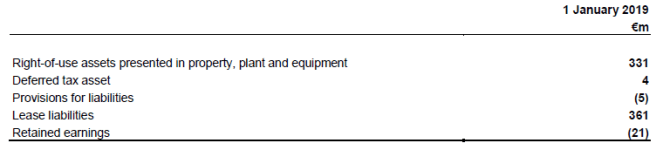

On transition to IFRS 16, the Group recognised additional right-of-use assets and additional lease liabilities, recognising the difference in retained earnings. The right-of use asset was adjusted by the onerous lease contract which was previously reported in ‘Provisions for liabilities’. The impact on transition is summarised below.

When measuring lease liabilities for leases that were classified as operating leases, the Group discounted lease payments using the lessee’s incremental borrowing rate at 1 January 2019. The weighted average rate applied was 3%.

The lease liabilities as at 1 January 2019 can be reconciled to the operating lease commitments as at 31 December 2018 as follows:

Impacts for the period

As a result of initially applying IFRS 16, in relation to the leases that were previously classified as operating leases, the Group recognised €307 million of right-of-use assets and €338 million of lease liabilities at 30 June 2019.

Also in relation to those leases under IFRS 16, the Group has recognised depreciation and interest costs instead of an operating lease expense. During the six months ended 30 June 2019, the Group recognised €40 million of depreciation charges and €5 million of interest costs from these leases.