Otsuka Holdings Co., Ltd. – Annual report – 31 December 2016

Industry: pharmaceuticals

Notes to Consolidated Financial Statements (extracts)

- Basis of Preparation (extract)

(1) Compliance with IFRS and first-time adoption

Pursuant to the provision of Article 93 of the Ordinance on Consolidated Financial Statements, the consolidated financial statements of the Company have been prepared in compliance with IFRS since the Company qualifies as a “Specified Company under Designated International Accounting Standards” prescribed in Article 1-2 of the Ordinance.

The Company’s consolidated financial statements for the fiscal year ended December 31, 2016 were approved on March 29, 2017 by Tatsuo Higuchi, President and Representative Director, and Atsumasa Makise, Senior Managing Director in charge of Corporate Finance.

The Group has adopted IFRS for the first time in the fiscal year ended December 31, 2016, and the date of transition to IFRS (hereinafter referred to as the “IFRS Transition Date”) is January 1, 2015. The impact of the transition to IFRS on financial position, operating results and cash flows of the Group on the IFRS Transition Date and in the comparative year is provided in “43. First-Time Adoption of IFRS.”

Except for IFRS that have not been early adopted and exemptions permitted under IFRS 1 “First-time Adoption of International Financial Reporting Standards” (hereinafter referred to as “IFRS 1”), the Group’s accounting policies are in accordance with IFRS effective as of December 31, 2016. The exemptions adopted and reconciliations required to be disclosed under IFRS are provided in “43. First-Time Adoption of IFRS.”

- First-Time Adoption of IFRS

The Company prepared consolidated financial statements in accordance with the generally accepted accounting principles in Japan (Japanese GAAP) for all periods up to and including the fiscal year ended December 31, 2015. The consolidated financial statements for the fiscal year ended December 31, 2016 are the first consolidated financial statements prepared by the Company in accordance with the International Financial Reporting Standards (IFRS). In the preparation of the consolidated financial statements, the Company has prepared the consolidated opening statement of financial position under IFRS on the IFRS Transition Date.

(1) Exemptions under IFRS 1 “First-time Adoption of International Financial Reporting Standards” IFRS requires a company adopting IFRS for the first time to apply the standards required under IFRS retrospectively. However, IFRS 1 allows exemptions from retrospective application of some IFRS requirements on first-time adoption of IFRS.

The Group applied the following exemption:

- Business combinations

It is allowed not to apply IFRS 3 “Business Combinations” retrospectively to business combinations that occurred before the IFRS Transition Date. The Group did not apply IFRS 3 retrospectively to business combinations that occurred before the IFRS Transition Date.

- Share-based payment transactions

It is allowed not to apply IFRS 2 “Share-based Payment” to share-based payment vested before the IFRS Transition Date. The Group did not apply IFRS 2 retrospectively to share-based payment vested before the IFRS Transition Date.

- Leases

It is allowed to determine whether or not an arrangement contains a lease based on facts and circumstances existing as of the IFRS Transition Date. The Group determined whether or not an arrangement contains a lease based on facts and circumstances existing as of the IFRS Transition Date.

- Foreign currency translation reserve

It is allowed to deem cumulative foreign currency translation reserve to be zero at the IFRS Transition Date. The Group deemed all cumulative foreign currency translation reserve to be zero as of the IFRS Transition Date.

- Designation of previously recognized financial instruments

It is allowed to designate equity financial assets as financial assets measured through other comprehensive income based on facts and circumstances existing as of the IFRS Transition Date. The Group designated equity financial assets, except for certain assets, as financial assets measured through other comprehensive income as of the IFRS Transition Date.

(2) Reconciliations

Reconciliations required to be disclosed in the first-time adoption of IFRS are as follows and include the following content.

The Group has disclosed the “reconciliation of equity (reconciliation from the consolidated balance sheet under Japanese GAAP to the consolidated statement of financial position under IFRS) as of January 1, 2015,” the IFRS Transition Date, which is required under IFRS 1 and the “reconciliation of equity (reconciliation from the consolidated balance sheet under Japanese GAAP to the consolidated statement of financial position under IFRS) as of December 31, 2015,” which is the final date for the consolidated financial statements issued in accordance with Japanese GAAP, and the “reconciliation of comprehensive income (reconciliation from the consolidated statement of comprehensive income and the consolidated statement of income under Japanese GAAP to the consolidated statement of comprehensive income and the consolidated statement of income under IFRS) for the fiscal year ended December 31, 2015.” Items that do not influence retained earnings and comprehensive income are included in “Adjustments of differences in presentation,” and items that influence retained earnings and comprehensive income are included in “Adjustments of differences in recognition and measurement” in the below reconciliations.

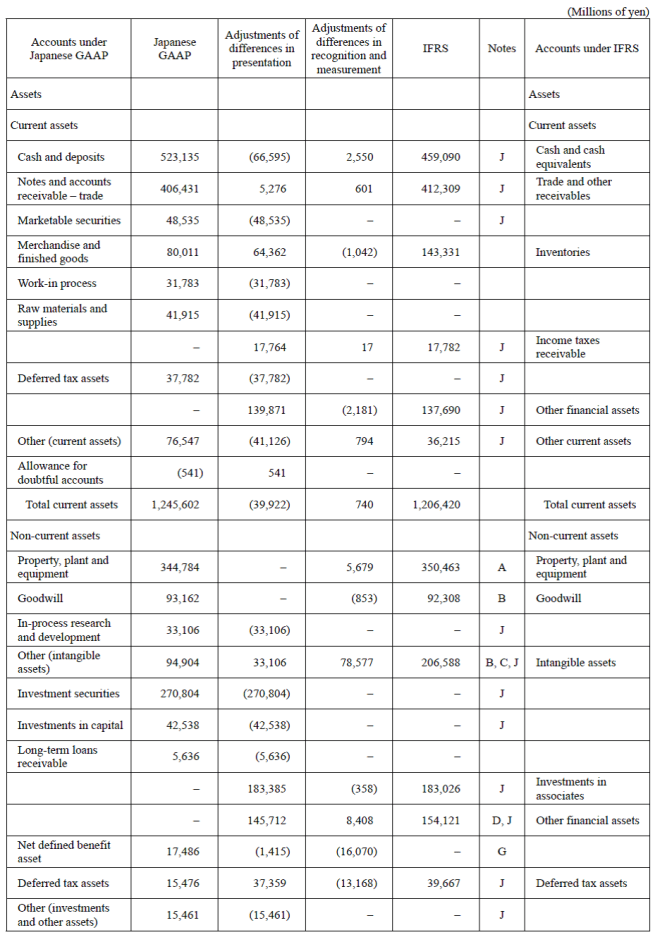

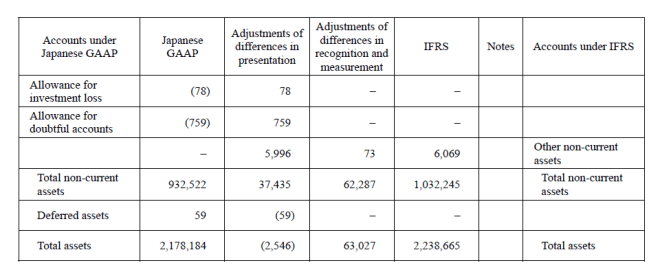

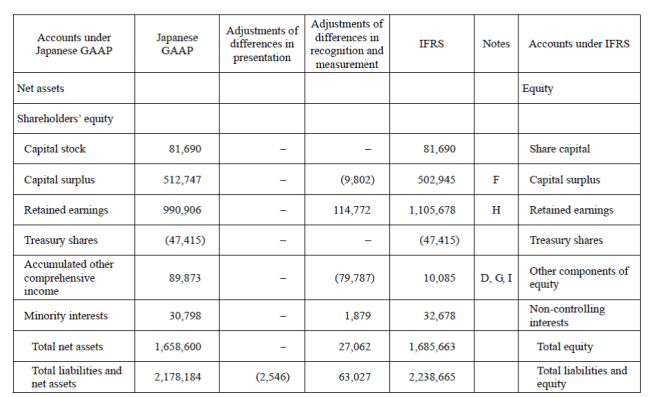

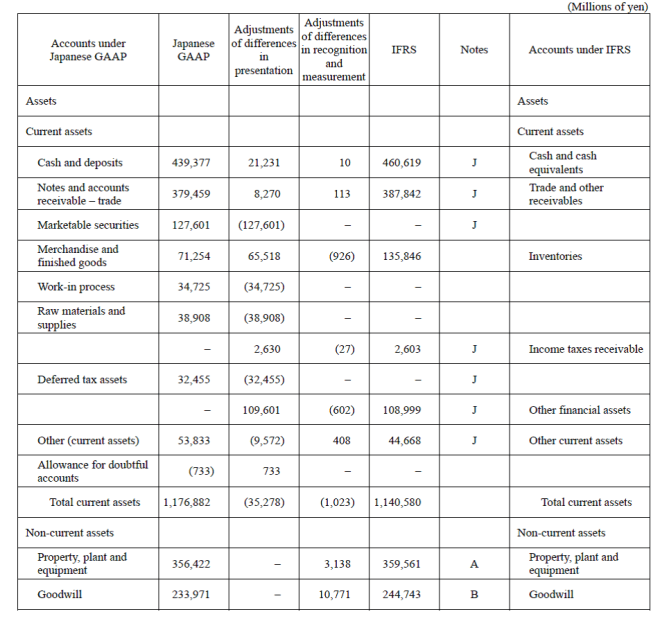

(i) Reconciliations of equity as of January 1, 2015 (IFRS Transition Date)

Notes on reconciliations

The main adjustments of differences are as follows:

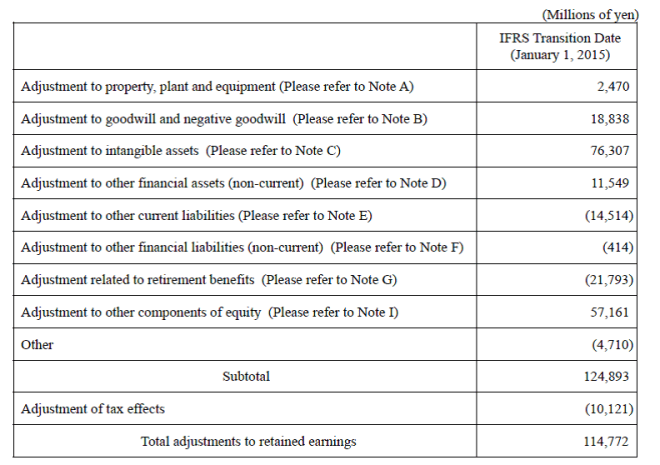

A. Adjustments to property, plant and equipment

For some subsidiaries that were not consolidated or to which the equity method was applied under Japanese GAAP, the scope of consolidation was reviewed under IFRS and they are considered to be consolidated subsidiaries. Consequently, property, plant and equipment have been capitalized.

Incidental costs such as import duties, acquisition taxes and professional fees for acquisition of property, plant and equipment, which were recorded as expenses under Japanese GAAP, are recognized and measured at the amount included in acquisition cost of the property, plant and equipment under IFRS, and the adjustments are made to retained earnings.

B. Adjustments to goodwill and negative goodwill

Under Japanese GAAP, for some business combinations, allocation of acquisition cost was not completed as of the transition date and goodwill was recognized and measured at the amount calculated by the tentative accounting treatment based on reasonable information that was available at that time; however, under IFRS, the finalization of the tentative accounting treatment is retrospectively reflected as of the transition date, and the adjustments are mainly made to intangible assets and retained earnings. In addition, under Japanese GAAP, goodwill of foreign subsidiaries arising from business combinations conducted before April 1, 2010 was translated at exchange rates prevailing at the date of the transaction; however, under IFRS, such goodwill is translated at exchange rates prevailing at the time of closing of accounts. The adjustments are made to other components of equity and immediately transferred to retained earnings. Under Japanese GAAP, negative goodwill arising from business combinations conducted before April 1, 2010 was recognized as liabilities at the date of the acquisition and amortized on a straight-line basis; however, under IFRS, since such negative goodwill is recognized as a gain at the date of the acquisition, the adjustments are made to retained earnings.

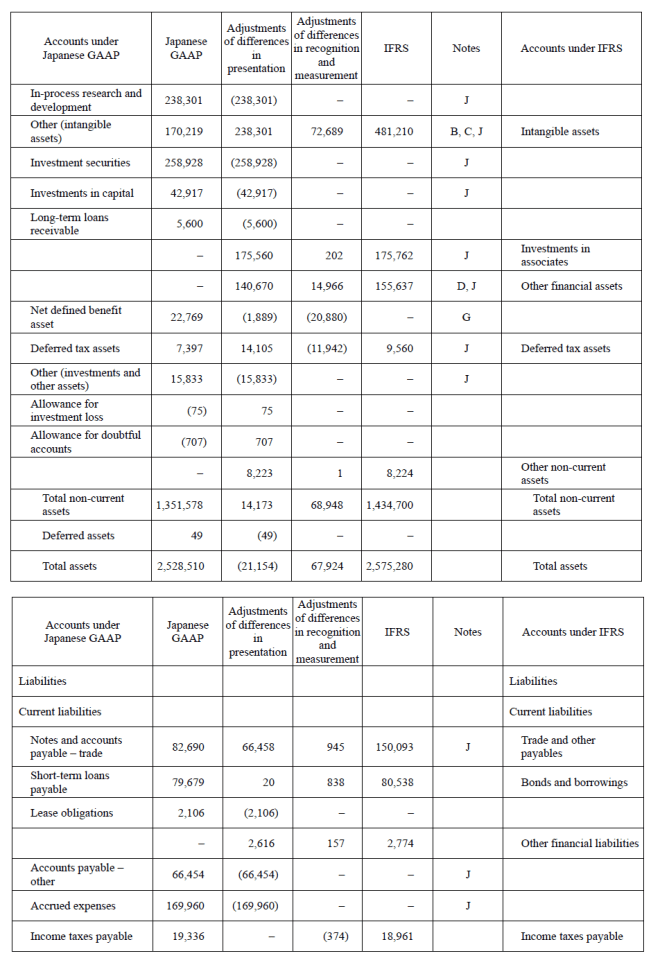

C. Adjustments to intangible assets

Under Japanese GAAP, expenditures for technology introduction contracts and others were recognized as research and development expenses; however, under IFRS, such expenditures that meet the definition of intangible assets under IAS 38 are capitalized, and the adjustments are made to retained earnings.

Under Japanese GAAP, for intangible assets with indefinite useful lives, amortization expenses were recognized on a straight-line basis with the useful life deemed as 20 years; however, under IFRS, because such assets are not amortized, the adjustments are made to retained earnings.

D. Adjustments to other financial assets (non-current)

Under Japanese GAAP, for securities of which the market value significantly decreased, impairment was recognized and acquisition cost was reduced; however, under IFRS, reduction of acquisition cost due to impairment is not made. Under Japanese GAAP, unlisted shares were mainly valued at cost using the moving average method, while under IFRS, such shares are measured at fair value. The adjustments for the resulting differences are made to retained earnings and other components of equity. Furthermore, for some subsidiaries that were not consolidated under Japanese GAAP, the scope of consolidation was reviewed under IFRS and they are considered to be consolidated subsidiaries. Consequently, elimination of investments and recording of assets and liabilities are conducted and the adjustments for the resulting differences are made to retained earnings.

E. Adjustments to other current liabilities

Unused paid absences, which are not required to be accounted for under Japanese GAAP, are recognized in liabilities under IFRS and the adjustments are made to retained earnings.

F. Adjustments to other financial liabilities (non-current)

For put options written on shares of foreign subsidiaries granted by the foreign subsidiaries to owners of non-controlling interests, which are not required to be accounted for under Japanese GAAP, the present value of the option exercise price is recognized as financial liabilities under IFRS, and the adjustments for the resulting differences are made to capital surplus and retained earnings.

G. Adjustments to retirement benefits

Under Japanese GAAP, for actuarial gains or losses, the amount was amortized by the straight-line method over a period within the average remaining service period (5 to 20 years) of eligible employees at the time of occurrence, beginning from the next fiscal year of occurrence; however, under IFRS, such actuarial gains or losses are recognized in other comprehensive income at the time of occurrence and immediately transferred to retained earnings.

Under Japanese GAAP, past service cost is amortized starting in the fiscal year incurred using a straight-line method over a certain period (5 to 23 years), but within the average remaining service period of employees; however, under IFRS, past service cost is recognized in gains or losses at the time of occurrence and immediately transferred to retained earnings.

Under IFRS, unlike Japanese GAAP, when a defined benefit plan is overfunded, the net defined benefit asset is limited to the asset ceiling, and when there are minimum funding requirements for past service, a reduction in assets or an increase in liabilities is made to the extent that minimum funding contributions payable to the plan will not be available as either a refund or a reduction in future contributions. Consequently, the adjustments are made to other comprehensive income and immediately transferred to retained earnings.

Retirement benefit obligations are recalculated in accordance with provisions of IFRS, and the adjustments are made to retained earnings.

H. Adjustments to retained earnings

The above adjustment to intangible assets includes ¥12,969 million of impairment losses on in-process research and development and trademarks, distribution rights and others, which was recognized for the first time on the IFRS Transition Date in the pharmaceuticals business. These impairment losses occurred because the carrying amount was reduced to the recoverable amount, which is value in use, due to a decrease in the profitability.

I. Adjustments to other components of equity

The Group applied the exemption of IFRS 1 and transferred all of cumulative foreign currency translation reserve to retained earnings on IFRS Transition Date.

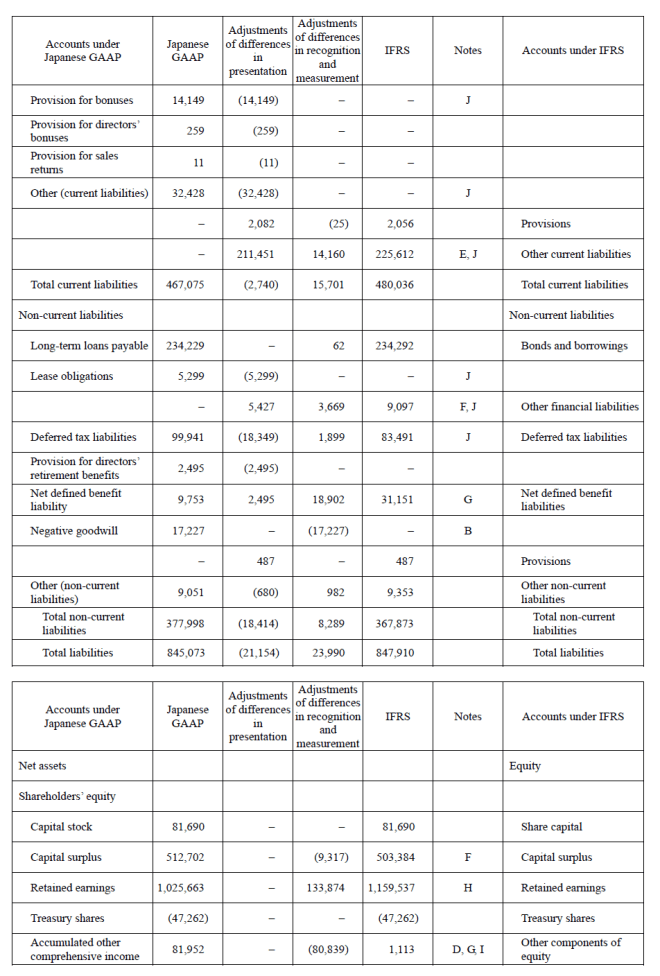

J. In addition to the above adjustments, the Group makes reclassifications to comply with provisions of IFRS. The major reclassifications are as follows:

- Cash and cash equivalents

Deposits with the deposit term of over three months included in cash and deposits under Japanese GAAP are reclassified to other financial assets (current) under IFRS.

- Trade and other receivables

Accounts receivable – other included in other in current assets under Japanese GAAP is presented as trade and other receivables under IFRS.

- Other financial assets (current)

Marketable securities, which was presented separately, and short-term loans receivable, etc. included in other in current assets under Japanese GAAP are presented as other financial assets (current) under IFRS.

- Other current assets

Short-term loans receivable included in other in current assets under Japanese GAAP are presented as other financial assets (current) under IFRS. In addition, income taxes receivable, etc. included in other in current assets under Japanese GAAP are presented separately as income taxes receivable under IFRS.

- Intangible assets

In-process research and development which was presented separately under Japanese GAAP is presented as intangible assets under IFRS.

- Investments in associates

Investments in associates included in investment securities and investments in capital under Japanese GAAP are presented separately under IFRS.

- Other financial assets (non-current)

Financial assets including shares and bonds presented as investment securities under Japanese GAAP are presented as other financial assets (non-current) under IFRS. In addition, long-term deposits, long-term loans receivable and lease and guarantee deposits, etc. presented as other in investments and other assets under Japanese GAAP are presented as other financial assets (non-current) under IFRS.

- Deferred tax assets (non-current) and deferred tax liabilities (non-current)

All current portions of deferred tax assets and deferred tax liabilities are reclassified to noncurrent portions.

- Trade and other payables

Accounts payable – other, etc. presented separately as current liabilities under Japanese GAAP are presented as trade and other payables under IFRS.

- Other current liabilities

Accrued expenses and provision for bonuses, as well as advances received, unearned revenue and accrued consumption taxes presented as other in current liabilities under Japanese GAAP are presented as other current liabilities under IFRS.

- Other financial liabilities (non-current)

Lease obligations presented as non-current liabilities under Japanese GAAP are presented as other financial liabilities (non-current) under IFRS.

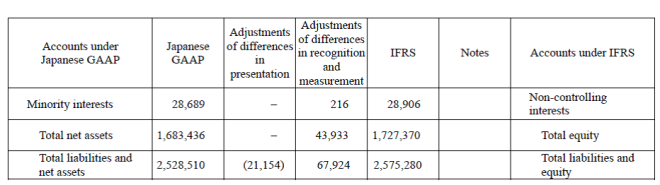

(ii) Adjustments to equity as of December 31, 2015

Notes on reconciliations

The main adjustments of differences are as follows:

A. Adjustments to property, plant and equipment

Incidental costs such as import duties, acquisition taxes and professional fees for acquisition of property, plant and equipment, which were recorded as expenses under Japanese GAAP, are recognized and measured at the amount included in acquisition cost of the property, plant and equipment under IFRS, and the adjustments are made to retained earnings.

B. Adjustments to goodwill and negative goodwill

Under Japanese GAAP, for some business combinations, allocation of acquisition cost was not completed as of the transition date and goodwill was recognized and measured at the amount calculated by the tentative accounting treatment based on reasonable information that was available at that time; however, under IFRS, the finalization of the tentative accounting treatment is retrospectively reflected as of the transition date, and the adjustments are mainly made to intangible assets and retained earnings. In addition, under Japanese GAAP, goodwill of foreign subsidiaries arising from business combinations conducted before April 1, 2010 was translated at exchange rates prevailing at the date of the transaction; however, under IFRS, such goodwill is translated at exchange rates prevailing at the time of closing of accounts, and the adjustments are made to other components of equity. Differences recognized as of the IFRS Transition Date are transferred to retained earnings. Under Japanese GAAP, goodwill was amortized over the period in which its effects were expected to occur; however, under IFRS, goodwill has not been amortized since the transition date.

Under Japanese GAAP, negative goodwill arising from business combinations conducted before April 1, 2010 was recognized as liabilities at the date of the acquisition and amortized on a straight-line basis; however, under IFRS, since such negative goodwill is recognized as a gain at the date of the acquisition, the adjustments are made to retained earnings.

C. Adjustments to intangible assets

Under Japanese GAAP, expenditures for technology introduction contracts and others were recognized as research and development expenses; however, under IFRS, such expenditures that meet the definition of intangible assets under IAS 38 are capitalized, and amortization expenses and impairment losses arising after the commencement of amortization are recognized in selling, general and administrative expenses.

Under Japanese GAAP, for intangible assets with indefinite useful lives, amortization expenses on intangible assets was recognized on a straight-line basis with the useful life deemed as 20 years; however, under IFRS, such assets are not amortized.

D. Adjustments to other current assets (non-current)

Under Japanese GAAP, for securities of which the market value significantly decreased, impairment was recognized and acquisition cost was reduced; however, under IFRS, reduction of acquisition cost due to impairment is not made. Under Japanese GAAP, unlisted shares were mainly valued at cost using the moving average method, while under IFRS, such shares are measured at fair value. The adjustments for the resulting differences are made to retained earnings and other components of equity.

E. Adjustments to other current liabilities

Unused paid absences, which are not required to be accounted for under Japanese GAAP, are recognized in liabilities under IFRS and the adjustments are made to retained earnings.

F. Adjustments to other financial liabilities (non-current)

For put options written on shares of foreign subsidiaries granted by the foreign subsidiaries to owners of non-controlling interests, which are not required to be accounted for under Japanese GAAP, the present value of the option exercise price is recognized as financial liabilities under IFRS, and the adjustments for the resulting differences are made to capital surplus and retained earnings.

G. Adjustments to retirement benefits

Under Japanese GAAP, for actuarial gains or losses, the amount was amortized by the straight-line method over a period within the average remaining service period (5 to 20 years) of eligible employees at the time of occurrence, beginning from the next fiscal year of occurrence; however, under IFRS, such actuarial gains or losses are recognized in other comprehensive income at the time of occurrence and immediately transferred to retained earnings.

Under Japanese GAAP, past service cost is amortized starting in the fiscal year incurred using a straight-line method over a certain period (5 to 23 years), but within the average remaining service period of employees; however, under IFRS, past service cost is recognized in gains or losses at the time of occurrence and immediately transferred to retained earnings.

Under IFRS, unlike Japanese GAAP, when a defined benefit plan is overfunded, the net defined benefit asset is limited to the asset ceiling, and when there are minimum funding requirements for past service, a reduction in assets or an increase in liabilities is made to the extent that minimum funding contributions payable to the plan will not be available as either a refund or a reduction in future contributions. Consequently, the adjustments are made to other comprehensive income and immediately transferred to retained earnings.

Retirement benefit obligations are recalculated in accordance with provisions of IFRS, and the adjustments are made to retained earnings.

H. Adjustments to retained earnings

I. Adjustments to other components of equity

I. Adjustments to other components of equity

The Group applied the exemption of IFRS 1 and transferred all of cumulative foreign currency translation reserve to retained earnings on IFRS Transition Date.

J. In addition to the above adjustments, the Group makes reclassifications to comply with provisions of IFRS. The major reclassifications are as follows:

- Cash and cash equivalents

Deposits with the deposit term of over three months included in cash and deposits under Japanese GAAP are reclassified to other financial assets (current) under IFRS. In addition, cash equivalents included in marketable securities under Japanese GAAP are presented as cash and cash equivalents under IFRS.

- Trade and other receivables

Accounts receivable – other included in other in current assets under Japanese GAAP is presented as trade and other receivables under IFRS.

- Other financial assets (current)

Marketable securities, which was presented separately, and short-term loans receivable, etc. included in other in current assets under Japanese GAAP are presented as other financial assets (current) under IFRS.

- Other current assets

Short-term loans receivable, etc. included in other in current assets under Japanese GAAP are presented as other financial assets (current) under IFRS. In addition, income taxes receivable, etc. included in other in current assets under Japanese GAAP are presented separately as income taxes receivable under IFRS.

- Intangible assets

In-process research and development which was presented separately under Japanese GAAP is presented as intangible assets under IFRS.

- Investments in associates

Investments in associates included in investment securities and investments in capital under Japanese GAAP are presented separately under IFRS.

- Other financial assets (non-current)

Financial assets including shares and bonds presented as investment securities under Japanese GAAP are presented as other financial assets (non-current) under IFRS. In addition, long-term deposits, long-term loans receivable and lease and guarantee deposits, etc. presented as other in investments and other assets under Japanese GAAP are presented as other financial assets (non-current) under IFRS.

- Deferred tax assets (non-current) and deferred tax liabilities (non-current)

All current portions of deferred tax assets and deferred tax liabilities are reclassified to noncurrent portions.

- Trade and other payables

Accounts payable – other, etc. presented separately as current liabilities under Japanese GAAP are presented as trade and other payables under IFRS.

- Other current liabilities

Accrued expenses and provision for bonuses, as well as advances received, unearned revenue and accrued consumption taxes presented as other in current liabilities under Japanese GAAP are presented as other current liabilities under IFRS.

- Other financial liabilities (non-current)

Lease obligations presented as non-current liabilities under Japanese GAAP are presented as other financial liabilities (non-current) under IFRS.

(iii) Reconciliations of profit or loss and comprehensive income for the fiscal year ended December 31, 2015

Notes on reconciliations

A. Adjustments to net sales

For some subsidiaries to which the equity method was applied under Japanese GAAP, the scope of consolidation was reviewed under IFRS and they are considered to be consolidated subsidiaries. Consequently, the adjustments are made.

B. Adjustments to cost of sales

Under Japanese GAAP, for actuarial gains or losses, the amount was amortized by the straight-line method over a period within the average remaining service period (5 to 20 years) of eligible employees at the time of occurrence, beginning from the next fiscal year of occurrence; however, under IFRS, such actuarial gains or losses are recognized in other comprehensive income at the time of occurrence and immediately transferred to retained earnings.

Under Japanese GAAP, past service cost is amortized starting in the fiscal year incurred using a straight-line method over a certain period (5 to 23 years), but within the average remaining service period of employees; however, under IFRS, past service cost is recognized in gains or losses at the time of occurrence.

For some subsidiaries to which the equity method was applied under Japanese GAAP, the scope of consolidation was reviewed under IFRS and they are considered to be consolidated subsidiaries. Consequently, the adjustments are made.

C. Adjustments to selling, general and administrative expenses

Under Japanese GAAP, goodwill was amortized over the period in which its effects were expected to occur; however, under IFRS, goodwill has not been amortized since the transition date.

Under Japanese GAAP, for actuarial gains or losses, the amount was amortized by the straight-line method over a period within the average remaining service period (5 to 20 years) of eligible employees at the time of occurrence, beginning from the next fiscal year of occurrence; however, under IFRS, such actuarial gains or losses are recognized in other comprehensive income at the time of occurrence and immediately transferred to retained earnings.

Under Japanese GAAP, past service cost is amortized starting in the fiscal year incurred using a straight-line method over a certain period (5 to 23 years), but within the average remaining service period of employees; however, under IFRS, past service cost is recognized in gains or losses at the time of occurrence.

Retirement benefit obligations are recalculated in accordance with provisions of IFRS, and the adjustments are made to retained earnings.

Under Japanese GAAP, expenditures for technology introduction contracts and others were recognized as research and development expenses; however, under IFRS, such expenditures that meet the definition of intangible assets under IAS 38 are capitalized and amortized over the estimated useful life, and impairment loss is recorded or reversed as necessary. Consequently, under IFRS, amortization expenses and impairment loss on trademarks, distribution rights and others have increased compared with those under Japanese GAAP. The amortization expenses and impairment loss are included in selling, general and administrative expenses.

Under Japanese GAAP, for intangible assets with indefinite useful lives, amortization expenses on intangible assets was recognized on a straight-line basis with the useful life deemed as 20 years; however, under IFRS, such assets are not amortized.

D. Adjustments to research and development expenses

Under Japanese GAAP, expenditures for technology introduction contracts and others were recognized as research and development expenses; however, under IFRS, such expenditures that meet the definition of intangible assets under IAS 38 are capitalized, and impairment loss is recorded or reversed as necessary. Under IFRS, such recording or reversal of impairment loss is recognized in research and development expenses.

Under Japanese GAAP, for actuarial gains or losses, the amount was amortized by the straight-line method over a period within the average remaining service period (5 to 20 years) of eligible employees at the time of occurrence, beginning from the next fiscal year of occurrence; however, under IFRS, such actuarial gains or losses are recognized in other comprehensive income at the time of occurrence and immediately transferred to retained earnings.

Under Japanese GAAP, past service cost is amortized starting in the fiscal year incurred using a straight-line method over a certain period (5 to 23 years), but within the average remaining service period of employees; however, under IFRS, past service cost is recognized in gains or losses at the time of occurrence.

Retirement benefit obligations are recalculated in accordance with provisions of IFRS, and the adjustments are made to retained earnings.

E. Adjustments to share of profit of associates

Under Japanese GAAP, goodwill on associates was amortized over the period in which its effects were expected to occur, and recognized as share of profit of associates; however, under IFRS, goodwill has not been amortized since the transition date.

F. Adjustments to other income

Under Japanese GAAP, negative goodwill arising from business combinations conducted before April 1, 2010 was recognized as liabilities at the date of the acquisition and amortized on a straight-line basis; however, under IFRS, since such negative goodwill is recognized as a gain at the date of the acquisition, the negative goodwill is not amortized.

G. Adjustments to finance income

For put options written on shares of foreign subsidiaries granted by the foreign subsidiaries to owners of non-controlling interests, which are not required to be accounted for under Japanese GAAP, the present value of the option exercise price is recognized as financial liabilities, and any changes after the initial recognition are recognized in profit or loss.

H. Adjustments to income tax expenses

Under Japanese GAAP, deferred tax assets associated with unrealized gains or losses were calculated using the effective tax rate of the seller; however, under IFRS, such deferred tax assets are calculated using the effective tax rate of the buyer. In addition, adjustments are made to the amount of income tax expenses due to temporary differences arising as a result of adjustments of other differences with IFRS and other factors.

I. In addition to the above adjustments, the Group makes reclassifications to comply with provisions of IFRS. The major reclassifications are as follows:

- Net sales

Payments of certain sales rebates were included in cost of sales and selling, general and administrative expenses under Japanese GAAP; however, they are deducted from net sales under IFRS.

- Selling, general and administrative expenses

Payments of certain sales rebates were included in cost of sales and selling, general and administrative expenses under Japanese GAAP; however, they are deducted from net sales under IFRS.

Impairment loss other than in-process research and development was included in impairment loss in extraordinary losses under Japanese GAAP; however, it is included in selling, general and administrative expenses under IFRS.

- Research and development expenses

Research and development expenses was included in selling, general and administrative expenses, while impairment loss of in-process research and development was included in impairment loss in extraordinary losses under Japanese GAAP; however, they are aggregated and presented separately as research and development expenses under IFRS.

- Share of profit of associates

Equity in earnings of affiliates was included in non-operating income under Japanese GAAP; however, it is presented separately as share of profit of associates under IFRS.

- Other income, other expenses, finance income, finance costs and other non-operating income (expenses)

Of the items included in non-operating income, non-operating expenses, extraordinary income and extraordinary losses under Japanese GAAP, items related to finance are reclassified to finance income and finance costs, while other items are reclassified to selling, general and administrative expenses, research and development expenses, other income, other expenses and other non-operating income (expenses) under IFRS.

J. Remeasurements of defined benefit plans

Under Japanese GAAP, for actuarial gains or losses, the amount was amortized by the straight-line method over a period within the average remaining service period (5 to 20 years) of eligible employees at the time of occurrence, beginning from the next fiscal year of occurrence; however, under IFRS, such actuarial gains or losses are recognized in other comprehensive income at the time of occurrence. Under IFRS, unlike Japanese GAAP, when a defined benefit plan is overfunded, the net defined benefit asset is limited to the asset ceiling, and when there are minimum funding requirements for past service, a reduction in assets or an increase in liabilities is made to the extent that minimum funding contributions payable to the plan will not be available as either a refund or a reduction in future contributions. Consequently, the adjustments are made to other comprehensive income.

K. Financial assets measured at fair value through other comprehensive income

Some equity instruments of which the balance sheet amount was the acquisition cost under Japanese GAAP are measured at fair value under IFRS, and the adjustments for the resulting differences are made to other comprehensive income. In addition, losses from valuation of equity instruments that were impaired under Japanese GAAP are recognized in other comprehensive income under IFRS.

(iv) Adjustments to cash flows

FY2015 (ended December 31, 2015)

The material differences between the Consolidated Statement of Cash Flows disclosed in accordance with Japanese GAAP and the Consolidated Statement of Cash Flows disclosed in accordance with IFRS are as follows.

The expenditures associated with research and development expenses were classified as cash flows from operating activities under Japanese GAAP because they were recognized as expenses when they were incurred, while under IFRS, the capitalized research and development expenses have been classified as cash flows from investing activities.

As a result, cash flows from investing activities decreased by ¥2,726 million and cash flows from operating activities increased by the same amount.