Deutsche Telekom AG – Annual report – 31 December 2025

Industry: telecoms

Accounting policies (extract)

Financial instruments (extract 1)

Financial assets include cash and cash equivalents, trade receivables, originated loans and other receivables, investments in equity instruments, and derivative financial assets. They are measured at fair value upon initial recognition. For all financial assets not subsequently measured at fair value through profit or loss, the transaction costs directly attributable to the acquisition are taken into account plus, in the case of debt instruments held, a loss account for expected credit losses. The fair values recognized in the statement of financial position are generally based on market prices of the financial assets. If these are not available, the fair value is determined using standard valuation models on the basis of current market parameters. For the classification and measurement of debt instruments held, the respective business model for managing the debt instruments and whether the instruments have the characteristics of a standard loan, i.e., whether the cash flows are solely payments of principal and interest, is relevant. Assuming the assets have these characteristics and if the business model is to hold to collect the asset’s contractual cash flows, they are measured at amortized cost. If the objective of the business model is to hold to collect and sell the contractual cash flows, they are measured at fair value through other comprehensive income with recycling to profit or loss at the date of their disposal. In all other cases, financial assets are measured at fair value through profit or loss. There may be different business models for separate portfolios of the same types of debt instruments, for example if factoring transactions exist for certain trade receivables.

Financial instruments (extract 2)

Investments in equity instruments represent strategic investments. Deutsche Telekom exercises the option of generally measuring these through other comprehensive income without recycling to profit or loss. The acquisition and disposal of strategic investments is based on business policy considerations.

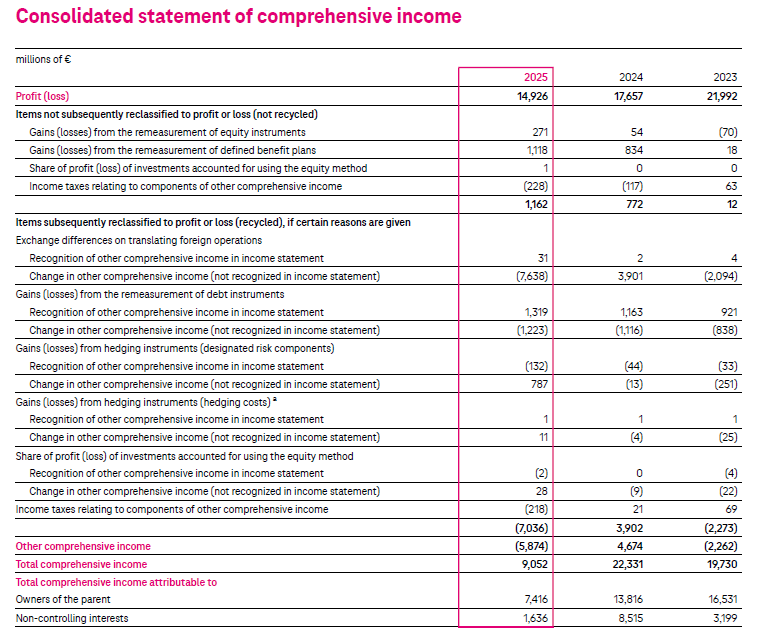

a The hedging costs relate entirely to cross-currency basis spreads. For further information, please refer to Note 43 “Financial instruments and risk management.”

32 Income taxes (extract)

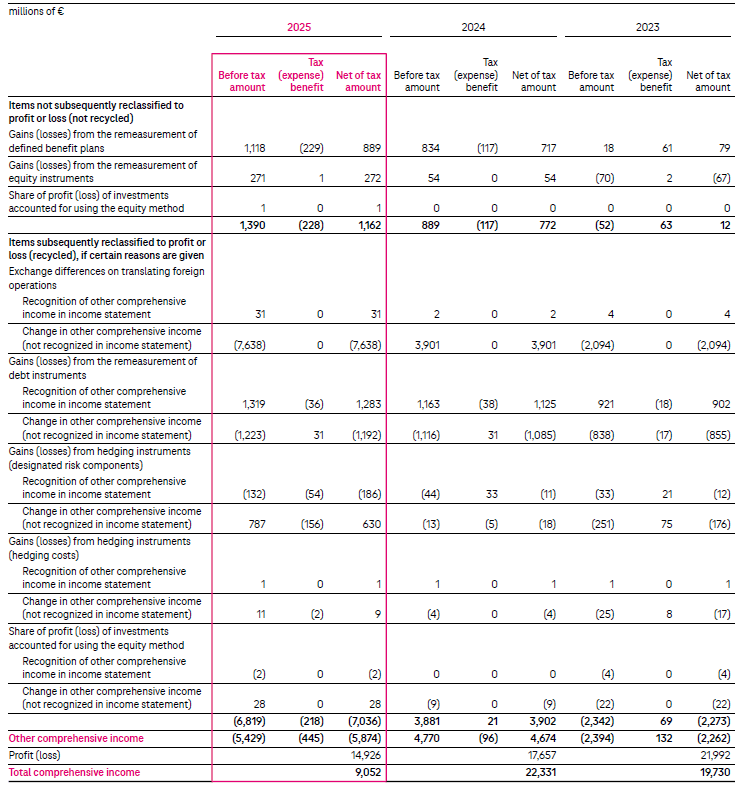

Income taxes in the statement of comprehensive income