Swisscom Ltd – Annual report – 31 December 2025

Industry: telecoms

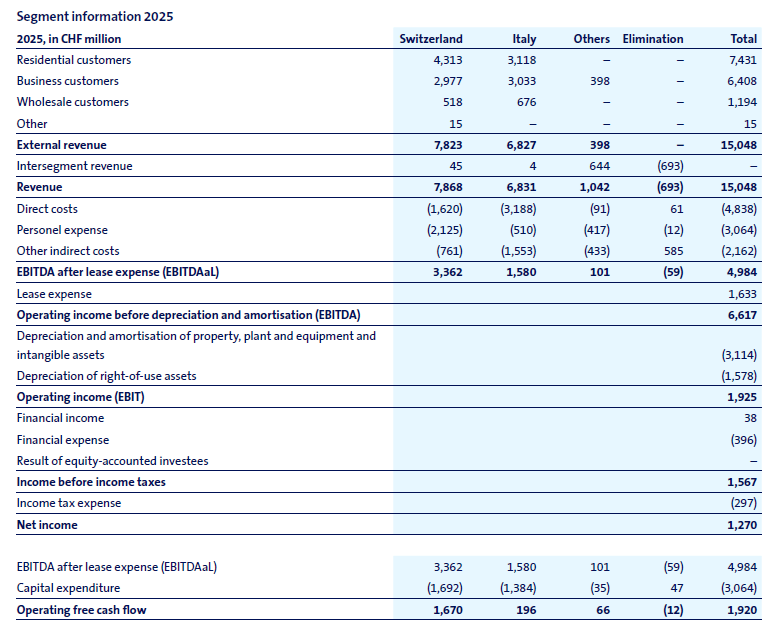

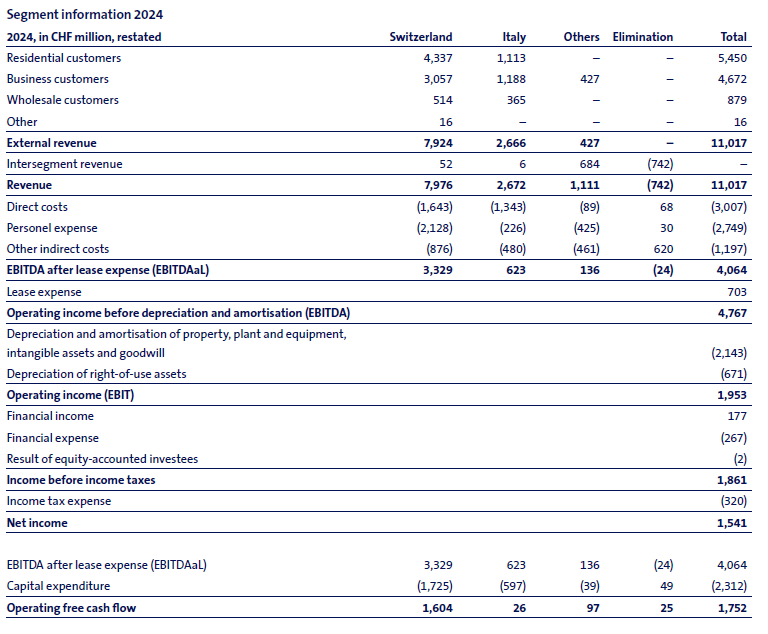

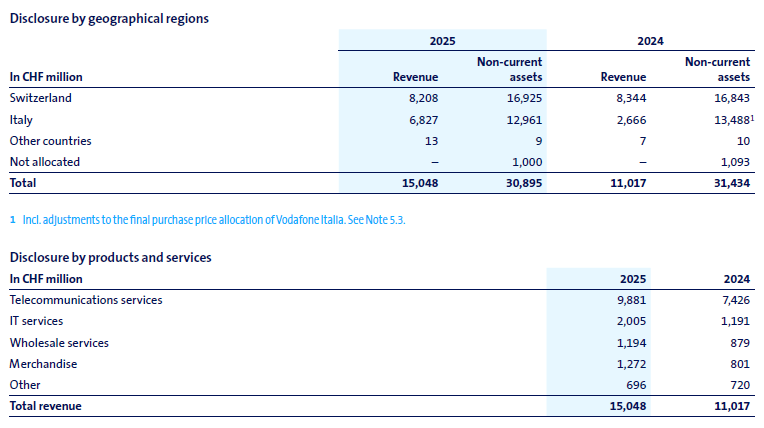

1.1 Segment information (extract)

General disclosures

Following the acquisition of Vodafone Italia at the end of 2024, Swisscom has adjusted its governance and organisational structure. A Group Executive Committee, led by the Group CEO, has been established to oversee Group-wide management. The business operations in Switzerland and Italy are each managed by a dedicated Executive Committee. Segment reporting has been aligned with this new organisational structure. Starting from the 2025 financial year, Swisscom has identified the segments Switzerland, Italy and Others.

The Switzerland and Italy segments are engaged in largely identical business activities, differing only in their regional scope. Residential customers are offered telecommunications services such as mobile communication, fixed-line telephony, broadband and TV. Business customers receive IT solutions in addition to telecommunications services, covering the entire spectrum of business ICT infrastructure from individual products to end-to-end solutions. In addition, the network infrastructure is made available to other telecommunications providers as wholesale services. Each segment includes its respective national telecommunications network and IT infrastructure. Groupwide functions are reported within the Switzerland segment.

From the 2025 financial year onwards, the EBITDA after lease expense (EBITDAaL) metric is used to measure and report on the financial performance of Swisscom and its operating segments. Following the acquisition of Vodafone Italia and the application of revised lease accounting principles from 2025 onwards, the significance of leases within Swisscom has increased substantially. Compared with the previously used EBITDA metric, EBITDAaL is considered a more reliable and relevant measure for financial management particularly – with respect to allocation of resources, performance assessment and communication with investors. The change also enhances comparability with other telecommunications providers.

Segment expense includes direct costs, personnel expense and other indirect costs. In the segment reporting, lease expense of CHF 874 million (prior year: CHF 412 million) is allocated to direct costs and to other indirect costs (current year: CHF 759 million; prior year: CHF 291 million). Segment expense includes the ordinary employer contributions as pension cost. The difference between these costs and pension cost determined in accordance with IAS 19 ’Employee Benefits’ is presented in the elimination column. The elimination column in the segment information of CHF –59 million (prior year: CHF –24 million) includes expense of CHF 12 million (prior year: income CHF 25 million), representing the IAS 19 pension cost reconciliation adjustment.

Capital expenditure comprises purchases of property, plant and equipment and intangible assets, as well as payments for indefeasible rights of use (IRU). IRUs are generally paid in full at the commencement of use and are classified as leases in accordance with IFRS 16 ‘Leases’. From an economic perspective, IRU payments are considered capital expenditure in the segment reporting. In 2025, capital expenditure includes IRU payments of CHF 57 million (prior year: CHF 24 million).

3.4 Goodwill (extract)

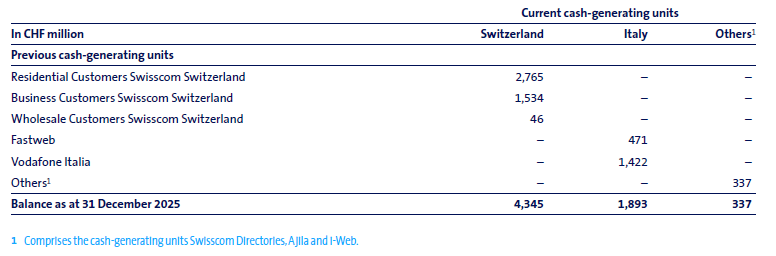

Swisscom allocates goodwill to the cash-generating units based on the business activities of the respective units. Goodwill arising from a business combination is allocated to those cash-generating units that are expected to benefit from the synergies of the business combination. Following the acquisition of Vodafone Italia at the end of 2024, Swisscom has revised its governance and organisational structure and, consequently, also its segment reporting effective from 2025. Segment reporting now comprises the segments Switzerland, Italy and Others. Accordingly, the goodwill arising from the Vodafone Italia acquisition has been allocated to the cash-generating unit Italy.

As at 31 December 2025, the goodwill recognised of CHF 6,575 million is allocated to the cash-generating units as follows:

The cash-generating units Italy and Others include impairment losses from previous years of CHF 1,188 million and CHF 30 million respectively.