International Consolidated Airlines Group, S.A. – Annual report – 31 December 2025

Industry: airline

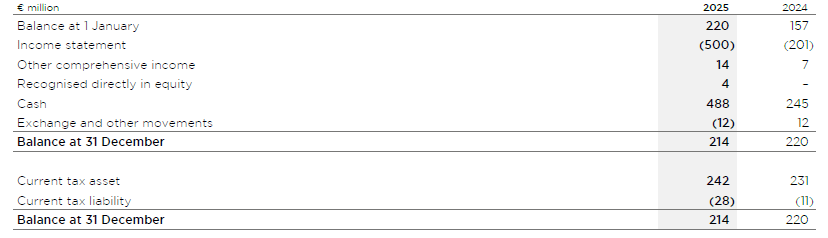

10 Tax (extract)

b Current tax asset

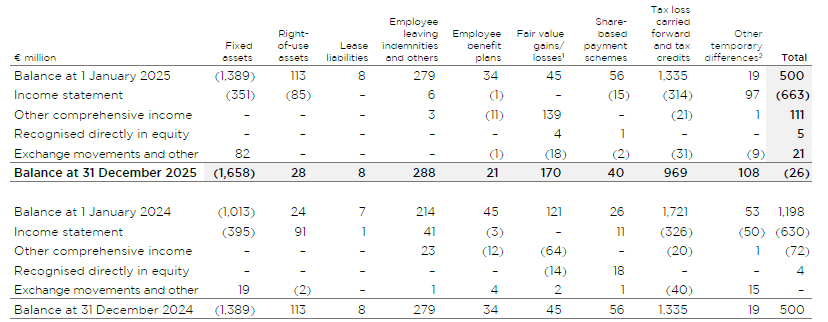

c Deferred tax (liability)/asset

1 Fair value gains/losses include both the Cash flow hedge reserve and the Cost of hedging reserve, of which the movement in relation to Other comprehensive income recognised in the Cash flow hedge reserve for 2025 was €151 million (2024: €40 million, see note 30d).

2 Other temporary differences include a deferred tax asset in relation to corporate interest of €64 million (2024: €36 million). There were no deferred tax liabilities in relation to unremitted earnings (2024: €5 million).

The deferred tax assets mainly arise in Spain and the UK and are expected to reverse in full beyond one year. Recognition of the deferred tax assets is supported by the expected reversal of deferred tax liabilities in corresponding periods and projections of operating performance laid out in the Board-approved business plans and longer term forecasts, where necessary, prepared by management.