Thomson Reuters Corporation – Half year report – 30 June 2017

Industry: media

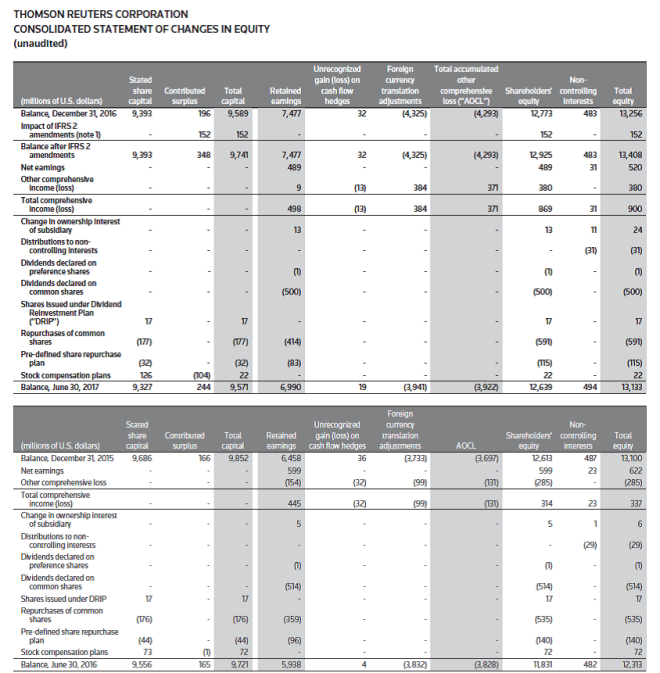

Notes to Consolidated Financial Statements (unaudited) (extract)

Changes in accounting policy

Effective January 1, 2017, the Company prospectively adopted the amendments to IFRS 2, Classification and Measurement of Share-based Payment Transactions. The amendments clarified the accounting for (a) the effects of vesting and non-vesting conditions on the measurement of cash-settled share-based payments; (b) share-based payment transactions with a net settlement feature for withholding tax obligations; and (c) a modification to the terms and conditions of a share-based payment that changes the classification of the transaction from cash-settled to equity-settled.

- Upon adoption on January 1, 2017, the Company reclassified $152 million of withholding tax obligations for share-based payments from liabilities to equity.

- The Company is no longer applying mark-to-market accounting on share-based payment transactions with a net settlement feature for withholding tax obligations. The impact was not material to the consolidated income statement and had no impact on the consolidated statement of cash flow for the three and six months ended June 30, 2017.