J Sainsbury plc – Annual report – 28 February 2026

Industry: retail

3 Material accounting policies (extract)

3.2 Cost of sales

Cost of sales consists of all costs that are directly attributable to the point of sale including warehouse costs, transportation costs and all the costs of operating retail outlets. In the case of Financial Services, cost of sales includes interest expense on operating activities, calculated using the effective interest method.

The Group regularly enters into arrangements to receive income from suppliers. This income can be in the form of purchase discounts, sales volume incentives or amounts received to perform marketing or promotional activities in store or online. These arrangements are collectively known as ‘supplier arrangements’ and are recognised as a reduction to cost of sales when the performance conditions within each agreement have been met. The types of supplier income and recognition policies are as follows:

Volume based discounts / incentive

Volume based discounts/ incentives are earned based on either sales or intake volumes over a defined period for defined products. Income is recognised as a deduction to cost of sales on sale of the inventory to which it relates. Where discounts are received based on intake volumes and there remains inventory unsold at the reporting period, the relevant discount is deducted from the carrying value of that inventory.

Marketing and promotional income

Marketing and promotional income primarily relates to in-store or on-line activity, including promotional or marketing materials, support for promotional pricing or product placement. Income is recognised over the period to which the agreement relates and in accordance with the performance conditions therein. As these agreements do not identify specific inventory purchases, this approach is deemed the best estimate to reflect the appropriate reduction in cost of sales.

Unpaid amounts relating to supplier arrangements are recognised within trade and other receivables, unless there is a legal right of offset, in which case it is recognised within trade and other payables. Amounts that have been invoiced at the balance sheet date are categorised as supplier arrangements due and those not yet invoiced are categorised as accrued supplier arrangements.

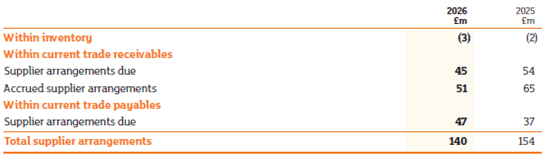

7 Supplier arrangements

The following amounts in relation to supplier arrangements are held on the balance sheet:

Additionally, £13 million (2025: £18 million) of supplier arrangements contractually agreed but not yet earned is held on the balance sheet within deferred income.